Feb 25, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To devastate is easier and more spectacular than to create.” – Anthony Burgess

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity markets are looking to build on yesterday’s turnaround Tuesday gains and are on pace to erase much of Monday’s losses, but whether these gains stick through the end of the week could depend on Nvidia’s (NVDA) report after the close. It’s widely assumed that the results will be strong, but will they be strong enough? And ff they’re too strong, will that also be interpreted as further future disruption in the software space?

Crude oil is higher this morning, trading just above $66 per barrel, even as Reuters reports that OPEC+ is considering a 137K barrel increase to daily production. Gold is also fractionally higher, back above $5,200 per ounce as silver surges 4% and platinum spikes 8%. Even bitcoin, yes bitcoin, is higher by more than 2%.

Asian stocks finished the day higher across the board, with the Nikkei up over 2% and South Korea up just under 2%. Chinese stocks also traded higher even as the Ministry of Commerce threatened to impose countertrade measures in response to the new tariff policies of the Trump Administration.

In Europe, stocks are also broadly higher but at a more restrained pace. The STOXX 600 is up 0.5%, led higher by 1% gains in Italy and the UK. Eurozone GDP fell more than expected (-0.6% vs -0.5% forecast) and German GDP was in line with expectations, growing 0.3% q/q.

Besides some important earnings reports after the close from NVDA and Salesforce (CRM), it’s a quiet day for data, but we will hear from many Fed speakers, including Barkin, Schmid, and Musalem.

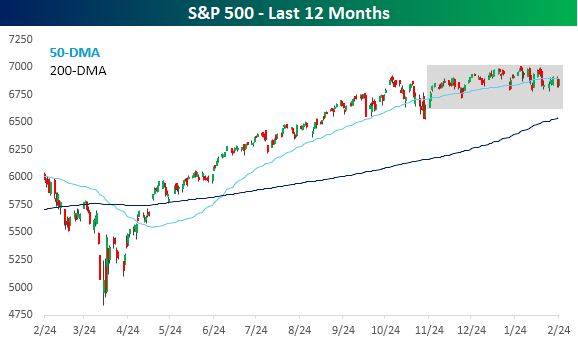

Given the ongoing weakness we have seen in certain areas of the market, which investors now think will be devastated by AI, it’s still hard to believe how range-bound the S&P 500 has been. Yesterday, the S&P 500 closed less than 0.1% below its 50-day moving average. You can’t get much closer than that! And it wasn’t just yesterday. The rangebound morass has been going on for months now, as there hasn’t been a day in the last three months where the S&P 500 closed more than 2.5% above or below its 50-day moving average.

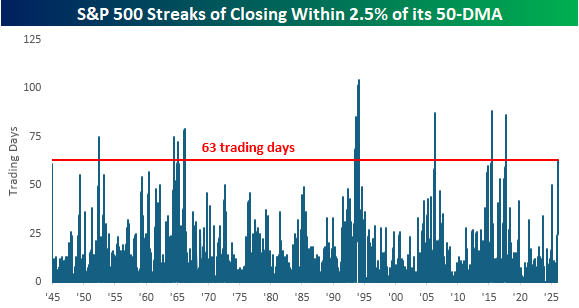

Periods where the S&P 500 has been so closely anchored to its 50-DMA haven’t been all that common throughout history. The chart below shows streaks when the S&P 500 closed within 2.5% of its 50-DMA (above or below), and the current streak, which reached three months (63 trading days) yesterday, is the longest since the first Trump administration in August 2017. Since WWII, there haven’t been many other extended periods where price was consistently so close to its 50-DMA.

