Nov 3, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It would be a mistake to think something is wonderful just because it looks great.” – Anna Wintour

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last week may have been the peak week of earnings season in terms of the market cap of companies reporting, but we have another busy week in store for investors, and it’s picking up right where it left off last week. Of the companies reporting so far today, 89% have reported better than expected EPS forecasts, and 75% have topped sales forecasts, so you can’t ask for much more than that. Even in terms of guidance, 3 companies have raised forecasts while only one lowered.

In response to the better-than-expected reports, equity futures are also picking up right where they left off last week, as markets look to open the week higher with the Nasdaq leading the way. Today’s positive open for the Nasdaq will be the ninth straight positive start to a week for the index, which is only the longest streak since summer 2024, but still tied for the second longest in the index’s history.

In Asia, Japan was closed for the day, but other indices in the region were broadly higher even as South Korea’s manufacturing PMI moved into contraction territory. In Europe, most manufacturing PMIs were also in line with forecasts, and the STOXX 600 responded by rallying 0.5% while Germany rallied more than 1%.

Outside of equities, the 10-year yield is slightly lower at 4.09% ahead of a busy week for Fed speakers, who have mostly sounded more skeptical of a December rate cut, as concerns over inflation linger even as there are signs that the labor market is stabilizing.

Crude oil prices are essentially unchanged even as OPEC+ announced over the weekend that it would increase output by 137K barrels per day, but then pause those increases beginning in January. WTI is starting the month just over $60 per barrel after declining 2% in October, taking its monthly losing streak to three months.

Gold prices are starting off the month back above $4,000 per ounce as other metals also trade higher, but the troubles for digital gold continue as bitcoin prices trade down close to 2% and barely hangs on to $108K. Ethereum prices are down twice as much as they barely hang on to $3,700.

With just two months left in the year, over the weekend, we looked at asset class performance, country performance, and individual stock performance for October and various other time periods. Make sure to take a look at that rundown of where things stand heading into year-end. Even though the major averages may be looking good, not everything looks great.

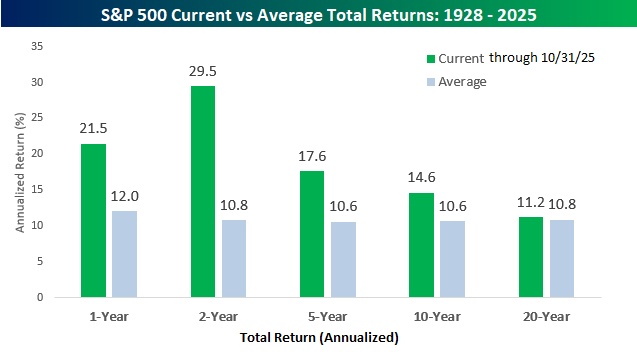

Taking a high-level look at equity market returns, whether you’re looking at the short-term or long-term, it has been a friendly environment. Over the last year, the S&P 500’s total return has been a gain of 21.5% which is nearly twice the historical average of 12.0%, but over the last two years, the 29.5% annualized gain has been nearly triple the long-term average. Looking out over longer-term time periods, though, over the last five, ten, and twenty years, returns aren’t as strong, but they’re still above the long-term average.

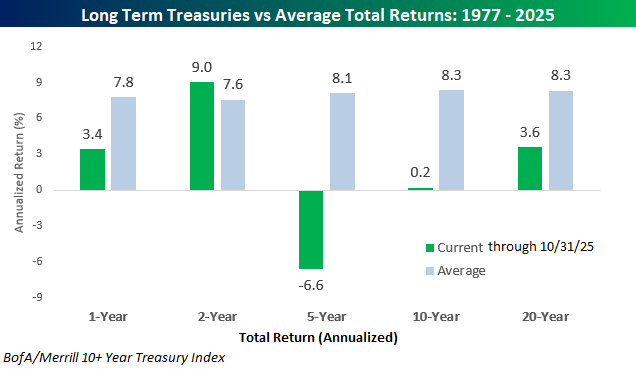

While equity market investors have been on a highway paved in green, the treasury market has been a world of pain. Over the last year, long-term treasuries, as measured by the BofA/Merrill 10+ Year Treasury Index, have posted positive returns, but at 3.4% it’s still less than half of the long-term average. Over the last two years, the annualized gain of 9.0% is actually slightly above average. Still, looking back further than that, it’s been a painful five, ten and twenty years for anyone who has loaned money to the US Treasury.

