Bespoke Brunch Reads: 5/22/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Sentiment Check

Stock Market Is Top-Heavy, but Carnage Is Widespread by Karen Langley (WSJ)

The drop in stocks this year has been acute among the largest companies, but plenty of stocks beneath the surface are getting punished heavily as well. [Link; paywall]

Wall Street is heading into a summer from hell — and top investors say it’s going to bring a near-biblical reckoning to the market by Linette Lopez (Business Insider)

Always worth noting when adjectives like “biblical” get unleashed to talk about stock market declines; this kind of extreme sentiment is usually something you see closer to bottoms than tops. [Link]

This Could Be a Lost Decade for Stocks by Spencer Jakob (WSJ)

While the near-term headwinds for stocks are well-understood, we are starting to see extrapolations of those headwinds forward over the long-term, another sign of a sentiment extreme that should be of note to contrarians. [Link; paywall]

US CEO Confidence (The Conference Board)

The outlook for chief executives surveyed by The Conference Board and The Business Council has collapsed over the last several quarters, though it remains above the lows from 2019 and 2009. [Link]

Child Rearing

Asia’s advanced economies now have lower birth rates than Japan (The Economist)

Extremely high housing costs have driven down the fertility rate across Asia. Worries about Japan’s low birth rate now look somewhat antiquated given the country has one of the highest birth rates in the region as-of 2020. [Link; soft paywall]

Teen Babysitters Are Charging $30 an Hour Now, Because They Can by Rachel Wolfe (WSJ)

Wage growth is soaring for babysitters as hourly rates roughly double versus pre-pandemic and bargaining power is exerted by the scarce supply of willing sitters. [Link; paywall]

Supply Chains

Giant container ships are ruining everything by Rachel Premack (FreightWaves)

Since the 1980s, ship size has risen by a factor of more than 5 since the early 1980s. Larger ships are a sign of concentrated market power, port congestion, and excess capacity investment during weaker periods of the global shipping industry. [Link]

Critical minerals threaten a decades-long trend of cost declines for clean energy technologies by Tae-Yoon Kim (IEA)

Given the IEA’s history of over-estimating renewables costs and under-estimating renewables installation capacity, this analysis should be taken with a grain of salt. That said, it’s indisputable that many of the inputs for renewable energy supply have gotten significantly more expensive. [Link]

Civil Asset Forfeiture

Michigan Couple Says Town Seized Their Building and Offered To Return It if They Bought Two Cars for Police by C.J. Ciaramella (Reason)

A town in Michigan illegally seized a building, then tried to shake down the owners for two new police vehicles before they would return the stolen property. [Link]

Short-Sightedness

HSBC AM global head of responsible investing: ‘Who cares if Miami is six metres under water in 100 years?’ by James Baxter-Darrington (Investment Week)

The head of HSBC’s asset management division thinks the real problem with climate change is “the amount of work these people make me do”. [Link]

The Fed

Why the Fed matters to regular Americans, in one stunning chart: Morning Brief by Myles Udland (Yahoo! Finance)

The median listed home price’s carrying cost has risen over 40% in the past year as the Federal Reserve’s move into tightening and soaring home prices drive massive increases in mortgage payments for new buyers. [Link; auto-playing video]

Dressing Up

Leave the Sweatshirt at Home. Dining Dress Codes Are Back. by Priya Krishna (NYT)

Restauranteurs are starting to demand more of their patrons, especially when it comes to the attire they don for their dining experience. [Link; soft paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

Q1 Earnings Rhetoric

In our Conference Call Recaps, which are available to institutional subscribers, we summarize the conference calls and earnings releases of the most important earnings reports. Not only do we summarize the earnings results and the guidance, but we also relay each company’s macro and longer-term outlook to help subscribers keep up to date on the ever-changing landscape in topics spanning the US consumer, supply chains, inflation, labor, travel, technological developments, housing, foreign exchange, and capital markets. Click here to become a Bespoke member today!

Below we have provided some of the interesting insights we heard during the Q1 earnings season. We find that they are a helpful way to keep abreast of the major macro themes. Enjoy!