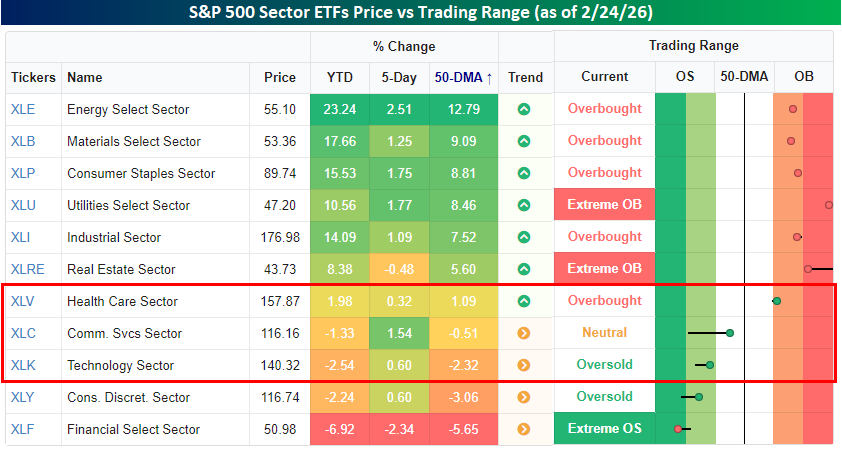

What makes the current streak even more incredible is that most sectors haven’t been showing the same pattern. As of yesterday’s close, just three of eleven S&P 500 sector ETFs – Health Care (XLV), Communication Services (XLC), and Technology (XLK) – closed within 2.5% of their 50-DMAs, and most sectors aren’t even close. Six are more than 5% above their 50-DMAs, and another is more than 5% below its 50-DMA. Like a sleeping volcano, the S&P 500 looks placid from above, but underground, the molten lava bubbles.

Feb 24, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t know what happened. It was just euphoria. I can’t even explain what I was feeling, just pure joy.” – Charlie McAvoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After trading uniformly higher earlier, equity futures are mixed this morning, with the S&P 500 fractionally lower, while the Nasdaq is higher. Investors are still reeling from yesterday’s tech sell-off, as markets start to think that AI-disruption will negatively impact just about every business and sector. Treasury yields are little changed, but at 4.03%, the 10-year yield is near the low end of its range. Crude oil is modestly higher but still hovering around $66 per barrel, while gold is down over 1% and Bitcoin is down another 2% and barely hanging on to $63,000.

In Asia, Japan, South Korea, and China were all firmly higher as the latter returned from the Lunar New Year holiday, while India and Hong Kong were both down over 1%. In Europe, trading has been directionless in early trading with the STOXX up 0.2%, but at the country level, performance has varied between gains and losses.

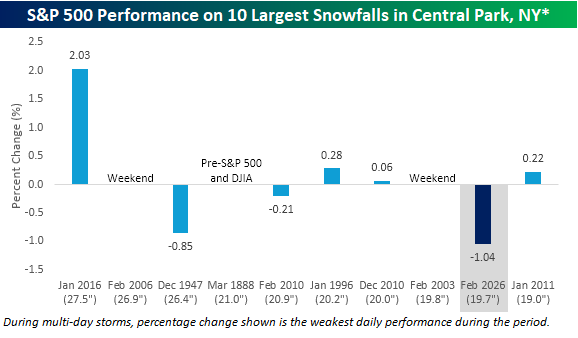

Let’s start with yesterday’s blizzard in the Northeast. With 19.7 inches of snow in New York’s Central Park, it was the ninth-largest snowfall in New York City history. While travel bans were in place around the New York tri-state area, the bears had no trouble getting to work. With the S&P 500 down 1.04%, it was the worst single-day performance for the S&P 500 during one of its ten-largest snowstorms on record. As shown in the chart below, during the prior top ten snowstorms for New York City, the weakest single-day performance during one of these snowstorms was a decline of 0.85% on 12/26/1947.

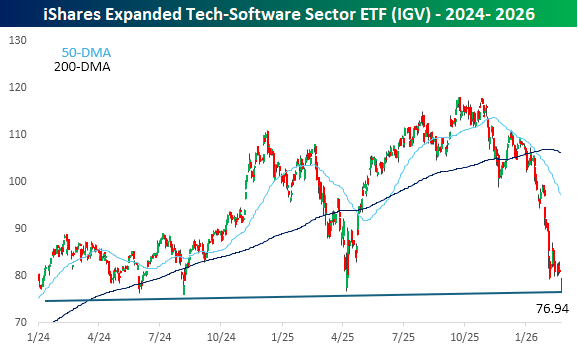

As it has been for some time, the software sector was responsible for much of yesterday’s weakness. The iShares Expanded Tech-Software Sector ETF (IGV) fell close to 5% and to its lowest level on an intraday basis since August 2024 as the lows from earlier this month broke like a hot knife through butter.