Oct 31, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The work of today is the history of tomorrow and we are its makers” – Juliette Gordon Low

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view yesterday’s CNBC interview talking about market breadth, click on the image below.

The S&P 500 heads into today with just fractional gains for the week, but today’s trading should add to those gains with futures indicated 0.7% higher. Strong earnings from the mega-caps are to thank for the gains, as what has already been a positive earnings season continues. Outside of equities, treasury yields are slightly higher, while crude oil trades slightly lower but has hung on to $60 per barrel for now. Metals prices are mixed as gold hangs on to $4,000 while silver and copper are essentially unchanged. Crypto is showing some life as Bitcoin trades higher by 3% and Ethereum rallies closer to 5%.

In Asia overnight, markets were mixed. Japan, China, and South Korea all closed out the week higher and with solid gains for the week, but Hong Kong and India were both lower. The biggest economic datapoints of the session were PMI readings in China as the Manufacturing index slid further into contraction territory while the Services component barely stayed out of contraction (50.1).

In Europe, there’s another negative bias with the STOXX 600 down 0.4% as an index of inflation expectations showed a modest uptick from 2.0% to 2.1% for 2025. It wasn’t all bad news, though, as 2025 GDP growth forecasts also showed a modest uptick from 1.1% to a still anemic 1.2%. The higher inflation expectations were also accompanied by an uptick in headline CPI to 0.2% m/m from September’s rate of 0.1%.

Apple (AAPL) and Amazon.com (AMZN) rounded out the group of mega-caps reporting this week with earnings releases after the bell Thursday. Shares of Apple (AAPL) are poised to gap up over 2% at the open, but the real standout is Amazon.com (AMZN). While investors worried that the company’s layoff announcement earlier in the week was a precursor to a weak report, AMZN eased those fears with strong numbers across the board, and in response, shares spiked more than 10%.

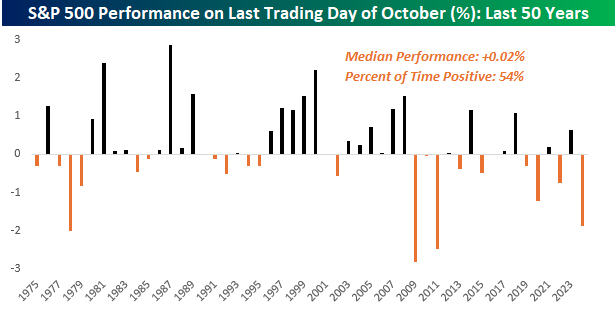

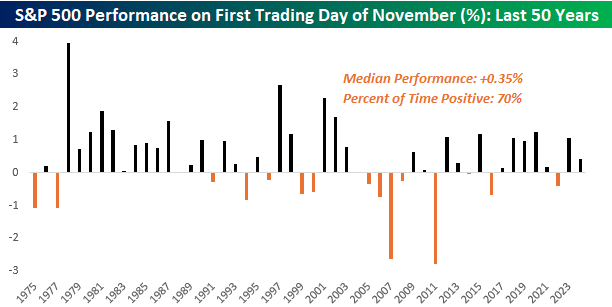

Today is Halloween and the last trading day of October, so can investors expect a trick or a treat? Over the last 50 years, it’s been a bit of a coin flip. As shown in the chart below, the S&P 500’s median performance on the last trading day of October has been a gain of 0.02% with positive returns 54% of the time. In terms of volatility, the median absolute daily change on these days has been 0.50%.

While the last day of October has been relatively uneventful in terms of returns, November typically starts on a more positive note. Over the last 50 years, the S&P 500’s median gain has been 0.35% with gains 70% of the time. And while October is a month known for its volatility, with a median absolute daily change of 0.77%, the first trading day of November has been more volatile than the last day of October.

