Jul 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Don’t confuse schooling with education. I didn’t go to Harvard, but the people that work for me did.” – Elon Musk

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a mixed picture for US equities this morning, as Dow futures are poised to open down by about 0.4%, while the S&P 500 and Nasdaq are indicated to be higher. Helping to drive the gains in the Nasdaq and S&P 500, shares of Alphabet (GOOGL) are up over 3% after the company reported better-than-expected earnings and sales. To the downside, Tesla (TSLA), another trillion-dollar stock, or at least as of the close yesterday, is down 6% after CEO Elon Musk warned of “a few rough quarters” ahead.

The mixed picture for US stocks follows a positive session in Asia, where the Nikkei rallied over 1.5% while Chinese stocks also finished the session in positive territory as trade deals start to emerge. European equities were also positive on prospects of trade deals ahead of the August 1 deadline. Flash PMI readings for July came in roughly in line with expectations. The ECB also announced its latest policy decision, and as expected, there was no change in rates.

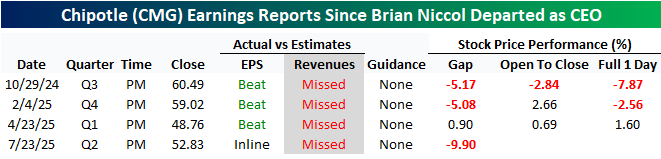

Turning back to the US, another CEO, like Elon Musk, who didn’t go to Harvard, is the current Starbucks (SBUX) CEO and former Chipotle (CMG) CEO Brian Niccol. Since it was announced that the Miami University (Ohio) alum would be leaving Chipotle for Starbucks, the former’s stock has had a rough go, and its four earnings reports since then haven’t been particularly positive either.

After the close yesterday, CMG reported inline EPS on weaker-than-expected revenues. The revenue miss was the fourth straight time it missed top-line expectations, and the stock is on pace to gap down close to 10% at the open this morning. Besides the four straight sales misses, CMG will have now gapped down 5%+ in reaction to three of its last four earnings reports.

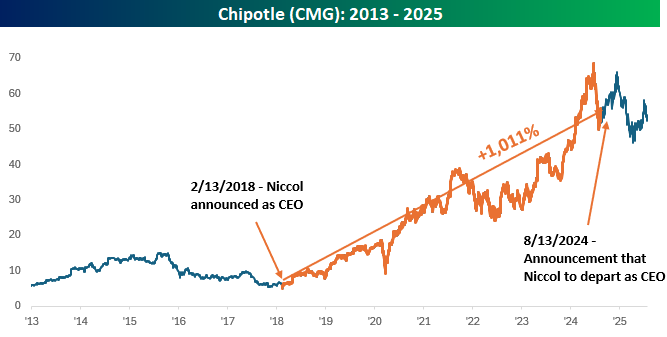

Including this morning’s decline, shares of CMG are down over 15% since it was announced that Niccol would be leaving the company. Over that same period, the S&P 500 is up over 18%. All of this also comes after the stock rallied more than 1,000% during Niccol’s tenure as CEO. Whether all of CMG’s problems are a result of Niccol’s departure or he saw the writing on the wall could be up for debate, but his timing was impeccable, further burnishing his reputation. He came into the company just as it was reeling from food safety incidents in 2018, and while he didn’t get out right at the top, he didn’t miss it by much.

