Oct 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If everything you try works, you aren’t trying hard enough.” – Gordon Moore

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US stocks are on pace to end the week on a positive note as S&P 500 futures indicate a 0.33% gap higher at the open, while the Nasdaq is up 0.50%. Treasury yields are higher as the 10-year yield is back above 4%, and crude oil remains above $60 with WTI trading up 1%. Gold, on the other hand, is down 1.7% and on pace to end its nine-week streak of gains. Finally, crypto is higher with Bitcoin up 0.6% and back above $111K, while Ethereum gets back up near $4K with a gain of 2.3%.

Overnight, Asia was mostly higher with Japan up 1.35% after declining 1.35% Thursday. For the week, most major indices were up multiple percentage points, although India and Australia only managed modest gains. The tone is less positive in Europe this morning as most major indices experience modest declines, but for the week, they’re all comfortably higher.

We finally got a government-run economic indicator as the BLS summoned workers back into the office to tabulate the September CPI, which came in weaker than expected across the board. While still well above the Fed’s 2% target, it’s moving in the right direction.

It’s been a while now, but after nine trading days bouncing around within the intraday range from 10/10, the S&P 500 is poised to test the upper end of that range at the open today. If the streak ends, it will be tied for the longest run of days trading within a prior day’s intraday range in at least 40 years. In our Chart of the Day from Tuesday, we covered these prior streaks and how the S&P 500 performed going forward, so make sure to check that out.

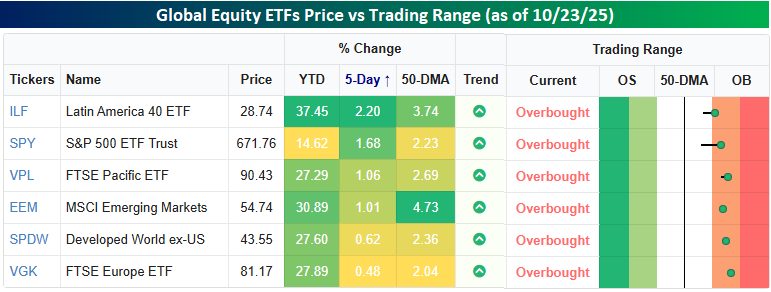

While the S&P 500 has been rangebound for two weeks now, like the rest of the world, it has been a positive week. The snapshot below from our Trend Analyzer shows the performance of various regional global ETFs. As shown, it’s been somewhat of a uniform move with every ETF trading higher to varying degrees over the last week, and all four moving into overbought territory. One of the biggest outliers, though, is in YTD performance. While every other regional equity ETF has rallied at least 27% YTD, the US is up barely more than half that, with a gain of ‘only’ 14.6%.

Oct 23, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want to increase your success rate, double your failure rate.” – Thomas J. Watson, Sr

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We may be starting to sound like a broken record, but once again this morning, futures are little changed with a downside bias, and the government is still closed. With the Fed in blackout ahead of next week’s rate decision, the only data the market has to focus on domestically is earnings. Overall, the pace of reports continues to come in positively with EPS and sales beat rates in excess of 70%. Also on the subject of broken records, it’s now been eight trading days where the S&P 500 has been stuck within the range it traded in on 10/10.

While the government may be closed, Washington is far from quiet, with the latest news being reports that the Trump Administration is in talks to acquire stakes of up to $10 million in various quantum computing stocks, including IonQ, Rigetti Computing, and D-Wave Quantum. Obviously, these stocks are surging in reaction to the news, and as a result have mostly erased yesterday’s declines. It’s worth pointing out, however, that after the gains these stocks have seen in the last couple of years, their market caps are all at or above $10 billion; a $10 million investment works out to less than 0.1%.

Outside of equities, crude oil is surging 5% and back above $60 per barrel after yesterday’s latest round of sanctions against Russian oil companies. Gold is also trying to regroup after the sell-off from the last couple of days, rallying 1.5% and back above $4,100 per ounce, while silver and platinum are both up at least 2.5%. Even Bitcoin and Ethereum have managed to rally more than 1%.