Oct 30, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“And so we always say we’re not on a preset path, and we really mean that.” – Jerome Powell

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are lower this morning with the S&P 500 and Nasdaq both indicated to open moderately lower from yesterday’s close as investors continue to digest Powell’s hawkish comments from yesterday. The weakness also follows a slew of earnings reports, including the behemoths of Alphabet (GOOGL), Meta (META), and Microsoft (MSFT). The reaction from the market to those three has been somewhat of a draw, with GOOGL up sharply, META down sharply, and MSFT only modestly lower. The fun continues tonight with just as many reports, including Amazon.com (AMZN) and Apple (AAPL) after the bell. After that, we’ll be through the peak of earnings season, at least in terms of market cap, so Congress better get the government open again, so there can be some economic data to focus on!

In Asia, there was no shortage of headlines with Presidents Trump and Xi meeting in South Korea. While the two leaders reached a 1-year détente on trade with Trump reducing fentanyl tariffs to 10%, China agreed to keep the flow of rare earth materials going and announced plans to purchase soybeans, energy, and other farm products. President Trump also said he plans to visit China in April. Despite all the headlines, though, it was a quiet session as most indices in the region were modestly lower. Of course, South Korea bucked the trend, though, with a gain of 0.1% as the KOSPI remains seemingly unstoppable.

In European trading this morning, stocks are decidedly lower. The STOXX 600 is down 0.5% as Spain leads the way lower with a decline of just over 1%, while Germany outperforms, even as it faces a decline of 0.1%. GDP growth for the region was above expectations (0.2% vs 0.1%), as growth in France led the region. The underperformance from Spain, however, stems from a higher-than-expected inflation print as y/y CPI increased 3.1% versus expectations for an increase of 2.9%.

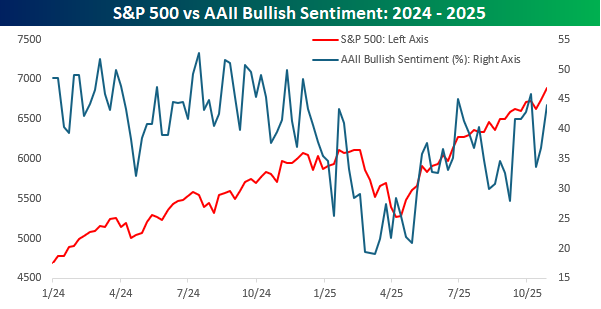

As US equities continue to march to new record highs, individual investor sentiment got a boost this week as the weekly survey from AAII showed that bullish sentiment increased from 36.9% to 44.0% for the highest reading in three weeks. While you would expect bullish sentiment to rise, current levels of optimism are nowhere near where they were at this point last year.

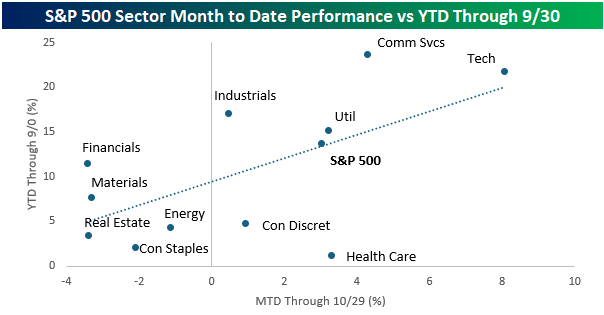

Perhaps one reason investors are less optimistic is due to the government shutdown, which has lasted nearly a month. With the S&P 500 up over 3% this month, it doesn’t appear as though the market is all that concerned, but looking at sector performance, there have been some shifts this month. The chart below compares sector performance so far in October (period covering the shutdown) on the x-axis to sector performance in the first nine months of the year (y-axis).

While sectors like Technology, Utilities, Energy, Real Estate, Materials, and Consumer Staples have stayed relatively close to the trendline, indicating that their YTD trend has remained largely intact this month, sectors like Communication Services, Health Care, Consumer Discretionary, Industrials, and Financials have seen their performance trend this month deviate significantly from their YTD trend in the first nine months of the year. That doesn’t necessarily mean that the shutdown has had a direct impact on these sectors’ performance, but their YTD trends have shifted.

Oct 29, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“People don’t care about what you say, they care about what you build.” – Mark Zuckerberg

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a day that doesn’t begin with “S” which these days means that stocks are poised to open higher with the S&P 500 indicated to open up 0.25% while the Nasdaq looks likely to gap up 0.43% at the open ahead of what will be a big day for earnings as three of the megacaps – Microsoft (MSFT), Alphabet (GOOGL), and Meta (META) – will report after the close. Also, don’t forget today’s Fed decision at 2 PM Eastern.

