Aug 26, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you can go through life without experiencing pain you probably haven’t been born yet.” – Neil Simon

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If last week’s rally to close out the week felt like a Friday, this morning’s futures feel a bit like a Monday as futures are modestly lower in what feels like a sluggish market. The big headline this morning is probably a story from Friday where the President threatened tariffs on furniture makers who import goods from overseas. Stocks like Wayfair and RG are trading sharply lower in response,

The only economic reports on the calendar are New Home Sales at 10 AM and the Dallas Fed report at 10:30. Earnings season is mostly over, except for the elephant in the room – Nvidia (NVDA)- which reports Wednesday after the close.

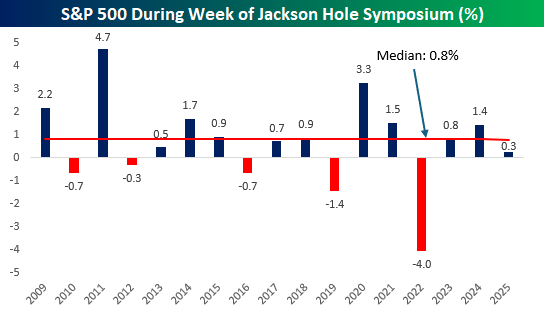

Friday’s gain wasn’t the first 1%+ rally this summer, but it was the largest gain for the S&P 500 since the day after Memorial Day. Even with that gain, the S&P 500 only managed to squeak out a gain of 0.3% for the week, owing to the five-day losing streak that the market was riding heading into Friday. Last week, we showed the chart of the S&P 500’s performance during the week of the Fed’s Jackson Hole symposium, and below we have updated it to include last week’s 0.3% gain. While it was a weaker-than-normal Jackson Hole week, last week was the third straight year of positive returns and the fifth in the last six.

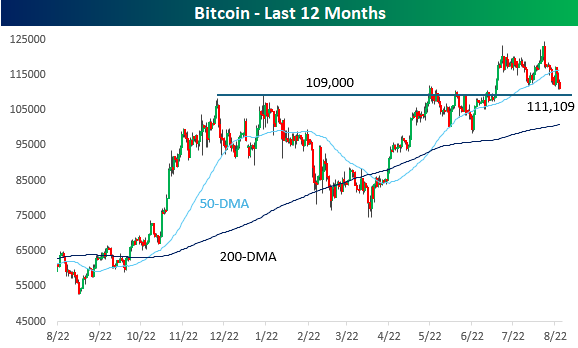

While most investors were checked out for the weekend, crypto markets had some major moves. Bitcoin, the world’s largest cryptocurrency, gave up all of Friday’s gains and fell to its lowest level since early July. The catalyst for the decline was a massive sale of 24,000 coins worth over $167 billion from a Bitcoin whale on Saturday. As shown in the chart below, for now, Bitcoin remains above support at the $109,000 level, but a break of that support within just two weeks of hitting a record high wouldn’t be a positive technical signal.