Summary

The Russia-Ukraine conflict only exacerbated an already strained supply chain environment and pushed commodity inflation even higher. Investors can reasonably assume that the constraints faced by the broader economy will persist throughout the fiscal year with some slight easing in the back half. The labor situation seems to have improved substantially, and certain companies even had a glut of labor supply. The consumer still appears quite strong, which means that price hikes will likely be taken in stride. View a complimentary sample of our Conference Call Recaps by clicking on the thumbnail below:

US Spending/Consumer

American Express (AXP) saw “increased engagement across our customer categories, led by strong spending by Millennial and Gen Z Card Members and small and medium-sized businesses, which were up 56 percent and 30 percent, respectively.”

“In terms of the North American business… we feel strong about the consumer demand.” – Whirlpool (WHR)

“Consumer spending… is quite robust [and] the labor market is almost fully recovered.” – Automatic Data Processing (ADP)

McDonald’s (MCD) is “keeping a close watch on lower-end consumers,” but “food at home has been increasing even more than food away from home.” The US consumer is in “good shape”.

United Rentals (URI) saw strong “customer sentiment and robust project activity.”

“We remain optimistic on the economy, at least for the short term – consumer and business balance sheets as well as consumer spending remain at healthy levels – but see significant geopolitical and economic challenges ahead due to high inflation, supply chain issues and the war in Ukraine.” – JP Morgan (JPM)

In the domestic parks segment, Disney’s (DIS) 2022 results will be “powered by strong demand coupled with customized and personalized guest experience enhancements that grew per capita spending by more than 40% versus 2019.”

Walmart’s (WMT) full-year guidance assumes “a generally stable consumer in the US, higher supply chain costs [and] continued pressure from inflation.”

Although inflation contributed to the rise in the average ticket price, customers “continue to trade up for premium innovative products.” – Home Depot (HD)

“As I sit here today, I’m not seeing any sign of a consumer slowdown.” – Target (TGT)

“When we talk to our guests, they often express their concerns about a host of rapidly changing conditions, ranging from geopolitics to high-end persistent inflation… particularly in food and energy.” – Target (TGT)

Supply Chain

“After a promising start the year, the operating environment soon changed with very significant geopolitical conflict, a resurgence of COVID in various places, record-high inflation and continued challenges on [the] supply chain front.” –Coca-Cola (KO)

“We are still seeing… inflated costs [and] quite a bit of disruption in our supply base.” – Whirlpool (WHR)

United Parcel Service (UPS) has been focused on digitization. Their new technology “enables [smaller customers] to begin shipping in under two minutes instead of… an average of 10 days.”

Microsoft (MSFT) is experiencing “constraints from the shutdowns in China.”

Apple (AAPL) noted that supply chain issues were “significantly lower” than they were in the December quarter before China began shutting down cities and factories again.

Management at Tesla (TSLA) maintained their volume growth target of 50% per annum over a multiyear horizon. However, over the last several quarters, “supply chain became the main limiting factor, which is likely to continue through the rest of 2022.”

“External challenges include limited availability and rising prices of certain commodities; as well as increased costs for labor, energy and transportation. These impacts are pervasive across the enterprise, but most notable in Consumer Health. We expect these pressures will continue to some degree throughout the remainder of 2022.” – Johnson & Johnson (JNJ)

JB Hunt (JBHT) gave clarity on the Chinese supply-chain situation, stating that the situation in Shanghai “looks just like a lot of ships and a little bit of water,” which will likely reach the US in the summer. Management expects ports to be relatively clogged in July.

As per Snap (SNAP), “supply chain shortages and labor disruptions, rising inflation, and geopolitical unrest” are impacting advertising budgets.

Constellation Brands (STZ) said that the company is facing numerous headwinds, such as “various supply chain challenges, adverse weather events, rising inflation [and] rapidly shifting consumer preferences.”

Lululemon (LULU) “continues to experience delays across [the] global network, particularly related to transporting products via ocean freight.”

KB Home (KBH) commented: “We underestimated the degree to which the Omicron variant would exacerbate an already constrained supply chain and workforce… While we take responsibility for our deliveries being below our prior expectations… we acknowledge that the variant was a significant contributing factor.”

Amazon (AMZN) is “no longer chasing physical or staffing capacity, our teams are squarely focused on improving productivity and cost efficiencies throughout our fulfillment network.”

“Simply said, [SBUX does] not have the adequate capacity to meet the growth demand.”