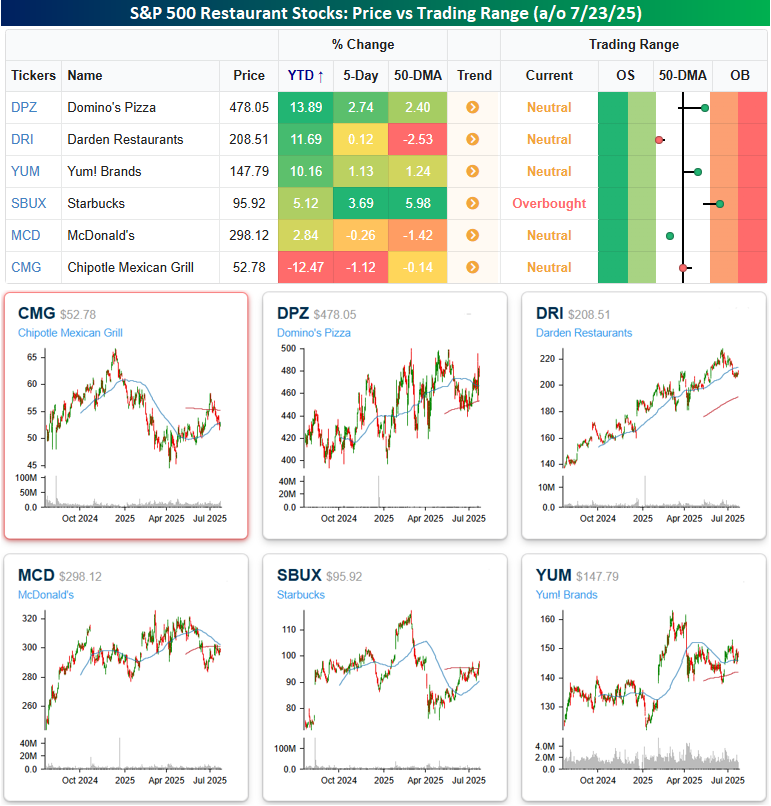

The snapshot below from our Trend Analyzer compares CMG to other restaurant stocks in the S&P 500. As of the close yesterday, stocks in CMG’s peer group were all up on the year, but CMG was down well over 10%, and that doesn’t even take into account this morning’s weakness.

Looking at the charts of all six stocks, CMG is also an outlier as no other stock in its group is closer to a 52-week low. SBUX is the second furthest from a 52-week high, so Niccol’s magic doesn’t appear to be coming through just yet.

Speaking of SBUX, the stock has been stuck in a range for the last five years. Just as it was announced nearly a year ago that Niccol would be taking over the company, SBUX was testing the low end of its multi-year range. Since then, the stock has rallied 25%, which is modestly better than the S&P 500, but outside of a brief period earlier this year, the downtrend from its post-COVID high remains intact. Since it was announced that Niccol would be taking over as CEO last August, SBUX has reported weaker-than-expected EPS and revenues in two of the last three quarters, so his move to the CEO seat has yet to show any meaningful impact on results, but the next opportunity will be next Tuesday.

Jul 23, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Restlessness is a fickle catalyst; it can drive you to achieve or it can coax your demise” – Slash

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The deals are starting to come in. Last night, President Trump announced a trade deal with Japan, which will set tariffs on imports from the country into the US at 15% (more details in today’s Morning Lineup). Futures are higher in response, with the biggest gains coming in the Dow while Nasdaq futures are just marginally higher.

Asian stocks surged in response to the news, with the Nikkei rising over 3% while other markets in the region saw broad gains. Japanese automakers have been the biggest winners with gains of over 10%. The positive sentiment from the trade deal with Japan has seeped into European trading as the STOXX 600 is up about 1%

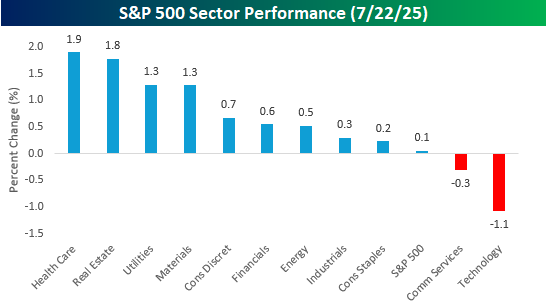

Yesterday was a strange day for the market. While the S&P 500 finished the day with a fractional gain of 0.06%, four sectors traded up more than 1% on the day, and nine of eleven sectors finished the day higher. The only two sectors to finish lower on the day were Technology (-1.1%) and Communication Services (-0.3%). As another example, while the S&P 500 was barely up, the equal-weighted index was up over 1%. You don’t see that very often!