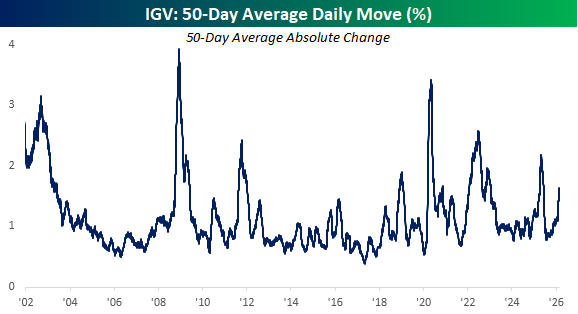

While software has been weak, it hasn’t necessarily been as volatile as you would expect. Over the last 50 trading days, IGV’s average daily change has been a gain or loss of 1.6%. While that’s elevated, it’s hardly anywhere near a historical extreme. Even in early 2025, the average daily change was much higher at over 2%.

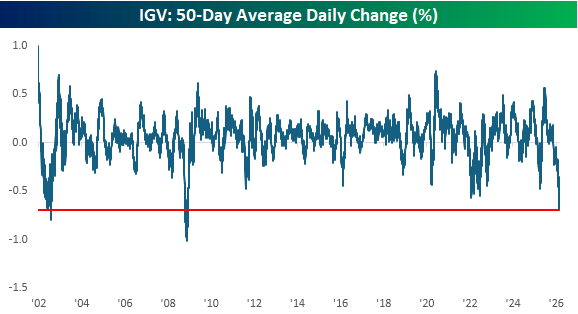

Where the moves in IGV have been extreme, though, is in terms of the average daily percentage change (not the absolute daily change but the average of the trailing 50-day changes). As of yesterday’s close, IGV’s average daily change was a decline of 0.69%, which ranks as one of the most negative readings in the ETF’s history. In fact, the only times that IGV was more of a one-way trade to the downside were during the Financial Crisis and at the end of the dot-com bust.

Feb 23, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t know what happened. It was just euphoria. I can’t even explain what I was feeling, just pure joy.” – Charlie McAvoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Confusion regarding the state of global trade following Friday’s Supreme Court decision striking down the President’s reciprocal tariffs has futures lower to kick off the week. The fact that some form of armed conflict with Iran looks increasingly likely also hasn’t helped. As if that weren’t enough, while the blizzard in the northeast doesn’t have any direct market impact right now, it has effectively paralyzed a central area of economic activity for the day, and air traffic, so it will have some economic impact as well. Crude oil is fractionally higher at close to $67 per barrel; gold is up 2% and looks to be making a new run at its January highs; and silver is up over 5%. Bitcoin, however, is down 2% as some investors are starting to question whether it’s even an effective store of value anymore.

Overnight in Asia, China remains closed for the Lunar New Year, and Japan is also closed, but South Korean stocks traded up nearly 1%, which nowadays doesn’t even register as an impressive move. In Europe, the STOXX 600 is down modestly in a mixed session where Italy and Spain are both up roughly 1% while Germany dips about 0.5%. The disparate performances stem from strength in banks and weakness in industrials (more German-focused).

Datawise, there’s not a lot on the calendar today. At 8:30, we got the Chicago Fed National Activity Index. That will be followed by Factory Orders at 10, and the Dallas Fed at 10:30. Fed Governor Waller is also speaking this morning, and he’s on the wires saying that a March rate cut will depend on the state of the labor market, which he sees as likely remaining weak going forward, citing potential pressures from AI.

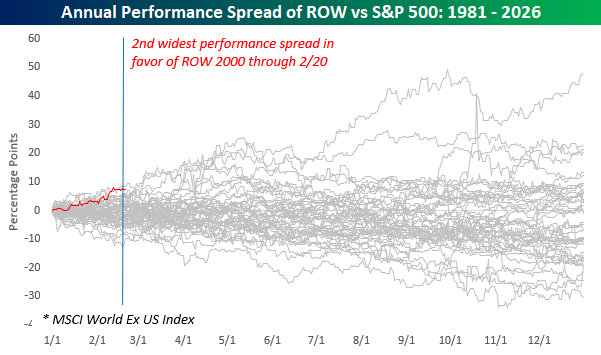

The US is on top of the hockey world this morning after Sunday’s dramatic OT win, and investors are hoping some of those gold-medal vibes rub off on the stock market. As we highlighted in Friday’s Bespoke Report, through the first several weeks of 2026, US stocks have underperformed stocks from the rest of the world to a near-historic degree. As shown in the chart below, the only year since 1980 when the S&P 500 underperformed the rest of the world by a wider margin was in 1984, and barely at that.

