Bespoke Brunch Reads: 10/20/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

The League

‘The Losses Have Already Been Substantial.’ Adam Silver Addresses Fallout From the NBA-China Controversy by Sean Gregory (Time)

NBA Commissioner Adam Silver reports that the league is already losing millions in revenues in China and is willing to do so in order to stand behind its values related to freedom of expression. [Link]

Inside LeBron James’ and Adam Silver’s make-or-break moments in China by Dave McMenamin (ESPN)

A fascinating piece of reporting looking at the experience of players and league officials on the ground in Asia in the hours after the Houston Rockets’ GM tweeted support for pro-democracy protestors in Hong Kong. [Link; auto-playing video]

NBA exec: ‘It’s the dirty little secret that everybody knows about’ by Baxter Holmes (ESPN)

Sleep deprivation driven by ridiculously tight scheduling across multiple time zones and games played late into the night is a serious problem for basketball players and their teams. [Link]

The Wealthy

Credit Suisse to start charging wealthy clients for cash deposits by Joh Revill and Oliver Hirt (Reuters)

Negative interest rates are going to be passed on to high-balance deposits of more than 2mm CHF, with a 75 bps negative rate. Smaller balances will be unaffected. [Link]

Why Don’t Rich People Just Stop Working? by Alex Williams (NYT)

An investigation of why the most wealthy tend to keep earning money even though they already have so much; a human question, as much as an economic one. [Link; soft paywall]

Parenting

The New Parental Obsession: Checking Kids’ Grades Online by Julie Jargon (WSJ)

Technology now means parents can see how their kids are doing at school in near-real time, presenting parents with a difficult quandary: to check grades or leave their kids room to learn on their own. [Link; paywall]

What It’s Like To Be A Single Dad Living On Minimum Wage by Quinn Myers (Mel)

Money diaries from men who are living on the edges of what’s possible on low wages and with spiraling costs for utilities and rent. [Link]

Politics

Impeachment Could Mean Most Presidential Candidates Can’t Leave Washington, Or Talk. Sorry, Those Are (Really) The Rules. by Paul McLeod (Buzzfeed)

Senate rules require that an impeachment recommendation delivered by the House would require Senators to be in session Monday-Saturday for several weeks, taking Senators Booker, Bennet, Harris, Klobuchar, Sanders, and Warren off the campaign trail. [Link]

Justin Trudeau Is in Trouble. Voters Get to Say How Much by Theophilos Argitis, Cedric Sam and Stephen Wicary (Bloomberg)

With Canada headed to the polls tomorrow, polls show a very tight race between the reigning liberals and the right wing Conservatives, as well as a late surge from the leftward-leaning NDP. [Link; soft paywall]

Aerospace

Building China’s Comac C919 airplane involved a lot of hacking, report says by Catalin Cimpanu (ZDnet)

China’s entry into the narrow body jet market is a remarkable effort at hacking of suppliers in order to onshore all manufacturing of the plane’s components. [Link]

Human Guinea Pigs About to Embark on World’s First 20-Hour Airline Flight by Angus Whitley (Bloomberg)

Extremely efficient new planes mean the limiting condition on air service is no longer fuel, but the amount of time that humans can sit in an airplane. [Link; soft paywall, auto-playing video]

Schemes

A Guy on Reddit Turns $766 Into $107,758 on Two Options Trades by Brandon Kochkodin (Bloomberg)

Popular sub-Reddit WallStreetBets is famous for ludicrously long-odds plays by retail trades, but the most recent lottery payout is truly one of the ages. [Link; soft paywall]

How A Massive Facebook Scam Siphoned Millions Of Dollars From Unsuspecting Boomers by Craig Silverman (Buzzfeed)

San Diego’s Ad Inc. was designed to trick the elderly into signing up for “free” trials that came with a very hefty subscription on the back end and were almost impossible to cancel. [Link]

Crude

China’s Biggest Refiner to Reduce Operations After Freight Rates Skyrocket by Alfred Cang, Sharon Cho, and Serene Cheong (Bloomberg)

With freight rates surging, crude demand is softening thanks to lower refiner runs, all thanks to US sanctions on specific Chinese shipowners. [Link; soft paywall]

Economics

Housing and Recessions by Bill McBride (Calculated Risk)

An update on housing market data (very strong) and what it means for the economic outlook (recession doesn’t look particularly likely). [Link]

Social Media

TikTok has moved into Facebook’s backyard and is starting to poach its employees by Salvador Rodriguez (CNBC)

The exploding popularity of the short video app fueled by algorithms has led the firm to expand its Silicon Valley operations, picking up hiring. [Link]

Old Is New Again

The strange revival of vinyl records (The Economist)

Vinyl is still only 4% of total music sales but it’s a growing market thanks to the quality of the sound that old fashioned records put out. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — 10/18/19

This week’s Bespoke Report newsletter is now available for members.