“We saw much higher than expected freight and transportation costs and a more dramatic change in our sales mix than we anticipated. This resulted in excess inventory, much of it in bulky categories which put additional strain on our already stretched supply chain.” – Target (TGT)

Inflation

“Pricing… has to be earning for the brands… When you go into high inflation, consumers come under pressure. There’s clearly reductions in real purchasing power going on for some segments of the population, if not everyone around the world.” – Coca Cola (KO)

“Restaurant-level margins continue to be impacted by unprecedented levels of inflation,” As per Chipotle (CMG)

Chipotle (CMG) saw “very little resistance to the pricing so far,” as menu prices were raised by over 4%.

“There are component costs that are falling and ones that are rising, and so not all of them are moving in the same direction.” – Apple (AAPL)

Pool Corp (POOL) added that the “tight labor market” is holding back installations, maintenance and repairs. On the bright side, the company has “seen some improvements in… supply chain issues.” POOL has “anticipated price increases” baked into their forecasts.

“Based on current prices, Alcoa (AA) expects both alumina and aluminum realized third-party prices to be higher than the first quarter, with that benefit partly offset by… higher energy and raw materials costs.”

Walgreens (WBA) stated: “inflation is on the rise… we expect to pass through most of that.”

Albemarle’s (ALB) guidance raise was largely due to higher “pricing in its Lithium and Bromine businesses… partially offset by inflationary cost pressures, particularly for natural gas in Europe.”

“Price leadership is especially important right now and one-stop shopping becomes more than just convenience when people are paying over $4 a gallon for fuel.” – Walmart (WMT)

Labor

“We are seeing hybrid approaches to learning and working are here to stay.” – Alphabet (GOOGL)

“The restaurants are staffed, we’re seeing performance in throughput.” – Chipotle (CMG)

“Strong overall economic activity continues to keep demand for labor high and we’ve been pleased to see labor force participation gradually recover over the course of the year.” – Automatic Data Processing (ADP)

Omicron led to “fairly meaningful labor challenges at the start of the quarter… as driver availability and productivity were impacted.” – JB Hunt Transport (JBHT)

“Labor continues to be an area with the greatest inflationary pressure in both professional driver and non-driver salary wages and benefits and we expect that trend to continue throughout the remainder of the year.” – JB Hunt Transport (JBHT)

“Associates that were out on COVID leave came back to work faster than we expected.” – Walmart (WMT)

Travel

“Travel and Entertainment spending was up 121 percent… and essentially reached pre-pandemic levels globally for the first time in March, driven by continued strength in consumer travel.” – American Express (AXP)

JPMorgan Chase (JPM) noted a “pick-up in credit card spending on travel and dining,” which is expected to continue into the next several quarters.

The travel industry is experiencing “robust consumer demand and an accelerating return of business and international travel.” – Delta (DAL)

According to Delta (DAL): “As demand continues to recover and we restore additional capacity in the second half of the year, we expect our non-fuel unit cost comparisons to 2019 will improve to up mid-single digits.”

Delta’s (DAL) press release stated: “Consumer demand accelerated through the quarter, highlighted by strong spring break performance. As Omicron faded, offices reopened and travel restrictions were lifted, resulting in an improvement in business travel demand and a stronger fare environment.”

In March, Hilton’s (HLT) system-wide rates “were up 3% compared to 2019 levels” due to “strong leisure trends”. Additionally, overall business transient now comprises 45% of total segment mix, just shy of pre-pandemic levels.”

In China, “re-imposed lockdowns suppressed demand [but] the rest of the Asia Pacific region saw a modest improvement in demand recovery as more countries loosen border and arrival controls in March.” – Hilton (HLT)

Technological Developments

This year, UPS will begin to implement “automated bagging, automated label application and robotic small sort… to drive increased productivity”.

“Waymo became the first company to run fully autonomous ride-hailing operations in multiple locations simultaneously.” – Alphabet (GOOGL)

Alphabet (GOOGL) also launched multi-search this quarter, which is “a new way people can find what they need using both images and words.”

Tech spend “As a percentage of GDP [is], by the end of the decade, going to double.” – Microsoft (MSFT)

Horizon, Meta’s (FB) metaverse platform, will launch through a web version “later this year.”

Meta (FB) is planning to launch a new headset (codenamed Project Cambria), “which will be more focused on work use cases and eventually [replace] your laptop or work setup.”

In order to mitigate semiconductor supply chain constraints, Apple (AAPL) developed “the world’s most powerful chip for a personal computer,” which is named M1 Ultra.