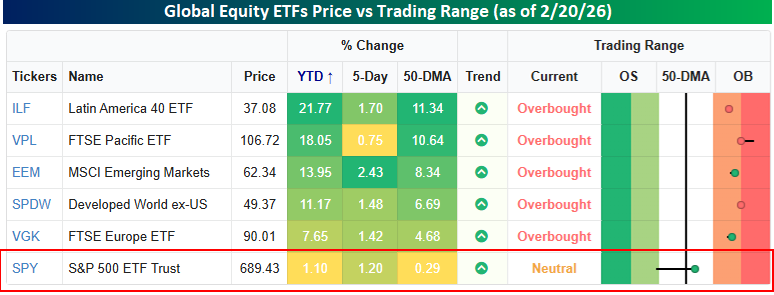

The graphic below puts the short-term US underperformance into even better perspective. Major international regional equity ETFs headed into the weekend on power plays at overbought levels (1+ standard deviation above their 50-DMAs), while the US was short-handed in penalty-killing mode and scrapping to get back above its 50-day moving average. YTD, European equities, as measured by the FTSE Europe ETF (VGK) were outperforming the S&P 500 by more than six full percentage points, but the other four regional ETFs shown were all outperforming by at least 10 full percentage points, with Latin America (ILF) outperforming by 20 percentage points – in less than two months! How the lines have shifted!

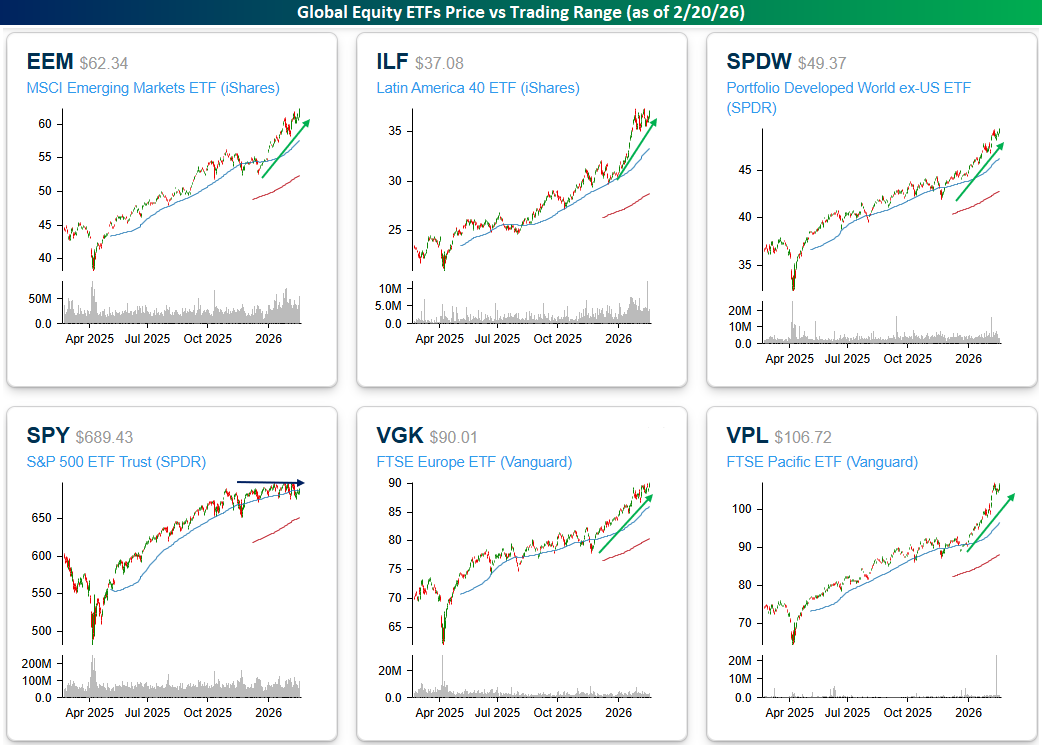

A look at the six price charts also shows the disparity between US and international stocks. Five of the charts shown are in clear, well-defined uptrends, while the US has been stuck in neutral between the blue lines, unable to push the puck into the zone, but also successfully fighting off any bearish attacks into their defensive zone.