With equities indicated higher, treasury yields have also moved higher, but at 3.99%, the 10-year yield remains below 4%. Crude oil prices are slightly higher, while gold has rallied more than 1%, moving back above $4,000 per ounce.

In Asia, most indices were higher as positive headlines emerged from the President’s trip to the region. Consumer sentiment in Japan came in higher than expected, but inflation in Australia came in unexpectedly high. All eyes in the region will now shift to tomorrow’s meeting between President Trump and Chinese President Xi after headlines this morning suggest that China has already placed soybean orders with American farmers, while the US is likely to reduce fentanyl-related tariffs. The positive tone in Asia made its way over to Europe as the STOXX 600 rallies 0.3% with the UK and Spain up more than twice that.

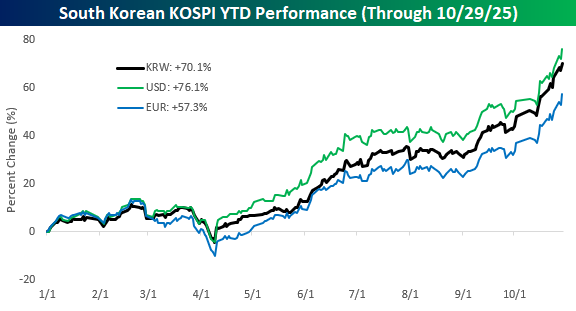

With Asian stocks mostly higher overnight, South Korea, after announcing a trade deal with the US, saw the KOSPI rally 1.8% to another in what has been a string of recent record highs. For the year, the KOSPI has now rallied more than 70%, which pretty much outdoes every other major stock market around the world on a YTD basis. Not only has the KOSPI rallied, but with its currency rallying against the dollar this year, from the perspective of a US investor, the gains are even greater at 76.1%. Even in euro terms, South Korean stocks are up over 57%!

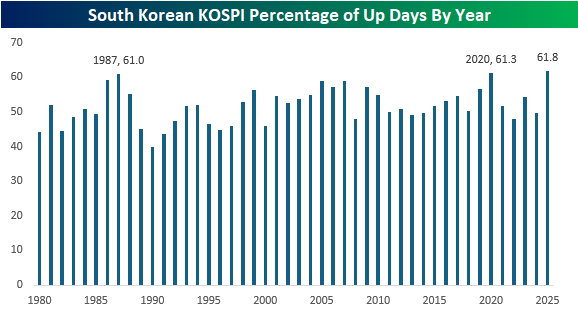

The gains in the KOSPI have also been consistent. Through last night’s close, the index traded higher on nearly 62% of all trading days, putting it on pace for the highest percentage of up days in a year on record. The only two other years when up days exceeded 60% were 1987 (61.0%) and 2020 (61.3%).

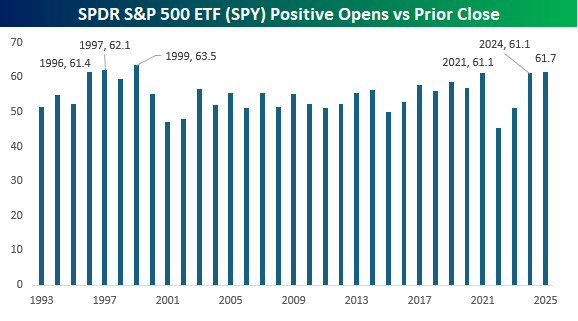

In the US, where we’ve seen strength this year has been at the opening bell. Just like today, the SPDR S&P 500 ETF (SPY) has gapped up at the open on 61.7% of all trading days. Since its inception, the only years with a higher percentage of positive gaps were 1999 (63.5%) and 1997 (62.1%), while 1996, 2021, and 2024 were the only three other years when SPY gapped up at the open more than 60% of the time.