Due to extremely high commodity prices, the Tesla (TSLA) investor presentation stated that “diversification of battery chemistries is critical for long-term capacity growth” and nearly half of the vehicles produced in Q1 utilized lithium iron phosphate batteries, “containing no nickel or cobalt.”

According to Elon Musk, Tesla (TSLA) is working on a “dedicated robotaxi that’s highly optimized for autonomy, meaning it would not have a steering wheel or pedals.” TSLA is targeting 2024 for volume production of the robotaxi. TSLA also “remains on track to reach volume production of the Cybertruck next year.”

“Harnessing the power of technologies such as hybrid cloud and AI remains essential as our clients face a number of strategic challenges and opportunities, whether it’s competing for talent, supply chain issues, inflation, cybersecurity or geopolitical instability.” – International Business Machines (IBM)

JPMorgan Chase (JPM) is building out “real-time payments [and] certain blockchain type things” to build out wholesale capabilities.

CarMax (KMX) recently unveiled online technology that allows the company to make instant cash offers for used vehicles. CEO Bill Nash stated that “the rollout and rapid adoption of our online instant appraisal offer has solidified our position as the nation’s largest buyer of vehicles from consumers, nearly doubling our fiscal 2022 inventory self-sufficiency and propelling our wholesale business to new heights.”

Walgreens (WBA) recently acquired VillageMD and Shields in an effort to deliver “consumer-centric, technology-enabled healthcare” to local communities.

According to Micron (MU), new DRAM and NAND products are “achieving excellent yields, providing [MU] with solid front-end cost reductions and contributing meaningful revenue. [MU] qualified additional products on the advanced notes with a broad set of customers.”

Lululemon (LULU) is “partnering with and investing in Genomatica to create the first-ever plant-based alternative to nylon.”

“Everywhere we look, whether it is in entertainment, education or the enterprise, content is fueling the global economy. The democratization of creativity, the emergence of new ways to work and learn from anywhere, and the business mandate for personalized customer experiences underscore the immense opportunities we have as a company.” – Adobe (ADBE)

“New technologies will continue to shrink geographic distances, but countries and companies are reevaluating their interdependencies in a way that we have not seen since the end of the Cold War.” – Blackrock (BLK)

Amazon.com (AMZN) users can now “ask Alexa about symptoms for common health ailments… and virtually connect to health care professionals through a new collaboration with Teladoc.” In addition, AMZN’s virtual health services are now available 24/7 in the US.

“We made a lot of progress on both the wafer side and significant investments on the substrates… we continue to get…very good support from our suppliers.” – Advanced Micro Devices (AMD)

Starbucks (SBUX) is planning to launch “a unique platform for NFTs” on web 3.0 that will create “new revenue streams for SBUX.”

Construction/Housing

United Rentals (URI) is “starting to have conversations with customers about federal [infrastructure] projects that should kick off in 2023.”

“It’s hard to find a leading construction indicator that isn’t flashing green right now.” – United Rentals (URI)

According to POOL Corp (POOL): “outdoor living remains a priority with homeowners across North America.”

JPMorgan Chase (JPM) saw home lending originations decline by 37% y/y, “primarily due to the rising rate environment.”

In the guidance provided by KB Homes (KBH), the average selling price per home is expected to be $495,000 at the midpoint of FY 2022. This would translate to a y/y increase of 17.1%, so don’t expect a pullback in home values any time soon.

“The medium-to-longer term underpinnings of demand for home improvement have never been stronger.” – Home Depot (HD)

Foreign Exchange Rates

“With the stronger U.S. dollar and based on current rates, we now expect FX to decrease total company revenue growth by approximately two points.” – Microsoft (MSFT)

“We are reiterating our currency outlook of a two- to three-point currency headwind to [sales] a three- to four-point currency headwind to [EPS] for full year 2022.” – Coca-Cola (KO)

Capital Markets

BlackRock (BLK) commented, “we’re not seeing any real panic at all in the fixed income market, despite the worst performance in fixed income in 30-plus years in one quarter.”

Blackrock (BLK) added: “breadth and resilience enable us to play offense when others may be pulling back. Our agility in responding to opportunities and continued investments across market cycles have driven our industry-leading growth, our consistent growth, and generated value for our shareholders.”