In international markets, Asian stocks were mixed overnight, with the Nikkei falling 1.4% and the Kospi dropping a percent. Hong Kong (0.7%), China (0.2%), India (0.2%), and Australia (0.1%) all managed to finish higher. The tone in Europe this morning is skewed more positive, with the STOXX 600 rallying 0.3% with little in the way of catalysts besides earnings driving the action.

The 10-year yield remains below 4% this morning after trading yesterday at its lowest level since the tariff-tantrum in April. While it wasn’t enough for a 52-week low on an intraday basis, on a closing basis, it was the lowest level since early October of last year. Since peaking at just under 4.6% in May, the 10-year yield has been stuck in a very consistent downtrend channel, and has been moving towards the lower end of that range all month.

Oct 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Women who seek to be equal with men lack ambition” – Timothy Leary

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The post 10/8 range-bound slog looks set to continue for the S&P 500 today as it enters its eighth day in a row of trading within its intraday range from 10/10. S&P 500 futures are essentially unchanged, while Nasdaq futures point to a modest decline. Yesterday’s weakness in gold and other precious metals has continued this morning, with gold down more than 1%, and while the crypto markets had a positive reversal yesterday, they’re giving it all back today as volatility in that space continues.

Overnight in Asia, most indices saw modest declines, although South Korea managed to buck the trend as it seems nothing can keep the Kospi down. European shares are mixed. The STOXX 600 is trading modestly higher on the session, led higher by the FTSE 100 and Spain’s Ibex 35, while Italy is down 0.5%. This morning’s strength in the UK was catalyzed by a much weaker than expected September CPI report, which showed no change in consumer prices relative to forecasts for an increase of 0.2%.

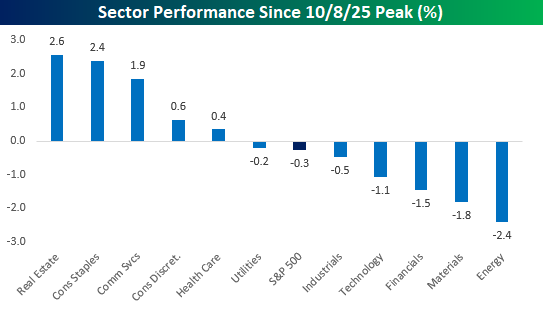

It’s now been two weeks since the S&P 500’s last record high, and while the S&P 500 has seen just marginal declines, some of the moves within sectors have been much larger. As shown in the chart below, Real Estate and Consumer Staples have both rallied over 2% and join Communication Services as the three sectors with gains of over 1%. To the downside, five sectors have declined since the 10/8 high, but four of them are down over 1%, including Energy (-2.4%) and Materials (-1.8%). Technology has also slumped 1.1%, which has acted as the main driver of the index’s decline.

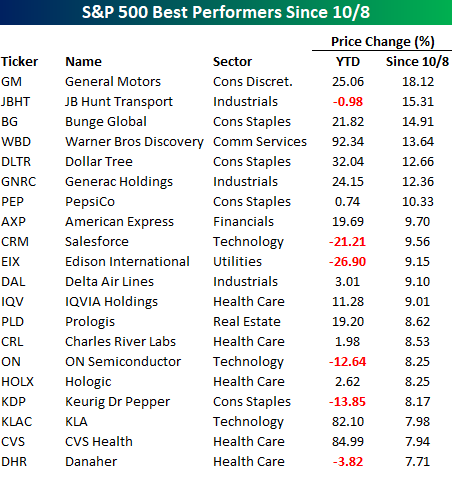

At the individual stock level, it’s been an eclectic mix of winners and losers. Starting with the winners, General Motors (GM) tops the list after yesterday’s post-earnings surge, and it’s one of seven stocks in the S&P 500 that have rallied over 10% since the 10/8 peak. While many of the 20 best-performing stocks in the S&P 500 are handily up YTD, they aren’t exactly the typical winners investors have been used to seeing throughout most of the year. The sector breakdown of these winners further illustrates that trend, as nearly half of the names listed are either from the Health Care (5) or Consumer Staples (4) sectors.