Given the strong breadth at the sector level, individual stock breadth was also very positive as the S&P 500’s net advance/decline reading was +314 – the strongest since June 6th! Going back to 1990, it was just the ninth time that the S&P 500 had a daily breadth reading of +300 or more on a day when the S&P 500 finished up by less than 0.5%. Yesterday was also the smallest gain of those nine prior days (and there has never been a day when net breadth was +300 and the S&P 500 finished down on the day).

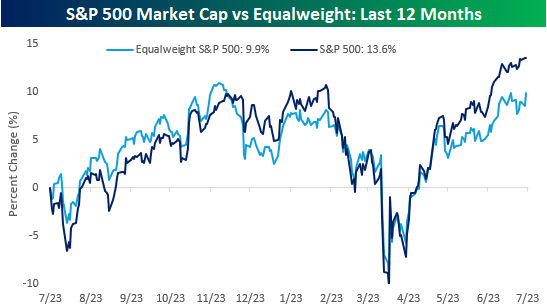

Checking up on the performance of the S&P 500 market-cap-weighted index versus the performance of the equal weight index, even after yesterday’s improvement in the equal weight index, the cap-weighted index has handily outperformed over the last year. While the performance gap between the two indices is wider now than at any point in the last year, it’s interesting to note that as recently as early May, the equal-weight index was outperforming the cap-weighted index. It just goes to show that trends can be quick to change, especially in the market.

Jul 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“My buddies wanted to be firemen, farmers or policemen, something like that. Not me, I just wanted to steal people’s money!” – John Dillinger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s a negative bias in equity futures this morning as investors digest what has been a monster run, especially in some of the more speculative areas of the market. You can’t fault investors for taking a step back to catch their breath as earnings season picks up and we approach the August 1st tariff deadlines. Treasury Secretary Scott Bessent stated in an interview this morning that August 1st is a firm deadline, after which tariff rates will revert to the April levels for any country where a deal has not been reached. Once again, the Treasury Secretary is promising lots of deals, but so far, there has been little substance.

European stocks are also weak again this morning, with the STOXX 600 down 0.6% with Germany leading the way lower with a decline of 1%. In Asia, equities had a more mixed showing with Japan down fractionally (after being closed yesterday) while China finished about 0.5% higher.

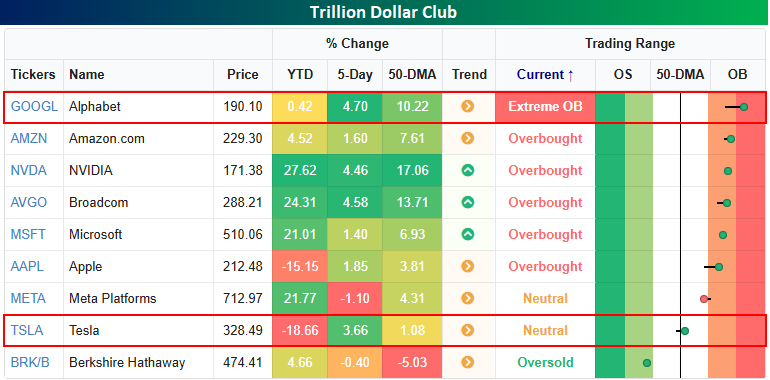

We’re in the second full week of earnings season, but the first of the big guns will kick things off tomorrow when Alphabet (GOOGL) and Tesla (TSLA) report after the close. In TSLA’s case, the stock is down nearly 20% on the year and closed yesterday just barely above its 50-day moving average, so expectations for the stock are pretty low. GOOGL is a bit of a different story. Of the now nine stocks with trillion-dollar market caps (a trillion isn’t what it used to be!), GOOGL is the only one trading at ‘extreme’ overbought (2+ standard deviations above its 50-DMA) levels, so on a short-term basis, expectations for the stock are on the high side. Longer-term, however, GOOGL has been an underperformer this year, with just a fractional gain, making it the third-worst performer of the “Noble Nine”.