Feb 20, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have a theory that the truth is never told during the nine-to-five hours.” – Hunter Thompson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Ahead of a busy economic data day and possibly an important Supreme Court ruling, equity futures are modestly lower across the board, with the S&P 500, Nasdaq, and Dow all indicated lower by about 0.20%. The 10-year yield is down close to two basis points to 4.06%, and crude oil is fractionally lower as comments from the President suggest that if there is going to be a strike against Iran, it won’t come this weekend, and even if there is, it’s likely to be targeted initially. Gold prices are up 1% and back about $5,000, and Bitcoin is also fractionally higher.

Japanese stocks traded 1.1% lower and closed out the week with a modest decline, and the Hang Seng traded down by the same amount. South Korean stocks bucked the trend, though, and rallied more than 2%, finishing the week up 5.5% in just two days of trading!

European stocks are finishing the week on a more positive note, with the STOXX 600 up 0.4% and taking its WTD gain to more than 1.5%. Every major index in the region is higher on the session, and except Germany, they’re all up over 1% for the week. Flash PMI for the manufacturing sector was better than expected, while the Services PMI was slightly weaker. On the inflation front, PPI in Germany showed an unexpected decline of 0.6% versus forecasts for an increase of 0.3%.

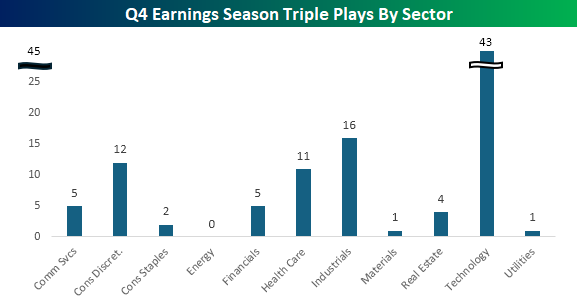

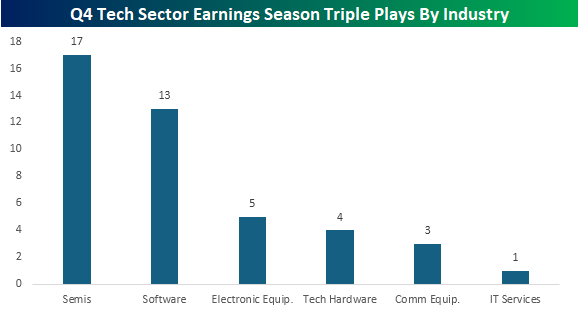

Yesterday marked the unofficial end of earnings season, with Walmart (WMT) reporting before the open. While the equity market had a muted to modestly negative performance this earnings season, there were plenty of earnings triple plays (companies that reported better than expected earnings and revenues and raised guidance). Since earnings season started in early January, 100 companies reported triple plays, and in the chart below, we break those names out by sector.

While it’s been one of the worst-performing sectors this year, the Technology sector has easily had the most earnings triple plays with 43. That’s more than double the next closest sector – Industrials, and is also more than the total of the other top four sectors combined! At the other end of the spectrum, not a single stock in the Energy sector reported a triple play, while the Materials and Utilities sectors each had one apiece.

Within the Technology sector, it’s also interesting to look at where the Triple Plays have come from. Leading the way, 17 of the tech sector Triple Plays have come from semiconductor companies, which should come as no surprise, given the group’s performance this year. Next on the list, though, is software with 13 stocks. Even as the group has been slaughtered this year, there’s no shortage of companies in the group exceeding results and raising guidance. This illustrates again that while these companies may not yet be feeling the impact of AI on their businesses, it’s the long-term that investors are more worried about.

Feb 19, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To know that we know what we know, and to know that we do not know what we do not know, that is true knowledge.” – Nicolaus Copernicus

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It looks like a sluggish start to the trading day with S&P 500 futures down about 0.25% while the Nasdaq is down closer to 0.40%. Walmart (WMT) reported earnings earlier, and the stock is down over 2.5% after giving disappointing guidance. WMT’s reaction to earnings encapsulates the entire earnings season, where stock price reactions and the overall market performance have been modestly disappointing.

Treasury yields are higher again this morning as the 10-year yield moves above 4.10% just two days after it looked like we’d be trading with a 3-handle. Crude oil prices are rising again, with WTI up over $66 as investors watch the Middle East, where a US military strike against Iran looks increasingly likely. Gold prices are basically flat, while crypto is down modestly.