JPMorgan Chase (JPM) “cannot foresee any scenario at all, where you’re not going to have a lot of volatility in markets going forward.” This prediction is due to the high inflationary environment, quantitative tightening, and elevated commodity prices.

“Gross investment banking revenue of $729 million was down 35% driven by both fewer large deals and less flow activity.” – JPMorgan Chase (JPM)

Click here to become a Bespoke member today!

B.I.G. Tips – Decile Analysis Since the Nasdaq’s Peak

The Bespoke Report – 5/20/22 – Could Use a Little Help From Lady Luck

This week’s Bespoke Report newsletter is now available for members.

How’s the glass? Half-full? No way. It’s not even half empty. It’s been emptied, put in the recycling machine, and crushed to pieces. We have a Fed chair talking about a ‘painful’ period of policy normalization, and a Treasury Secretary telling the public that a soft-landing is ‘conceivable’ with a little bit of ‘skill and luck.’ Somebody get us a rabbit’s foot and some four-leaf clovers, the fate of the world’s largest economy hinges on it! Need they be reminded of the famous quote: “Hope is not a strategy”?

We’re trying something a little different this week. With no economic data and little in the way of earnings news to speak of today, we’re sending out this week’s Bespoke Report early. Given the volatility in the market lately, we’re sure to miss some big moves throughout the trading day, but they’re unlikely to have a major impact on this year’s trends (famous last words).

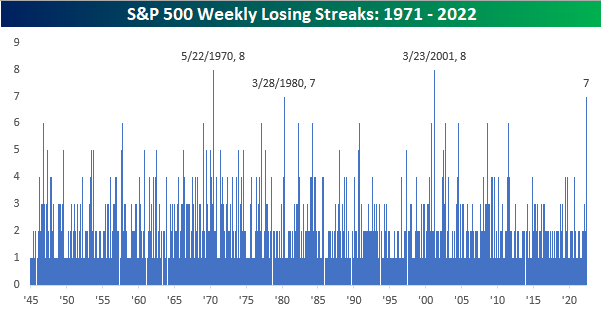

Barring a 3.1% rally on Friday, this week will mark the seventh straight week that the S&P 500 finished the week in the red. That would be the longest streak of weekly losses for the index since March 2001 and just the fourth streak of seven or more weekly losses in the post-WWII period. It’s a small sample size, but these types of streaks haven’t occurred during particularly positive periods for the equity market.

The snippet above is pulled from a page from this week’s Bespoke Report newsletter. If you’re not a Bespoke subscriber and you want to read this week’s full Bespoke Report (and access everything else Bespoke’s research platform has to offer), start a two-week trial to one of our three membership levels.

Bespoke’s Morning Lineup – 5/20/22 – Good Riddance

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You make most of your money in a bear market, you just don’t realize it at the time.” – Shelby M.C. Davis

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

While an up week is pretty much out of the question, can we at least get a positive close to the week? Futures have been higher for most of the overnight session following a larger than expected interest rate cut out of China. Retail earnings have been a big drag on the market this week with Walmart (WMT) and Target (TGT) declines impacting overall confidence. This morning, Ross Stores (ROST) is also down 25% in reaction to its earnings report which cited some of the same issues, but being the third big retailer blowup this week makes it lose some of the shock value. There’s only so much the market can go down on the same issues.

There’s no economic data or Fed speakers on the calendar today, so the market will have to find other excuses in order to whip around between gains and losses.

In today’s Morning Lineup, we recap overnight trading in Asia and Europe (pg 4), Taiwan Export Orders (pg 4), and other economic data out of Europe and Asia (pg 5), and a lot more.

Earnings season is over, and all we can say is good riddance. There weren’t a lot of winners this earnings season, but the list of losers is long. The table below lists each of the S&P 500 companies that experienced earnings reaction day declines of 10% or more over the course of the last three months. In total, 20 companies made the list. Again, these aren’t a bunch of rinky-dink penny stocks, they are some of the largest companies in the world.