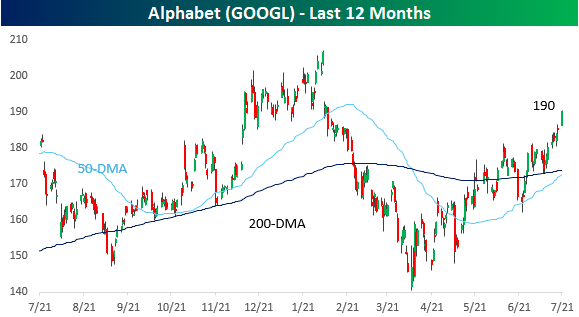

Looking specifically at GOOGL, even with the stock trading at extreme overbought levels, it remains right in the middle of the range it has occupied for the last year, with a low end just below $150 and a high end at just above $200. While GOOGL was the first mega-cap to brand itself as an AI-first company, the stock has been a battleground between those who say it missed the boat on AI and those who say it’s just taking its time.

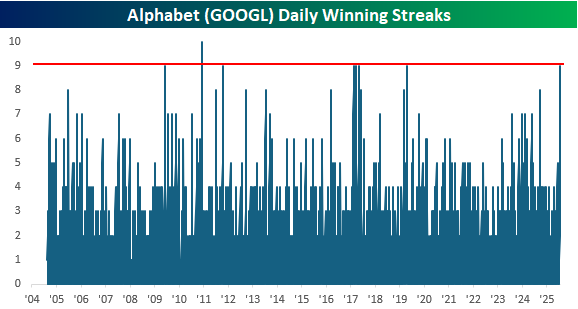

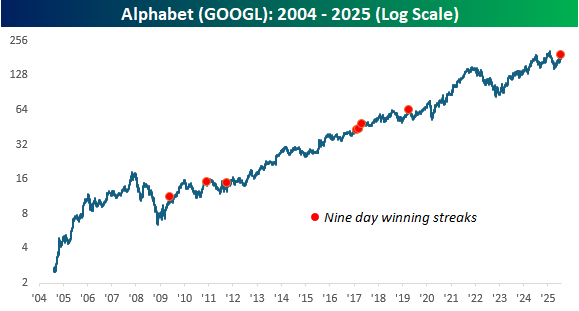

Besides closing at extreme overbought levels yesterday, GOOGL also finished the day higher for the ninth day in a row. That’s just one day shy of the longest streak in the stock’s history since its IPO in 2004 and the longest winning streak in more than six years.

The chart below shows the long-term performance of GOOGL with each red dot indicating a 9-day winning streak. While none of these streaks occurred at or near a long-term peak in the stock (there haven’t been many), many occurred near a short-term peak.

Jul 21, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Happiness in intelligent people is the rarest thing I know.” – Ernest Hemingway

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Stocks are poised to open the week higher this morning as we gear up for a busy week of earnings. The only economic indicator on the calendar this morning is Leading Indicators at 10 AM. In terms of earnings, we’ve already gotten reports from Cleveland Cliffs (CLF), Domino’s Pizza (DPZ), Roper (ROP), and Verizon (VZ). The only one of the four that missed EPS forecasts was DPZ, while it was the only one to miss estimates (barely) on the top line. After the close, the most notable reports on the calendar are Crown (CCK), NXP Semiconductors (NXPI), Steel Dynamics (STLD), and WR Berkley (WRB).

Outside of the US, Asian markets were mostly higher, while Japan was closed. Japan’s ruling party lost its majority in the weekend elections. While Asia was mostly higher, Europe is sitting on some modest losses in early trading with the STOXX 600 down 0.2%. Trade and tariffs continue to dominate the headlines there as the August 1st deadline approaches, and President Trump is pushing for 15% to 20% tariffs on all European imports.