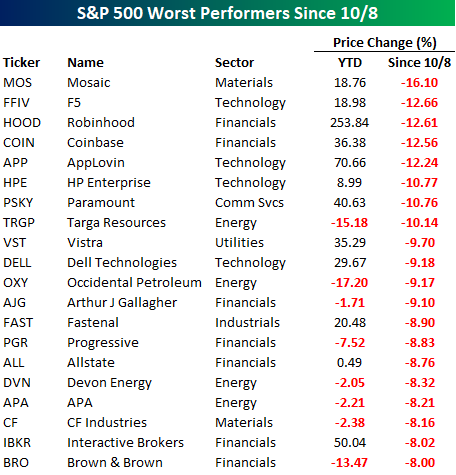

Shifting to the biggest losers, eight stocks in the S&P 500 have seen double-digit percentage declines since the 10/8 peak. Leading the way to the downside, Mosaic (MOS) has declined more than 16%. While many stocks listed have underperformed this year, for stocks like Robinhood (HOOD), Paramount (PSKY), Vistra (VST), Dell (DELL), and Interactive Brokers (IBKR), it has been a pause to potentially refresh.

At the sector level, Financials has been most heavily represented, with over a third of the names listed as concerns in the credit markets have hit some of the names in the sector hard. After Financials, the next most heavily represented sectors are Energy and Technology, with four each.

Oct 21, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In hindsight, I slid into arrogance based upon past success.” – Reed Hastings

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strong start to the week yesterday, US stocks are starting Tuesday on a modestly negative note with S&P 500 and Nasdaq futures both down less than 0.10%. The pace of earnings reports is finally starting to pick up, and what has been a strong reporting period so far in terms of results has remained that way this morning. As we type this, of the 14 companies reporting so far this morning, they have all exceeded EPS forecasts, and only one (NOC) missed top-line estimates. You can’t ask for much better than that!

With futures modestly lower, there’s still a lot of time left, but it’s pretty amazing to see that the S&P 500 still hasn’t traded outside of its intraday range from 10/10, which would make it seven straight days of trading inside a prior day’s range. Already, the current period ranks as just the 12th time in the last 40 years, and if the streak extends to seven, it would be just one of eight. For more on the topic, check out today’s Chart of the Day.

Outside of equities this morning, the 10-year yield is still below 4%, crude oil and natural gas are both up 1%, but precious metals are all uncharacteristically getting hit hard. Gold is down over 2%, while silver, platinum, and palladium are all down over 4%. Crypto prices also remain weak as Bitcoin trades back down below $110K and Ethereum is firmly below $4K with a decline of over 2.5%. Neither has been able to get back on track in the last couple of weeks.

Japanese stocks finished off their intraday highs overnight, but, along with other major indices in the region, finished higher on the session. Sanae Takaichi was officially elected PM, but there was a bit of sell-the-news reaction; Chinese stocks were the strongest in the region, finishing up more than 1% on optimism over US trade talks.

Europe is much like Asia this morning, with modest gains across the board. The STOXX 600 is up 0.1%, with Italy leading things higher, rallying by 1%.

Netflix (NFLX) will report earnings after the close today, which reminded us of an earnings report from the company in July 2011, when then CEO Reed Hastings announced that the company would be splitting off its DVD business from streaming, raising prices in the process. For consumers who wanted to continue with both services, the changes resulted in a 60% price hike from $10.00 to $15.98 per month. News of the price hikes and launch of the Qwikster DVD service were received poorly by the company’s customers and investors alike.

Right before the plan was announced, NFLX was trading at record highs, having just rallied 180% in the prior year. Within months, though, it gave up all of those gains, falling more than 70%. While there were other macro-related factors behind that drop, NFLX’s poorly communicated pricing plans and new strategy contributed to the weakness.