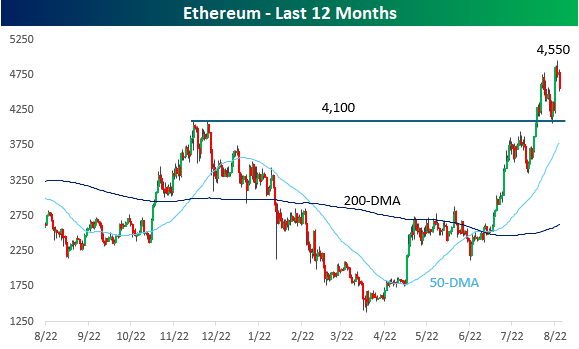

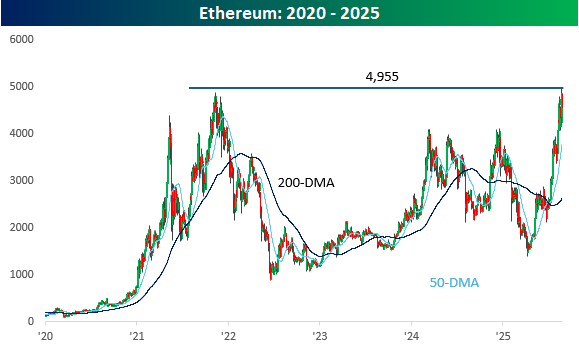

While Bitcoin investors may have been wishing that it didn’t trade on weekends after Saturday’s decline, Ethereum continues to gain attention and share in the crypto space. Around the time that Bitcoin was hitting record highs a couple of weeks ago, Ethereum was pulling back and testing support from its highs last fall. That support held, and over the weekend, Bitcoin broke out to new 52-week and record highs.

Looking at Ethereum from a 5-year time frame, its parabolic run over the last several weeks rocketed right through prior resistance in the low 4,000 range, right up to the highs from late 2021 and just under 5,000.

Aug 25, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Some people without brains do an awful lot of talking, don’t you think?” – The Wizard of Oz

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If last week’s rally to close out the week felt like a Friday, this morning’s futures feel a bit like a Monday as futures are modestly lower in what feels like a sluggish market. The big headline this morning is probably a story from Friday where the President threatened tariffs on furniture makers who import goods from overseas. Stocks like Wayfair and RG are trading sharply lower in response,

The only economic reports on the calendar are New Home Sales at 10 AM and the Dallas Fed report at 10:30. Earnings season is mostly over, except for the elephant in the room – Nvidia (NVDA)- which reports Wednesday after the close.

Friday’s gain wasn’t the first 1%+ rally this summer, but it was the largest gain for the S&P 500 since the day after Memorial Day. Even with that gain, the S&P 500 only managed to squeak out a gain of 0.3% for the week, owing to the five-day losing streak that the market was riding heading into Friday. Last week, we showed the chart of the S&P 500’s performance during the week of the Fed’s Jackson Hole symposium, and below we have updated it to include last week’s 0.3% gain. While it was a weaker-than-normal Jackson Hole week, last week was the third straight year of positive returns and the fifth in the last six.

While most investors were checked out for the weekend, crypto markets had some major moves. Bitcoin, the world’s largest cryptocurrency, gave up all of Friday’s gains and fell to its lowest level since early July. The catalyst for the decline was a massive sale of 24,000 coins worth over $167 billion from a Bitcoin whale on Saturday. As shown in the chart below, for now, Bitcoin remains above support at the $109,000 level, but a break of that support within just two weeks of hitting a record high wouldn’t be a positive technical signal.

While Bitcoin investors may have been wishing that it didn’t trade on weekends after Saturday’s decline, Ethereum continues to gain attention and share in the crypto space. Around the time that Bitcoin was hitting record highs a couple of weeks ago, Ethereum was pulling back and testing support from its highs last fall. That support held, and over the weekend, Bitcoin broke out to new 52-week and record highs.

Looking at Ethereum from a 5-year time frame, its parabolic run over the last several weeks rocketed right through prior resistance in the low 4,000 range, right up to the highs from late 2021 and just under 5,000.

Aug 22, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is winning and there is misery.” – Bill Parcells

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher heading into the last session of the week as the S&P 500 looks to end a five-day losing streak. There’s no economic data on the calendar, so whether we can end this streak will likely depend entirely on Powell’s 10 AM Jackson Hole speech.

In Europe, stocks are modestly higher on little in the way of news besides German GDP for Q2 being revised down more than expected to a decline of 0.3% versus forecasts for a decline of 0.1%.

In Asia, equities finished off a mixed week with a mixed session. Japan’s Nikkei finished slightly higher but down over 1% for the week. Chinese stocks were up over 1%, taking the weekly gain to more than 3%, while India traded down 0.9% on Friday but still managed to finish the week up nearly 1%. The main story out of the region was in China where Nvidia (NVDA) has reportedly stopped sales of its H20 chip to Chinese customers after that country’s government told local tech companies not to buy the chips citing security concerns. In response to the news, Chinese semiconductor names traded sharply higher.