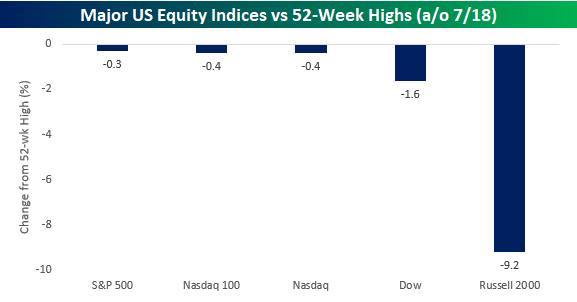

While the S&P 500, Nasdaq 100, and Nasdaq Composite all closed out the week within 1% of 52-week highs last Friday, the Dow Jones Industrial Average remains a little further off at 1.6%. The small-cap Russell 2000 remains in a league of its own, near correction territory at 9.2% below its 52-week high. Not all US equity indices are created equal.

At the sector level, the haves vs have-nots is even more pronounced. Last Friday, just three sectors – Utilities, Technology, and Industrials – closed within 1% of their respective 52-week highs. After these three, Financials, Communication Services, and Consumer Staples closed out the week between 1% and 5% below their respective 52-week highs.

Nearly half of the S&P 500 sectors, however, remain more than 5% from their respective highs, including Energy (-11.7%) and Health Care (-16.3%), which are still deep in correction territory. While the Energy sector’s weight of 2.97% in the overall index is nearly inconsequential, the Health Care sector still has a respectable weighting of right around 9%.

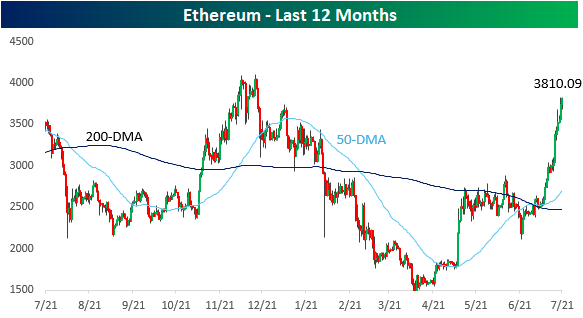

Outside of equities, the crypto space has been strong, and here, there’s been a relative rotation where the formerly overlooked Ethereum has been surging. After trading at $1,500 in April and below $2,500 as recently as July 4th, Ethereum is back up above $3,800 for the first time this year.

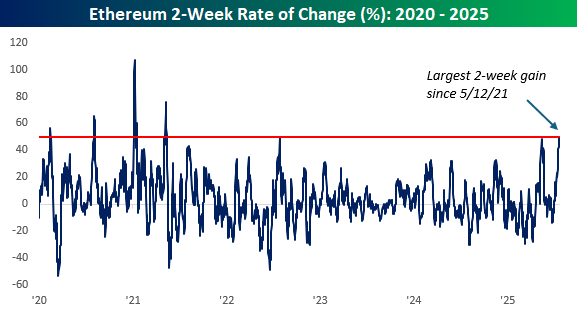

Based on where it’s trading this morning, Ethereum has rallied just over 50% in the last two weeks, which would put it on pace for the largest 14-day gain (crypto doesn’t take weekends off) in more than four years.

Jul 18, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life is a helluva lot more fun if you say yes rather than no” – Richard Branson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s little action going on in equity futures this morning as the market looks to close out what was an important week in terms of economic and earnings-related data on a positive note. Heading into the final session of the week, the Nasdaq is up 1.5% week to date while the S&P 500 is up a more modest, but still respectable 0.60%.