In Asia, China remained closed for the Lunar New Year, but South Korean stocks surged over 3% while the Nikkei rallied 0.6% after Core Machinery Orders rose more than 19% versus forecasts for an increase of 5.1%. Europe is following the US tone rather than Asia this morning, and the STOXX 600 is down 0.6%, led lower by Italy’s decline of 1.3%.

On the economic calendar, it’s been a busy morning, with the main reports being the Philly Fed Manufacturing report, which came in better than expected (+16.3 vs +7.5), and jobless claims. Initial claims were lower than expected at 206K versus forecasts for 225K, while continuing claims were slightly higher than expected at 1.869 mln versus forecasts for 1.860 million. For the rest of the day, the only remaining reports of note are Leading Indicators and Pending Home Sales at 10 AM

With Walmart’s report this morning, Q4 earnings season is now winding down to an unofficial close. We measure earnings season performance as the five weeks starting with the Friday before the large banks start to report, which for the current earnings season works out to the period from the close on 1/9 through 2/20. As of yesterday’s close, the S&P 500 was down 1.2%, and with futures down this morning, it would take a decent reversal and a rally tomorrow to push the S&P 500 into the green for this earnings season.

A negative earnings season would break a streak of five straight earnings seasons during which the S&P 500 had positive returns during earnings season. Even more notable is that the last time the market declined more than 1% during an earnings season was 15 quarters ago (nearly four years) during the Q1 2022 reporting period, when the S&P 500 fell more than 13%.

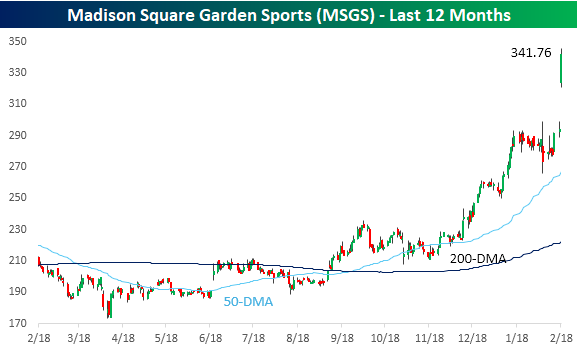

At the stock level, yesterday’s big story was news that Madison Square Garden Sports (MSGS), which owns the New York Knicks and New York Rangers, was considering a plan to separate the two franchises into two standalone companies. The stock rallied more than 15% in response, and deservedly so, as even after yesterday’s rally, MSGS has a market cap of less than $9 billion, and the combined value of both teams is estimated at well over $10 billion.

MSGS has been a solid performer over the last year as many investors started to anticipate this type of announcement from the company, and even before yesterday’s news, the stock was up over 42% in the last year. After yesterday’s surge, MSGS is up over 65%.

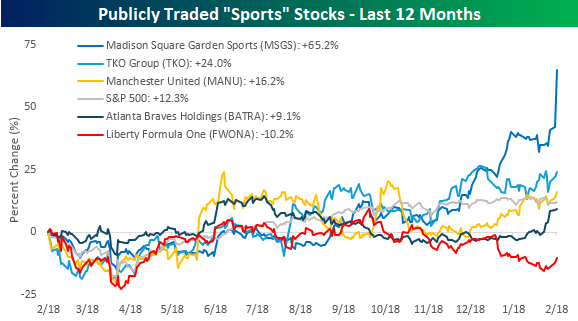

Owning sports franchises has become a popular investment strategy in recent years as their value has skyrocketed in the last couple of decades. Private equity funds have been rushing into the space, but as is usually the case for emerging investment trends, access for individual investors is tough. In the public equity space, there’s only a handful of stocks that primarily track the performance of individual sports teams or leagues.

The chart below shows the performance over the last year of five publicly traded stocks that provide exposure to individual sports franchises or an entire league. While it’s been a popular investment strategy among the limited options available to individual investors, performance over the last year has been mixed.

Even before yesterday’s surge, shares of MSGS were the top performer, and they only added to the gains yesterday. Trailing MSGS, TKO Group (TKO), which owns the UFC and WWE, was up 24%, which also handily outperformed the S&P 500. Next on the list was Manchester United (MANU), and its 16.2% only modestly outperformed the S&P 500. While three of the five stocks have outperformed the S&P 500 over the last year, shares of Liberty – Atlanta Braves (BATRA) are up just 9.1%, while shares of Liberty Formula One (FWONA) have “crashed and burned” 10.2%. While Formula One is billed as one of the fastest-growing sports these days, its stock price has gone the other way.