It’s only been a week, but the general market tone heading into this Friday’s session is different than last Friday. For starters, we’re not sure where you are, but in the New York area, last Friday’s morning temperature was around 80 degrees, but this morning, we’re looking at a fall-like temperature of 58 degrees as we type this. In the equity market, last Friday, the S&P 500 was coming off its 3rd record closing high in a row and its 13th record high of the quarter. A rate cut at the next Fed meeting in September was pretty much a done deal.

Today, things look a lot less certain, the market is now pricing in just a 70% chance of a cut at the September meeting, and ahead of his Jackson Hole speech at 10 AM this morning, he probably won’t rule it out, but it doesn’t feel like Powell will make a forceful case to cut rates. With all the increased uncertainty, we’ve gone from a market closing at record highs to a 5-day losing streak that is tied for the longest since April 2024.

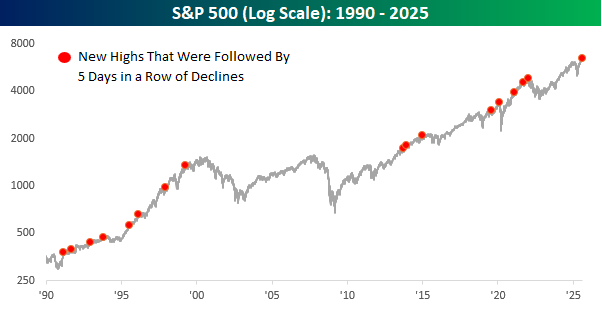

The last time the S&P 500 closed at a record high and then fell for five straight days was in January 2022 right at the start of the last bear market. There was also an occurrence right around the pre-Covid peak, and another near the dot-com peak in 2000. Any time you can make a connection between the current market and those three periods, it’s an ominous signal. Don’t they say that tops are a process? These all sound like pretty quick reversals!

Looking at ALL the occurrences where the S&P 500 hit a new high and then immediately went into a five-day losing streak, though, shows that there were plenty of occurrences within much longer-term bull markets.

Aug 21, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Solving big problems is easier than solving little problems.” – Sergey Brin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are set for another lower open this morning, just as the Fed kicks off its annual Jackson Hole symposium and tomorrow’s speech by Fed Chair Powell. Shares of Walmart (WMT) are down close to 4% after the company reported weaker-than-expected EPS. If the stock closes down today, it would mark the third consecutive negative reaction to earnings, the longest such streak since 2021. Outside of WMT, the earnings calendar is relatively quiet this morning, but it’s a busy day for economic data, with jobless claims (higher than expected) and the Philly Fed (weaker than expected) at 8:30, PMIs at 9:45, and then Leading Indicators and Existing Home Sales at 10:00 AM.

The weakness in US futures follows what has been a weak morning in Europe, where the STOXX 600 is down 0.3% while Asian stocks were mixed, with Japan falling 0.7% and China, India, and South Korea all finishing the session with modest gains.

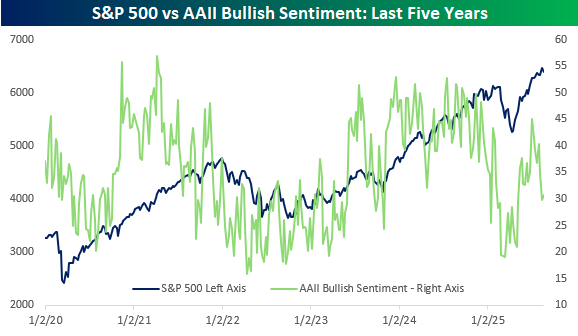

A four-day losing streak for the S&P 500 hasn’t done much to improve what has already been subdued sentiment on the part of individual investors. In this week’s survey from AAII, bullish sentiment rose slightly to 30.8% from 29.9% but with the S&P 500 within 2% of 52-week highs, investors aren’t happy. As shown in the chart below, a similar divergence emerged between equities and bullish sentiment earlier in the year, right before the market started to unravel. Then again, from early in 2021 and throughout the year, sentiment steadily deteriorated while the market just marched higher.