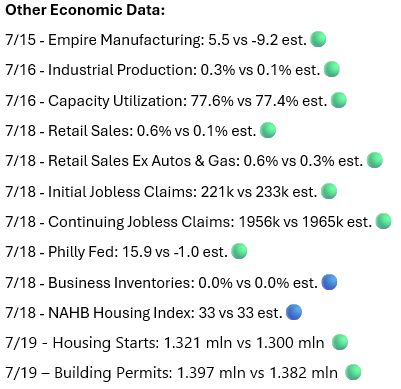

There are only a handful of earnings reports this morning, but some of the more notable ones were 3M (MMM), American Express (AXP), Charles Schwab (SCHW), and SLB. All four companies managed to top expectations on both the top and bottom line, continuing what has been a positive start to the Q2 earnings season. On the economic calendar, we’ll close the week with Housing Starts and Building Permits at 8:30, followed by Michigan Confidence at 10.

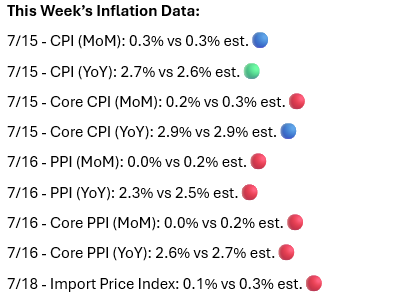

As mentioned, it was a significant week for economic data, particularly in terms of inflation, and the results came in just about as good as anyone could have hoped for. Of the nine different major metrics for the week, the only one that came in higher than expected was headline CPI on a y/y basis.

While most of the inflation-related data came in lower than expected, other data for the week were nearly across the board better than expected. Not a single report missed expectations, and the only reports that didn’t top expectations were Business Inventories and Homebuilder Sentiment.

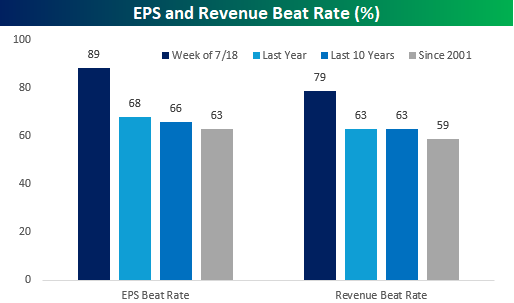

We’re only a week into earnings season, but the reporting period has gotten off to a strong start. 89% of the more than 75 companies that reported earnings this week topped EPS forecasts, and 79% exceeded sales estimates. Relative to the average EPS and sales beat rates over the last one and ten years, as well as going back to 2001, the readings for this earnings season are significantly better than expected.

Jul 17, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“All money is a matter of belief.” – Adam Smith

Often hailed as the father of modern economics, Adam Smith (who died on this day in 1790) profoundly shaped our understanding of free markets and individual liberty through his seminal works, The Wealth of Nations and The Theory of Moral Sentiments. His ideas on the “invisible hand” and division of labor remain foundational to economic theory, emphasizing how self-interest and cooperation drive prosperity.