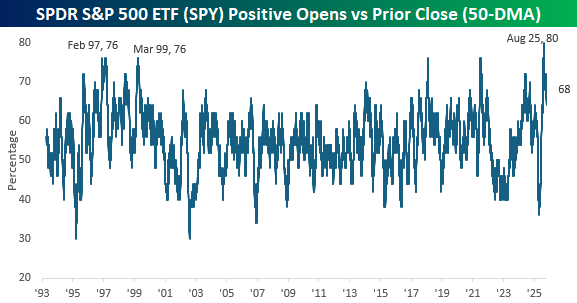

Much of the strength in SPY at the opening bell has come more recently since the tariff-tantrum. Over the last 50 trading days, SPY has gapped up at the open on more than two-thirds of trading days, and back in August, that percentage spiked up to a record high of 80%, exceeding the twin peaks of 76% from February 1997 and March 1999. What makes the current spike even more unique is the fact that it immediately followed a period of extreme selling at the open. Just as recently as this Spring, SPY gapped down on nearly two-thirds of all trading days, which was the lowest reading since December 2006.

Oct 28, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We are like chameleons, we take our hue and the color of our moral character, from those who are around us.” – John Locke

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a positive start to the week, stocks are taking a breather this morning as S&P 500 and Nasdaq futures are indicated just fractionally higher, while a 5%+ rally in UnitedHealth (UNH) in reaction to earnings has the Dow indicated to open up closer to 0.40%. The muted gains in the US follow what has mostly been a modestly negative session in Asia and Europe.

The pace of earnings has really picked up, and tomorrow will be the biggest day of earnings season in terms of market cap with Microsoft (MSFT), Alphabet (GOOGL), and Meta (META) all on deck to report. Besides earnings reports, this morning we’ll also get the October Richmond Fed report and Consumer Confidence at 10 AM Eastern.

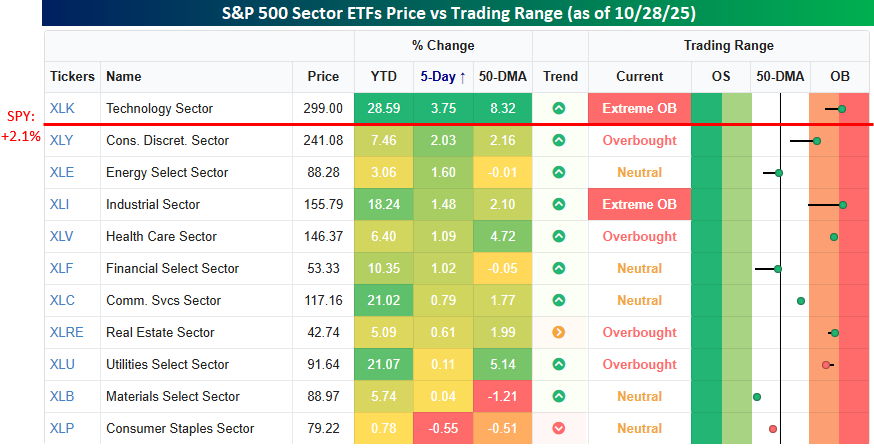

It’s been quite a week for stocks as the major US equity indices have broken out to new record highs, and S&P 500 7000 has entered the conversation. As noted in yesterday’s Chart of the Day, though, breadth has been somewhat weak. Another example of that weak breadth is in overall sector performance. As shown in the snapshot below showing sector ETF performance, over the five trading days ended yesterday, the only one outperforming SPY is Technology (XLK) with a gain of 3.75%. Consumer Discretionary (XLY) is close (2.03% vs 2.10%) but not good enough. Besides XLY, the only two other sector ETFs whose performance is within even one percentage point of the S&P 500 are Energy (XLE) and Industrials (XLI).

At the other end of the spectrum, the sectors underperforming are mostly what you would expect to see in an environment where the market rallies. Consumer Staples (XLP) is the lone decliner with a loss of 0.55% while Materials (XLB) and Utilities (XLU) have only seen modest gains of 0.10% or less. While XLU has underperformed over the last week, it remains one of just three sectors with a gain of more than 20% on the year.