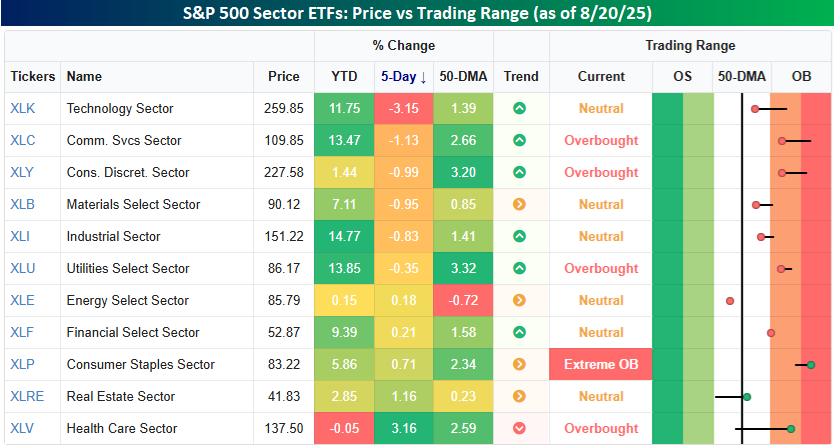

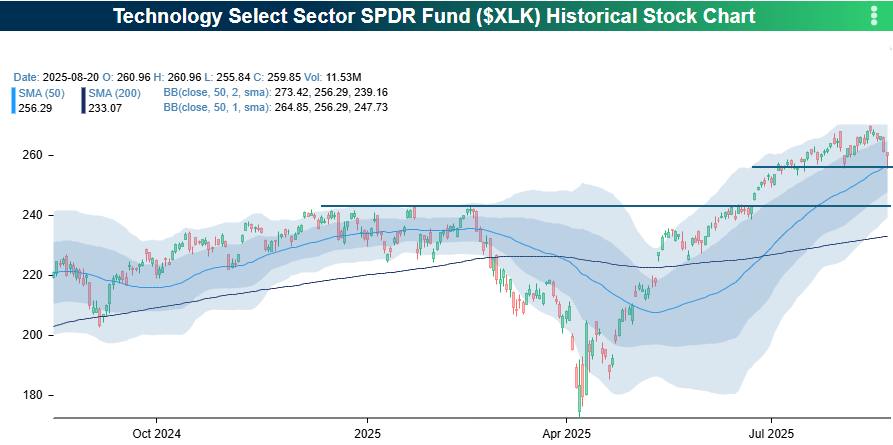

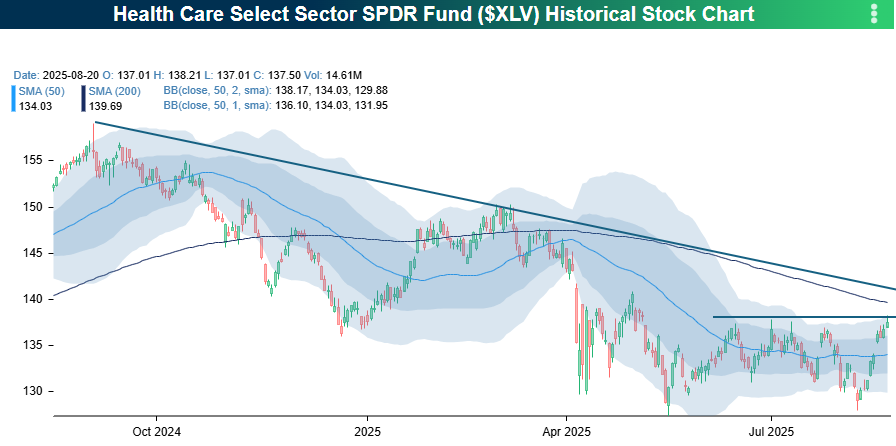

It’s been a mixed picture in terms of sector performance over the last week. Technology (XLK) has been the biggest loser, declining 3.2%, moving it out of overbought territory. Besides tech, the only other sector down more than 1% is Communication Services (XLC), while Consumer Discretionary (XLY) and Materials (XLB) are down just shy of a percent. At the other end of the spectrum, it has been defensive sectors holding up the best, just as you would expect during a market pullback. Health Care (XLV), the only sector down YTD, is up 3.2% while Real Estate (XLRE) and Consumer Staples (XLP) are the only two other sectors that have gained more than half a percent.

Looking at the Tech sector, at one point in yesterday’s sell-off, it tested its 50-day moving average and short-term support that coincides with other low points since the start of the second half. If these levels don’t hold, the next area to look at would be the high from earlier in the year, right before markets started to roll over. Those levels are about 7% below yesterday’s close.

Health Care has been a completely different animal. After testing support near 52-week lows last week, the sector has now rallied back to the high end of its post-Liberation Day range. If it can break through those short-term resistance levels, the next areas to watch will be the 200-DMA, which is about 1% above yesterday’s close. After that, the downtrend line in place for a year now would be the next area to watch. If the sector can break through all these levels, we may finally be able to say that the sector is on the mend!