Feb 18, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You just have to find that thing that’s special about you that distinguishes you from all the others, and through true talent, hard work, and passion, anything can happen.” – Dr Dre

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equities are poised to open higher this morning, but futures are well off their overnight highs. As things stand, the S&P 500 is on pace for a 0.35% rally at the open while the Nasdaq is up 0.45%. The 10-year yield is up less than a basis point, but with the yield over 4.06%, it’s well off its intraday low of under 4.02% yesterday. Oil prices are up over 2.5% as markets remain on edge over the possibility of military action in Iran. That has also helped to push gold prices up over 1%, even as they remain under $5,000 per ounce.

While most of Asia remains closed for the Lunar New Year, Japanese markets were open for trading, and the Nikkei rallied 1% as export growth came in stronger than expected. The country’s trade minister also announced the first tranche of investments for US infrastructure projects, which was part of the trade deal.

In Europe, we’re also seeing broad-based strength with the STOXX 600 up just under 1%, led higher by Spain and Italy. There’s no real catalyst behind the gains, but UK and French CPI data were generally inline with expectations.

There’s a busy schedule of economic data today, kicking off with Durable Goods (better than expected), Building Permits (better than expected), and Housing Starts (better than expected) at 8:30, followed by Industrial Production and Capacity Utilization at 9:15 followed by Leading Indicators at 10:00. At 2 PM, we’ll also get the Minutes from the January FOMC meeting, and in between Fed Vice Chair Bowman will be speaking in DC at 1 PM Eastern.

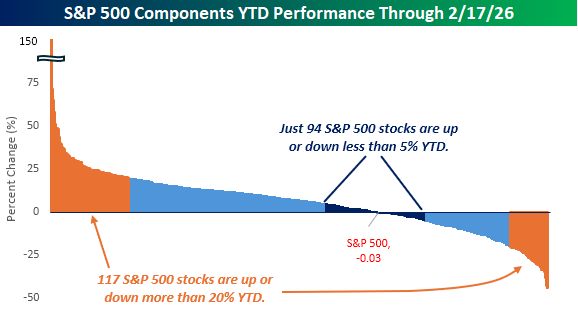

There have been 31 trading days so far in 2026, and for many, it’s been an exhausting year in the markets. For all the sound and fury, though, consider this. On 12/31, the S&P 500 closed at 6845.50. Yesterday, it closed at 6843.22. Just two points lower! For the year, the S&P 500 is down just 0.03%!

On the one hand, the S&P 500’s inability to make any headway this year (and over the last five months, for that matter) is enough to make you want to rip your hair out, but after the rally the market had off the April lows, some consolidation was in order, so you could say this is exactly what the market needed.

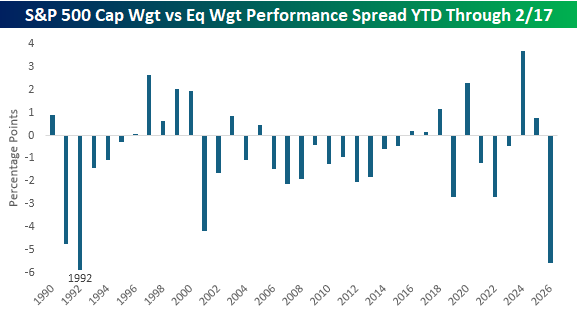

While there’s been nothing going on at the index level, underneath the surface, we’ve seen massive rotation. While the S&P 500 is flat on the year, just 94, or less than 20% of the index’s components, are up or down less than 5%. At the extremes, though, 117 stocks are up or down at least 20% YTD! It seems that Washington isn’t the only place where we’ve seen an increase in concentration at the extremes with nothing to show for it.

While the big moves in individual components of the S&P 500 haven’t shown up at the index level, on an equal-weighted basis, the S&P 500 has much more to show for it this year as it’s up 5.5% YTD. With that gain, the S&P 500 cap-weighted index is underperforming its equal-weighted peer by 5.53 percentage points YTD. Since 1990, the only other year when the cap-weighted index underperformed the equal-weighted index by a larger amount was in 1992. In that year, the outperformance of the equal-weighted index continued through the rest of the year, but both indices were up more than 5% from that point through year-end.