Following that decline in the wake of the Qwikster announcement, Hastings issued a public apology regarding how the changes were communicated, which included the quote above. Another month after his apology, Netflix reversed plans to separate the units (but kept the price hikes), relegating Qwikster to the waste bin of other disastrous product launches like New Coke, and more recently, the Cracker Barrel restaurant rebrand. Also, how can we ever forget the Apple Newton, rocking out with the Microsoft Zune, snacking on Olestra-infused WOW! Potato chips, and then the McDonald’s Arch Deluxe for dinner? The story of Qwikster and its demise before ever even launching serves as a reminder that the how of a message’s delivery can take on just as much importance as the message itself. It’s also a lesson that people and companies often become most vulnerable after a long string of successes, just as the feeling of invincibility starts to set in.

Hopefully, Netflix has no Qwiksters up its sleeve for today’s earnings report. Even after rallying 3% yesterday, the stock heads into the report short on momentum. While up over 60% in the last year and 25% in six months, the stock is down about 8% from its highs in the summer, forming a trend of lower highs. Looking on the bright side, the lack of a meaningful rally leading up to today’s report means that expectations likely aren’t too high.

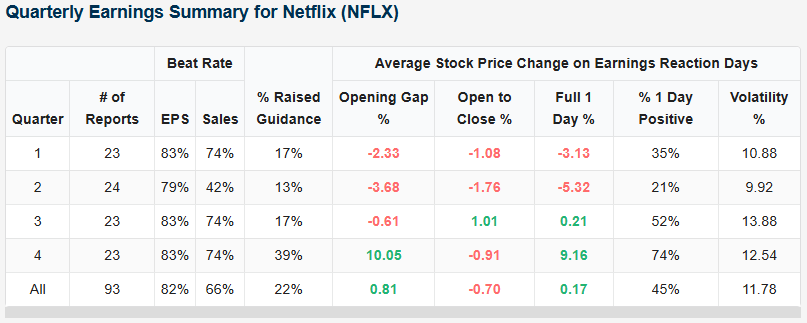

Looking at prior earnings reports from our Earnings Explorer, NFLX also has history slightly on its side. Over the last 23 years, its Q3 report has been the second-best of the four quarters in terms of stock price reaction. As shown in the table below, like Q4, NFLX has exceeded EPS forecasts 83% of the time in Q3 and topped sales forecasts 74% of the time. On its earnings reaction day, the stock averaged a gain of 0.21% with gains 52% of the time. That’s peanuts compared to the average gain of 9.2% following Q4 reports, but it beats the sharp declines that tend to follow Q1 and Q2 reports.

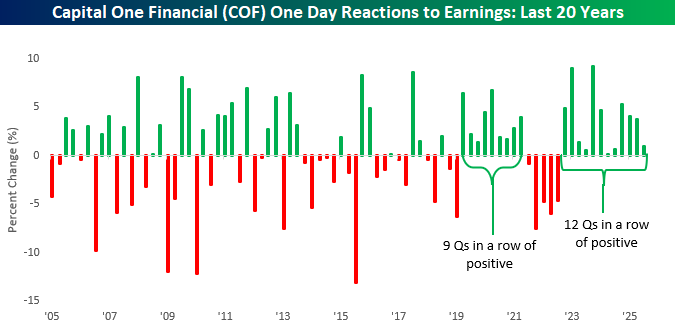

While NFLX will get most of the investor attention after the close today, another stock with a strong track record heading its report today is Capital One Financial (COF). Given its business, it will also give us a good read on the health of the consumer.

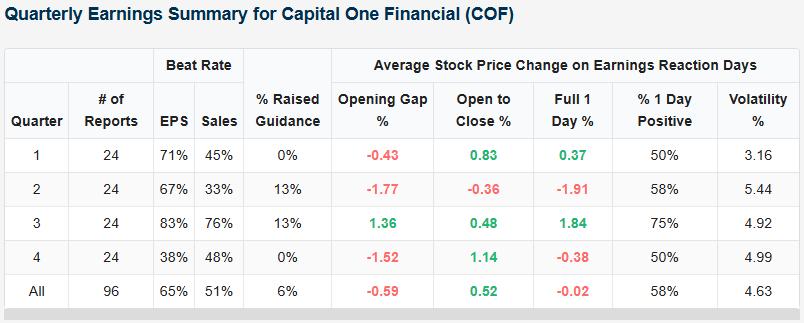

As shown in the snapshot below, COF has exceeded EPS and sales forecasts more in Q3 than in any other quarter. As a result, its average earnings reaction day performance has been a gain of 1.84% with positive returns 75% of the time. That’s also better than any other quarter.