Aug 20, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Only in America can you find so many angry people claiming to love their country, while hating almost anyone in it.” – Don King

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly lower this morning after a weak day for momentum and megacap stocks yesterday. There’s only been a handful of earnings reports this morning, and the market reaction to them has been mixed. On the positive side, shares of Analog Devices (ADI), TJX, and Lowe’s (LOW) are all higher, while Estee Lauder (EL) and Target (TGT) are both down sharply. For both of these stocks, the negative reactions aren’t exactly a surprise, as they have been weak for some time now. EL is on pace now for its sixth straight negative reaction to earnings and the 11th out of the last 12. TGT hasn’t been quite as much of a disaster, but today will be the fourth straight quarter that the stock has reacted negatively to earnings.

Besides these earnings reports, there’s not much else on the calendar for today. Weekly mortgage applications fell 1.4% after a 10%+ increase last week. We’ll also get the FOMC Meeting Minutes at 2 PM, along with speeches from Waller at 11 AM and Bostic at 3 PM.

In Asia overnight, the session was mixed, with China up 1% and Japan down 1.5%, as trade data was weaker than expected. In Europe, major averages are little changed as the STOXX 600 is up fractionally, as CPI was in line with expectations (0.0% m/m).

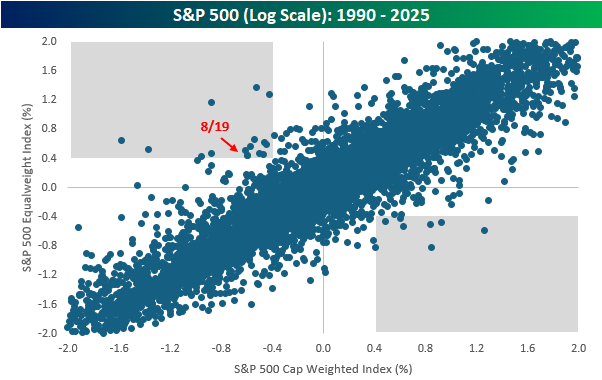

Depending on how you look at it, yesterday could have been a good or bad day. Based on the S&P 500’s 0.59% decline, it looked like a bad day, but underneath the surface, 354 stocks in the index finished the session higher, and the equally-weighted S&P 500 finished the day up 0.45%.