The S&P 500 has been a bit top-heavy this month with the largest stocks in the index driving all of its October gains. We’ve seen interest rates start to push higher finally, which has helped Financials. The homebuilders have also extended gains even though mortgage rates have stopped going down. We’d be careful getting long the builders here given how overbought they’ve gotten. We cover everything else you need to know related to trends in financial markets in our weekly Bespoke Report. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 10/18/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

Bonds Bounce Back In Fund Flows Data

The week ended October 9th saw relatively large inflows into bond funds and relatively large outflows from equity funds. Across all mutual and exchange traded funds, equity flows were in the 7th percentile of all readings since 2013, with outflows of $11.5bn. Of that total, $5.8bn was ETFs, with the lion’s share of equity fund outflows coming from domestic funds. As has so frequently been the case lately, bond funds were the exact opposite situation. Total bond fund flows across mutual funds and ETFs meant $5.8bn of new cash on the week, which is in the 64th percentile of all periods. ETFs were relatively stronger, with bond funds drawing $1.9bn of inflows, higher than more than 81% of periods since 2013. Within both ETF and combined mutual and ETF flows, municipal bonds were the standouts, with total flows in the top 10% of all periods. Since 2013, $152bn has flowed into mutual funds and ETFs that own municipal government bonds, with more than $90bn of that coming since the end of 2017. Those flows are very likely being driven by tax-advantaged buying incentivized by the changes to the tax code at the end of 2017 which ended a variety of popular state and local tax deductions. Start a two-week free trial to Bespoke Institutional to unlock access to our actionable research and interactive tools.

ISM Offsides, If Not Utterly Incorrect

This week’s manufacturing activity releases from the New York Fed and Philly Fed showed a slightly weaker but generally upbeat assessment of economic activity. The numbers from these two regional surveys may not be fully representative of the aggregate national economy, but they’re usually a pretty good indicator. As shown in the chart below, they’ve been a decent guide to what the ISM Manufacturing index says about national activity since the Empire State manufacturing index started its releases in 2001.

Unlike these two indices, which have shown a general uptick in activity over the last few months, the ISM index shows a different route. But that data isn’t backed up by the average results across the five Fed districts that survey their manufacturers. The size and scale of the divergence is so big that one of these indices is almost certainly wrong, but which?

For a tiebreaker, Markit’s manufacturing survey suggests conditions are at multi-month highs and picking up, more consistent with the data from Fed surveys than ISM. Markit’s sample size is bigger and the index is more representative of the whole sector than ISM only; with all five regional Fed surveys in the mix, they also have a sample size advantage over ISM. Hard data of late (including manufacturing production, exports, and hiring) has all sided against ISM and is showing data more consistent with the Five Fed or Markit surveys. For now, it looks like the brutal ISM results are a bit overstated. Start a two-week free trial to Bespoke Institutional to unlock access to our actionable research and interactive tools.

Moving Abroad?

While the title may suggest it, this isn’t a political post geared towards Democrats who can’t stand President Trump or Republicans fearing the prospect of a President Warren or Sanders. What we’re talking about here is what could be early signs of a break in the nearly decade long trend of international stocks underperforming equities in the United States. The first chart below shows a long-term look at the relative strength of the MSCI Ex-US Index versus the S&P 500 going back to 1999. When the line is rising, it indicates outperformance on the part of international stocks (ROW), and when it is falling, US equities are outperforming.

While the first several years of this century were dominated by outperformance on the part of international stocks at the expense of the S&P 500, that trend reversed with the Global Financial Crisis as international stocks had given up all of their outperformance by 2012, and then continued to lag going forward. The lower chart shows a closer look at the relative strength between the two indices over the last year. Here, it has been mostly more of the same. Outside of a brief surge during the Q4 market rout late last year, ROW has underperformed the S&P 500 for pretty much all of 2019. That is up until recently. Since late August, the relative strength line of the ROW has actually been drifting higher. Granted, it’s not a major shift at this point, but you have to start somewhere, and as of now ROW’s relative strength is near a four-month high.

For emerging markets (EM), the trend has been nearly identical to that of the ROW. The charts below are the same as the ones above, except instead of the MSCI World Ex-US index, we substituted in the MSCI Emerging Markets Index. Here, it’s been a similar story as relative strength in EM peaked just after the Financial Crisis and has been drifting lower ever since. While EM hasn’t given up all of its outperformance from the earlier part of this century, it has given up most of it and is now right near multi-year lows. Like the picture for ROW, though, it’s still early, but in the last couple of months, the relative strength for EM has been slowly drifting higher and is now near three-month highs. Start a two-week free trial to Bespoke Institutional to unlock access to our actionable research and interactive tools.