Even more notable for COF is that the company has reacted positively to earnings for an incredible 12 straight quarters! Looking at COF’s one-day reactions to earnings over the last 20 years shows an interesting pattern. Whereas there was no streaky trend in terms of stock price reactions from 2005 through 2019, since then, it has been the opposite. COF has gone nine straight quarters with positive one-day reactions, then five straight quarters with negative reactions, followed by 12 quarters in a row of positive reactions. Talk about streaky!

Oct 20, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s unbelievable how much you don’t know about the game you’ve been playing all your life.” – Mickey Mantle

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The government remains shut down this morning as the stalemate between the two parties nears the start of its fourth week. As has been the case nearly the entire time, though, the markets seem indifferent as the S&P 500 will open today pretty much right where it was when the shutdown started. Interest rates are little changed this morning as the 10-year yield remains right at 4%. Crude oil is trading about 1% lower, right at $57 per barrel, and as has been the case for seemingly every day, gold prices are 1.5% higher, but still over 2% off record highs after Friday’s sharp reversal lower. Along with higher gold prices, crypto is also strong this morning with Bitcoin back above $110K and Ethereum back above $4,000. There’s not much economic data due to the shutdown, but the pace of earnings this week will really fill the void.

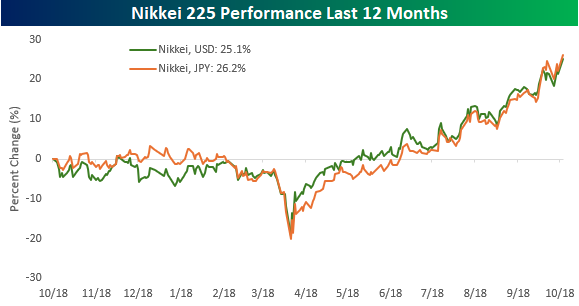

In Asia overnight, Japan surged more than 3% to new record highs after the LDP and Innovation Party agreed to form a coalition government, paving the way for Takaichi to become Prime Minister effective tomorrow. Elsewhere in the region, Chinese GDP rose more than expected, while Unemployment in Hong Kong rose more than expected.

Japan’s rally overnight pushed the index’s ‘marathon’ gain over the last 12 months to 26.2% in local currency terms, and interestingly enough, for all the fluctuations in global currencies this year, the dollar and yen haven’t moved much relative to each other, so on a dollar-adjusted basis, the Nikkei is up slightly less at 25.1%.

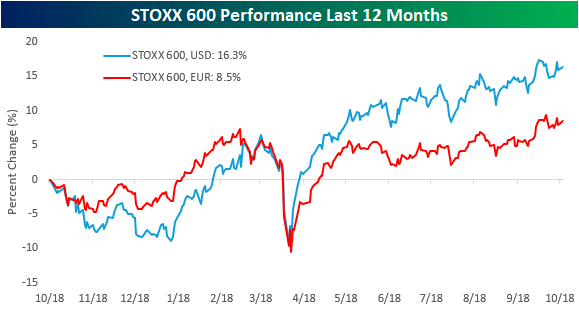

European markets aren’t as strong as Asia this morning, but they have a positive bias nonetheless. The STOXX 600 is up 0.6% to start the week. The CAC-40 is the only major benchmark not in the green as S&P lowered the country’s credit rating and an adverse legal ruling against BNP Paribas has that stock trading down over 5%.

Not only is Europe up less than Japan in early trading today, but the STOXX 600 is also lagging over the last year. As shown in the chart below, on a local-currency basis, Europe’s benchmark index is up a relatively modest 8.5% and trading just shy of new highs. After accounting for the weakness in the dollar this year relative to the dollar, though, it’s up nearly twice that at 16.3%. Depending on which side of the Atlantic you’re on, the performance of European stocks looks a lot different.