Topping the list, Netflix (NFLX) reported weaker than expected revenues and lowered guidance, and in reaction saw its stock lose more than a third of its value in a single day! More recently, just this week Target (TGT) missed EPS forecasts and saw its stock lose nearly a quarter of its value. Some of the other more notable losers include Amazon.com (AMZN) which declined 14.1% while Walmart (WMT) saw its stock decline by more than 11%. GE falling 10% isn’t really a surprise these days, but the fact that it has become so much less relevant in the market than it used to still surprises us. In total, 20 companies – or 4% of the index – saw their stocks decline 10% or more in reaction to earnings over the last three months.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

The Bespoke 50 Growth Stocks — 5/19/22

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. The Bespoke 50 is updated weekly on Thursday unless otherwise noted. There were no changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. You can learn more about our subscription offerings at our Membership Options page, or simply start a two-week trial at our sign-up page.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

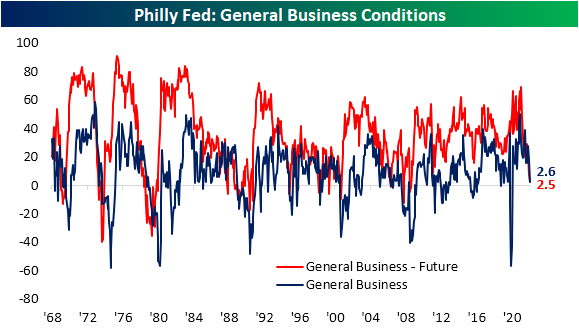

End in Sight For Philly Supply Chain Stress?

On the backs of a disappointing Empire Fed earlier this week, the neighboring Philadelphia Federal Reserve Bank’s own reading on its region’s manufacturing economy also came in well below expectations at the headline level. The index for General Business Conditions was anticipated to decline from a healthy reading of 17 to a more modest 15. Instead, it plummeted to a barely positive reading of 2.6. That would point to a significant moderation in activity in the month of May.

While the headline index fell sharply, the rest of the report was perhaps more mixed. Breadth was certainly weak with only three categories rising month over month (New Orders, Shipments, and Unfilled Orders). As for the indices that declined, on the one hand, some could be perceived as welcome drops with pullbacks in elevated readings of prices and delivery times. On the other hand, the moderation in Number of Employees or CapEx expectations could be taken as a less positive sign for the broader economy.

As shown in the table above, overall most current conditions indices remain historically elevated even after recent declines. Expectations indices meanwhile are generally more depressed with some readings even near record lows. As such, the average normalized distance between the current conditions and expectations categories throughout the report have broken out to the highest level since February 1988 and mid-1975 before that. Put differently, there have rarely been times in which the region’s manufacturers have reported such a dramatic difference between healthy current conditions while also holding a pessimistic outlook.

Taking a closer look at individual categories, New Orders remain well off-peak but ticked higher in May rising 4.3 points to 22.1. There was an even larger jump in expectations, although the level of that index is not nearly as elevated. The modest increase in demand was met with a huge jump in Shipments and Unfilled Orders. With a 16.2 point jump month over month, Shipments are reported to be growing at the fastest rate since the fall of 2020. Given the region’s firms are getting orders out the door at a faster clip, inventories are growing only modestly with that index falling to a barely expansionary 3.2. Additionally, that evidence of improved fulfillment also resulted in a huge drop in expectations for Unfilled Orders. In fact, that index dropped to the lowest level since March 1995. That means the region’s firms expect to work off unfilled orders at a historic rate in the coming months.

The likely reason as to why companies are anticipating such a huge improvement in fulfillment is massive expected declines in lead times. Delivery Times remain elevated but have moderated significantly in the past couple of months. Six-month expectations meanwhile have fallen all the way down to -29.1 which, like unfilled orders expectations, is the lowest level since March 1995.

Another expectations reading that has fallen precipitously in May is CapEx expectations. The reading fell to the worst reading since September 2016 indicating huge moderation in planned investment. Likewise, hiring is expected to slow as has already been observed by the current conditions index. We would note that these readings remain positive, meaning firms are still expecting to take on more hiring and spending on net, but at a more modest rate. Click here to learn more about Bespoke’s premium stock market research service.