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

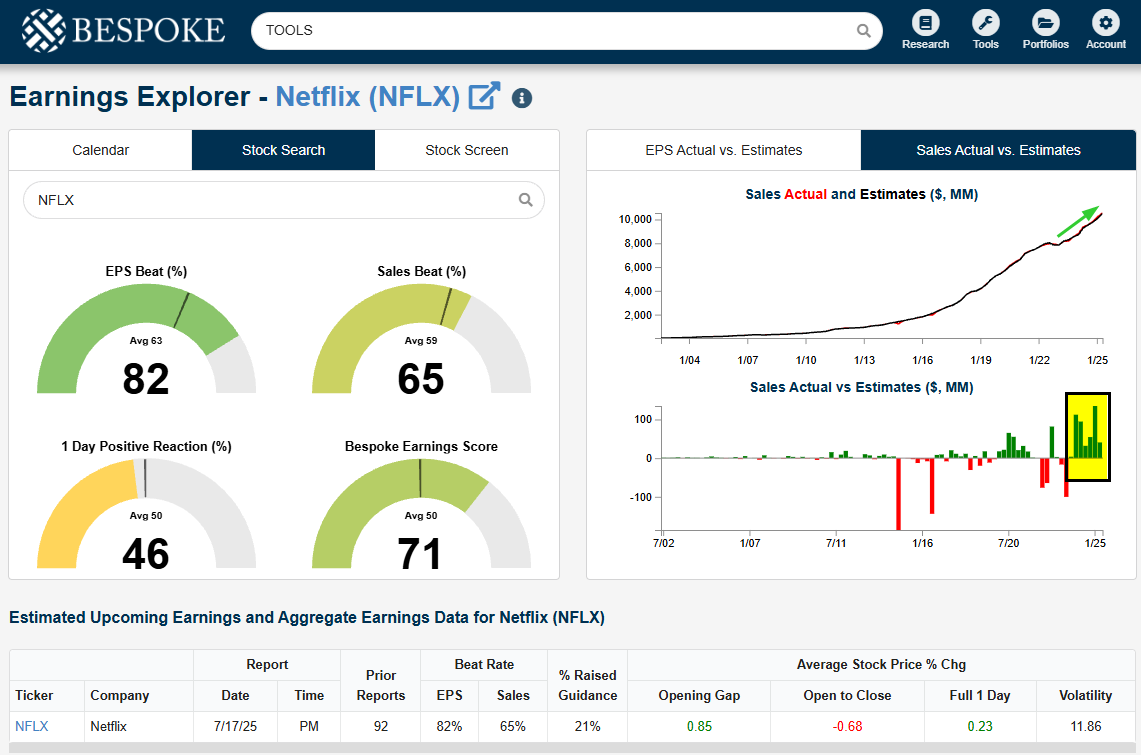

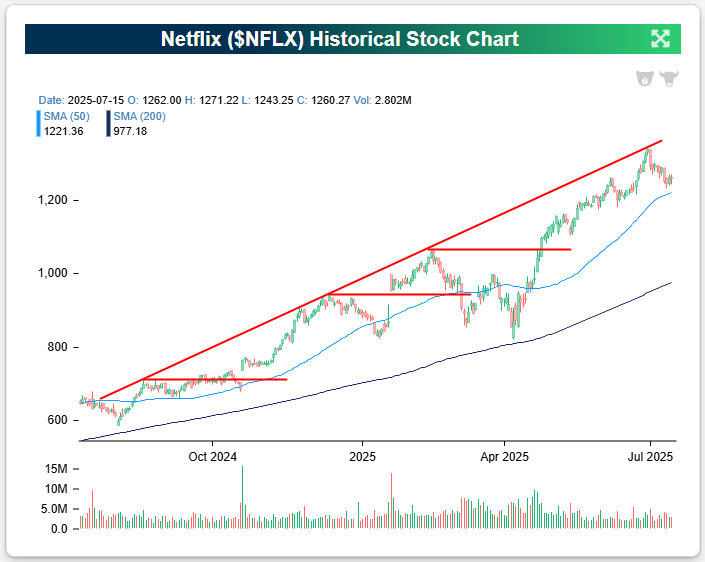

The banks and brokers always kick off each earnings season, but Netflix (NFLX) is the company that gets things started on the Tech/Consumer side of things. As shown below, NFLX is heading into its Q2 earnings report tonight in a long-term uptrend, but it has pulled back some in the past couple of weeks after touching up against the top of its one-year uptrend channel at the end of June. At the moment, it’s sitting just above support at its 50-day moving average after working off overbought levels.

Below is a snapshot of Netflix (NFLX) from our Earnings Explorer tool, which can be seen on our website here for those with access (Institutional only). After stumbling on sales a few years ago in 2022, NFLX has seen a revenue resurgence with strong beats versus top-line estimates for six straight quarters. If estimates are met, this will be the third straight $10+ billion quarter for NFLX and the first above $11 billion.

There is some negative historical precedent for Netflix’s Q2 earnings reports specifically, though…