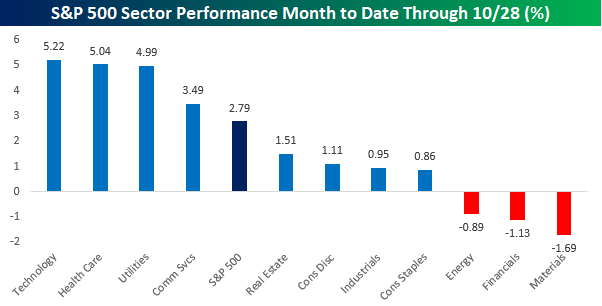

Shifting focus, with the government shutdown now set to enter its fifth week at midnight tonight, we wanted to look at how sectors have performed so far this month to see what, if any, impact it has had on performance. With a gain of 2.8% MTD through yesterday, it’s hard to say that the market has been impacted. Leading the way higher, Technology, Health Care, and Utilities have all seen gains of 5% or more, while Communication Services is the only other sector that has outperformed the S&P 500. To the downside, Materials (-1.69%), Financials (-1.13%), and Energy (-0.89%) are the only sectors to have experienced declines. It’s also worth noting that Consumer Discretionary has managed a gain of just over 1%, so even with so many Americans relying on the Federal government for either pay or benefits, and those paychecks and benefits poised to dry up, at least temporarily, it appears that the sector has held up.

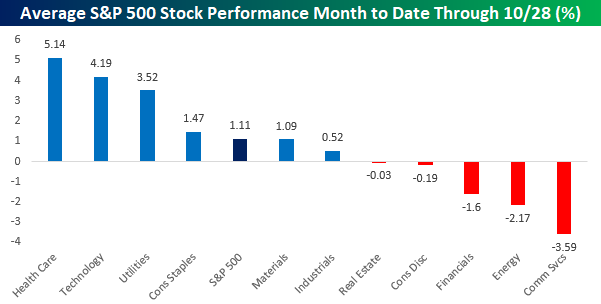

There’s always a but, though. If we look at sector performance on an unweighted basis, performance for the month looks much different. For the market as a whole, while the cap-weighted index is up 2.79%, on an unweighted basis, the gain is less than half that at 1.11%. One of the most notable shifts in performance, though, is in the Consumer Discretionary sector where the 1.11% gain on a market cap weighted basis shifts to a decline of 0.19% on an unweighted basis as MTD gains in the sector’s trillion dollar stocks (Amazon.com and Tesla) don’t carry nearly the weight on an equal-weighted as they do on a cap weighted basis.

Oct 27, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you could kick the person in the pants responsible for most of your trouble, you wouldn’t sit for a month.” – Theodore Roosevelt

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A flurry of trade deals announced over the weekend and this morning has futures surging, with the S&P 500 indicated to open up about 0.8% and the Nasdaq indicated to rally more than 1%. It should be noted, however, that current levels are off the overnight highs. With most of the announced deals being connected to Asia, that is where the biggest gains were seen overnight as the Nikkei rallied 2.5% while China gained more than 1%. European stocks have been much more subdued this morning as the STOXX 600 is just marginally higher and major benchmarks on the continent trade on either side of the unchanged line.

With investors taking more of a risk on approach, treasury yields are higher, with the 10-year yield moving back above 4% to 4.03%. Crude oil is fractionally lower along with gold as it tries to recover after breaking a streak of nine weekly gains last week. Finally, after a rough go of it in recent weeks, Bitcoin is up again after a strong weekend, taking it back above $115K while Ethereum is up over $4,100.

As mentioned above, gold ended a streak of nine straight weekly gains last week during which it rallied more than 25%. Since 1975, it was just the fifth time that gold traded higher for at least nine weeks and the first such streak since August 2020. Of the four prior streaks, only one in 2007 lasted longer (12). Of the four prior streaks, after the first down week that ended the streak, gold continued lower over the following three months three times for a median decline of 4.6%, and a year later it was lower three out of four times as well for a median decline of 7%.

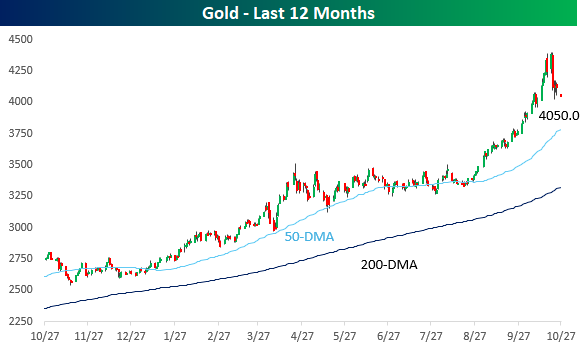

As shown in the chart below, gold’s decline last week was a sharp reversal from record highs hit just last week and was one of the larger drawdowns we have seen in the commodity over the last year. Despite the decline, though, gold remains well above its 50 and 200-DMAs.