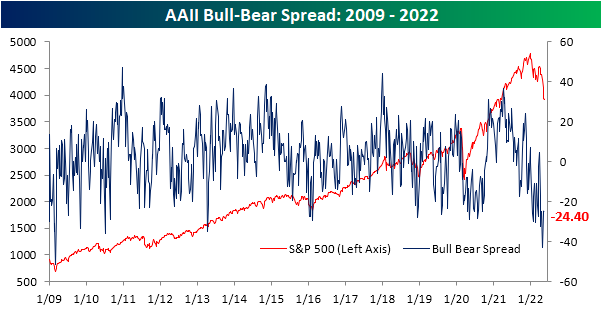

Sentiment Little Changed – Still Bearish

Depending on when a respondent reported their answers to the weekly AAII sentiment survey, they could have been justified in giving either bullish or bearish. From last Thursday’s close to Tuesday, the S&P 500 rallied a little more than 4% but anyone reporting yesterday would have reflected the index giving back all of those gains in a single session. Given that back and forth of equities, sentiment remains little changed. Around a quarter of respondents remain in the bullish camp as has now been the case for three weeks in a row. Albeit a historically low reading, it is a major improvement from readings in the mid-teens only one month ago.

Bearish sentiment meanwhile ticked higher and back above 50% this week. As with bullish sentiment, that is an overwhelmingly pessimistic reading even if it is less extreme than last month when it closed in on a 60% reading.

The bull-bear spread in turn was marginally improved rising from -24.7 to -24.4 indicating sentiment stays heavily slated toward pessimism.

With both bearish and bullish sentiment gaining share this week, the percentage of respondents reporting neutral sentiment fell back below 25% to 23.6%. Click here to learn more about Bespoke’s premium stock market research service.

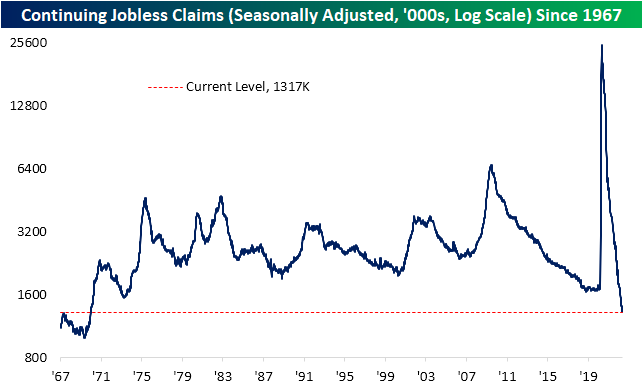

Continuing Claims Keep Falling

Jobless claims have continued to tick higher with this week’s reading rising to 218K. That is an increase of 21K versus last week’s print which was revised back below 200K to 197K. That leaves the seasonally adjusted number at the highest level since January. While there has not been any further improvements, the actual level of claims remains well below the standard historical range near similar levels to the couple of years prior to the pandemic.

Historically, unadjusted claims have fallen week over week more than three-quarters of the time in the current week of the year. However, this year was not one of those occasions as claims rose to 198.7K. While that is not any sort of dramatic increase, it is a somewhat unusual rise a little ahead of when claims have tended to experience a seasonal bottoming out. Looking ahead to the next couple of weeks, claims could see further marginal improvements before resuming a move higher through the early summer.

Continuing claims—which are delayed an additional week to the initial claims number—have been healthier than initial claims as the reading has made yet another multi-decade low per the latest release. Continuing claims are now down to 1.317 million. As low of a reading has not been observed since the last week of 1969. Combined with the uptick in the initial claims number, claims data points to moderating, albeit historically impressive, readings on the number of people filing for unemployment. Click here to learn more about Bespoke’s premium stock market research service.

Post-COVID Gains for Small-Cap Growth Go Poof!

Growth stocks outperformed value stocks by a wide margin in the years leading up to the pandemic. Growth also outperformed value in the first ~18 months after the pandemic, but that trend has been flipped on its head since late 2021. You can see the recent convergence between growth and value in the chart below. Entering 2022, the S&P 500 Growth index was outperforming the S&P 500 Value index by ~40 percentage points since the pre-COVID high for the stock market in February 2020. Now, Growth is only outperforming Value by ~8 percentage points.

The shift from growth to value has been even more dramatic in the more economically sensitive small-cap space. Remarkably, the Russell 2,000 Growth index is now DOWN 6% on a total return basis since the pre-COVID peak for stocks on 2/19/20. Six months ago, this index was still up 45% from its pre-COVID high.

Fed Chair Powell first shifted to a tighter monetary stance in November 2021. In just six months since Powell’s pivot, we’ve seen the entire post-COVID bull market for small-caps give up its gains and then some. And this doesn’t even factor in a double-digit percentage point increase in inflation since COVID began that pushes “real” returns for the Russell 2,000 Growth index much deeper into negative territory. Click here to learn more about Bespoke’s premium stock market research service.