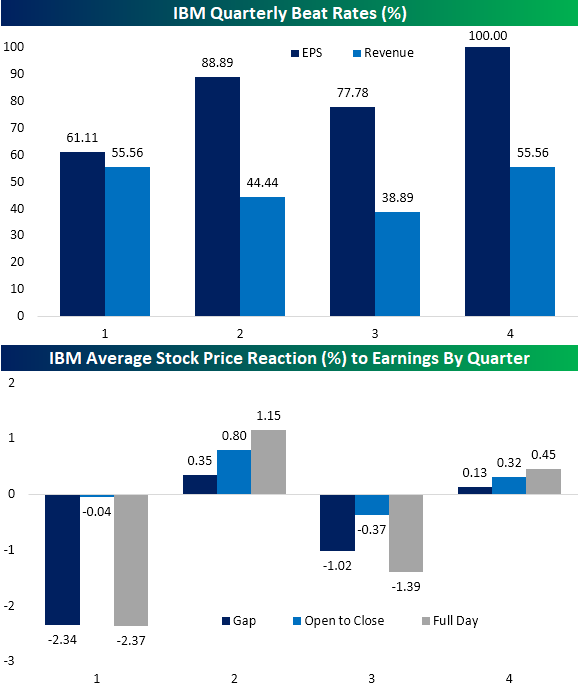

Dividend Stock Spotlight: International Business Machines (IBM)

After Wednesday’s close, investors got third-quarter results from blue-chip technology giant International Business Machines (IBM). Consensus analyst forecasts were calling for EPS of $2.66 and revenues of $18.285 billion. While IBM beat EPS by two cents, revenues were more than $250 million below forecasts and down 3.9% year-over-year (the fifth straight quarter with revenues lower than the previous year) even with the boost from newly acquired cloud computing company Red Hat which had stronger revenues In reaction to this miss at the top line, IBM’s stock declined 5.52% in trading on Thursday on elevated volumes.

Putting this week’s report into historical context, Q3 has been one of the weakest quarters in terms of beat rates as well as stock price reaction for IBM. Since 2000, IBM has only reported better than expected revenues in Q3 38.89% of the time, the lowest of any quarter. The EPS beat rate of 77.78% could also be better but is better than Q1’s 61.11%. Given this, Q1 and Q3 stock price reaction to earnings have been less frequently positive with IBM’s stock rising only 22% and 33% of the time, respectively. Q1 has actually been the weakest quarter as IBM has averaged a full day decline of 2.37%, most of which comes at the opening gap. Q3 is the next weakest quarter with an average decline of 1.39%. In other words, while yesterday’s decline was larger than expected, it is not unusual for the stock to be weak in Q3.

As a result of Thursday’s decline, IBM traded down through both its 50 and 200-DMA and now trades at the lower end of the past year’s range. The decline also pushed IBM’s dividend yield up to 4.83%, which is the highest yield of all S&P 500 technology stocks. It also has the third-highest yield of the 30 Dow stocks behind only Exxon Mobil (XOM) and Dow (DOW). Although the payout ratio is around the highest levels of the past 20 years at 85.8%, meaning further dividend growth given the slowing pace of revenues could come into question, 2019 marked the 24th consecutive year that IBM raised its dividend. Given this, if IBM raises the dividend again in 2020, the stock could potentially join the Dividend Aristocrats—a group of stocks with 25+ straight years of a growing dividend. If this were to happen, IBM would join Automatic Data Processing (ADP) as the only Technology stocks in the group. Additionally, at current yield levels, IBM would also be the fourth-highest yielder of the Dividend Aristocrats, behind AbbVie (ABBV), AT&T (T), and Exxon Mobil (XOM). Start a two-week free trial to Bespoke Institutional to access our interactive chart screens and much more.

Nasadaq – One Downtrend Down, Another To Go

In a post yesterday, we discussed the seemingly never-ending rangebound trading pattern for the STOXX 600. It’s not just Europe either. Seemingly everywhere you look these days, there’s a major equity index stuck in some sort of range. The Nasdaq is just one example of many. At a level of around 8,140, the Nasdaq is at the same level it was at exactly six months ago and also all the way back in August of last year.

Last week at this time, things were looking good for the Nasdaq as the index had bounced off of support at its 200-DMA and broke its short-term downtrend from the September lower high. This week has seen further gains with the Nasdaq rising more than 1%, but that rally looks to have stalled out yesterday right at another downtrend from the July high. A meaningful break of that downtrend would come into play at around 8,200 which is just over half of one percent above current levels. Using our Trend Analyzer tool, of the 100 stocks in the Nasdaq 100, heading into today, 43 were overbought and just five were oversold, so it may take a few days of ‘rest’ for the index before a meaningful break of that downtrend can occur. Start a two-week free trial to Bespoke Institutional to unlock access to all of our interactive tools.

Bespoke’s Morning Lineup – 10/18/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Europe Rejections, Construction Cruising, Manufacturing Divergence – 10/17/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, beginning with a technical note, we show the resistance European markets have run into and the breakdown in the dollar. Moving onto economic data, we show the pause in September home construction data. We then provide an update to our Five Fed Manufacturing Composite, including the massive divergence between the Empire and Philly Fed’s indices with ISM. We finish with a look at today’s EIA data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!