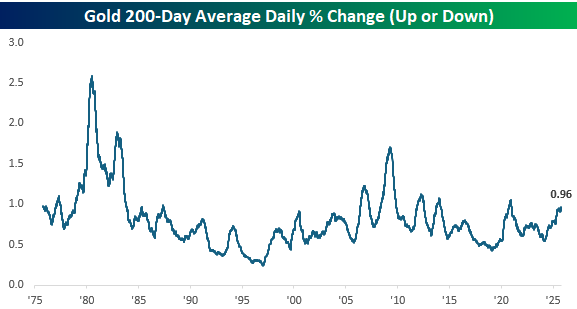

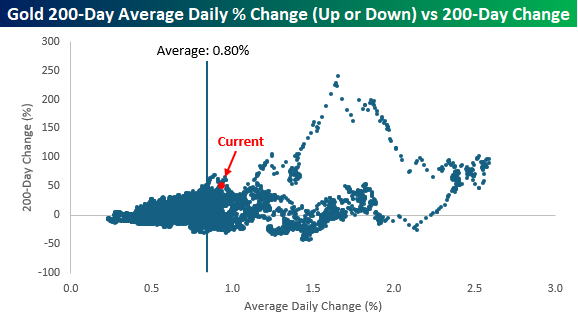

The weakness in the dollar against currencies like the euro has helped to drive the rally in gold, but in addition to being so strong lately, gold has also been volatile. Over the last 200 trading days, gold’s average daily move has been just under 1% which is the most volatility over a trailing 200-day period since Covid, but nowhere near historical extremes like we saw in the 1980s.

In the equity markets, volatility and large daily moves tend to occur during periods of market weakness, but for gold, that hasn’t necessarily been the case. In periods when gold has rallied 30%+ in 200 days, its average daily change was 1.27% whereas in all other periods, its average daily change was much less at just 0.76%.

Oct 17, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The main purpose of the stock market is to make fools of as many men as possible.” – Bernard Baruch

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity markets have seen volatility tick up as we enter the second half of October, which is very typical for this time of year. US index futures were down more than 1% a few hours ago, but they’ve rallied back to the flat-line after President Trump made comments diffusing trade drama with China.

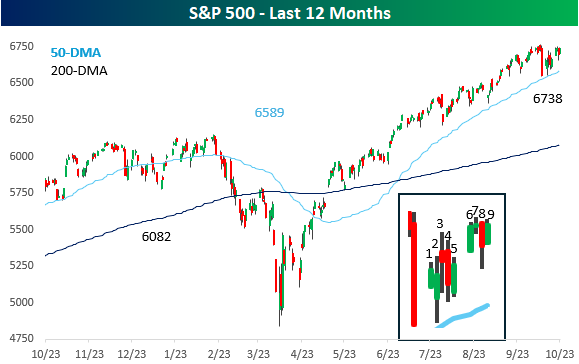

As shown below, key index ETFs remain within their long-term uptrends above their 50-day moving averages, with the exception of the S&P 500 Equal Weight.

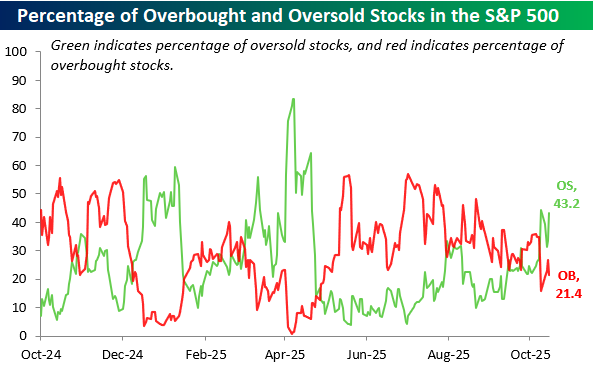

While cap-weighted large-cap indices remain strong on the surface, a much higher percentage of stocks in the S&P are now oversold (43.2%) than overbought (21.4%).