Divergent days like yesterday, where the cap-weighted index declines at least 0.4% while the equal-weighted index rises at least 0.4% have been very uncommon. Since 1990, yesterday was only the 16th occurrence, and there have only been eight days where the opposite occurred (cap-weighted index up 0.4%+ and equal-weight index down at least 0.4%).

The scatter chart below compares the daily performance of the S&P 500 cap-weighted and equal-weighted indices for every day since 1990, but we have truncated the axes at gains or losses of 2% so it’s easier to see the details. Dots that fall in the upper left gray box were like yesterday, where the cap-weighted index fell 0.4%+ and the equal-weight index rallied at least 0.4% while dots in the lower right box are the opposite scenario. Here again, this chart shows just how uncommon these types of daily divergences have been over time.

Aug 19, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A lot of people are scared to ask questions because they don’t want people to know how dumb they are. I’ve never had that problem.” – Ken Langone

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Home Depot (HD) kicked off retailer earnings week this morning and reported weaker-than-expected EPS on slightly weaker-than-expected revenues. That’s the bad news. On a positive note, the company reaffirmed its guidance for the full year, and while most companies missing results this earnings season have been pummeled on their earnings reaction days, shares of HD are trading more than 1% higher in the pre-market. HD earnings have had little impact on futures, which are mixed on either side of the flatline. That follows what was a fractionally negative overnight session in Asia, and a fractionally positive session so far in Europe.

Here in the US this morning, besides the HD earnings report, there hasn’t been much in the way of stock-specific news. On the economic calendar, July Building Permits and Housing Starts will hit the tape at 8:30. Heading into those reports, bonds are trading slightly higher, crude oil is down 1%, gold and other precious metals are modestly high, while Bitcoin and Ether continue their recent weakness with declines of roughly 1%.

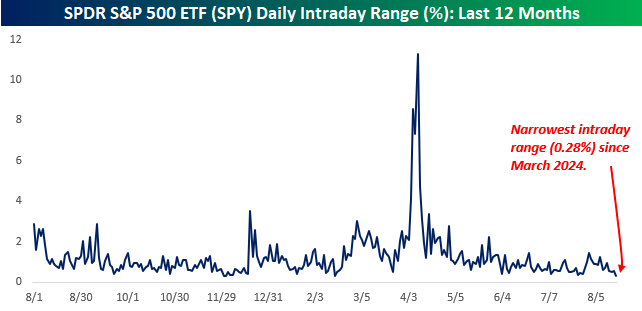

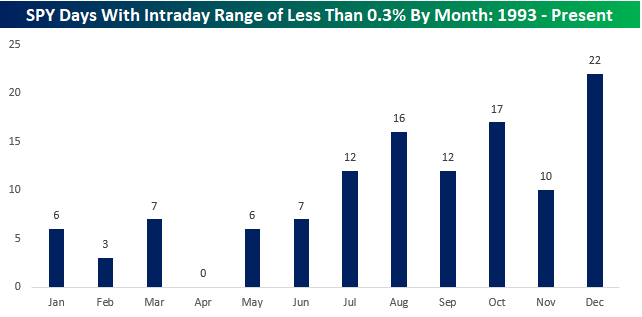

Yesterday was a tough day in the market – to stay awake. From the opening to closing bell, the SPDR S&P 500 ETF (SPY) traded in a range of 0.28% which was the narrowest intraday range since March 2024. To put yesterday’s range in perspective, the intraday range of the market on April 9th at the height of the tariff drama was more than 40 times larger.

Given that we’re in August, it shouldn’t come as too much of a surprise that the market has been quiet. Since the launch of SPY back in 1993, August has seen the third-highest frequency of days when the ETF’s intraday range was narrower than 0.3%. The only two months with a higher frequency were October (17) and December (22). December makes sense given the holidays, but the fact that October has had the second-highest frequency of days with an intraday range of less than 0.3% was surprising. Digging a little deeper, we found that more than half of them (9) occurred in October 2017. That could have been the most docile month of trading in SPY’s history!

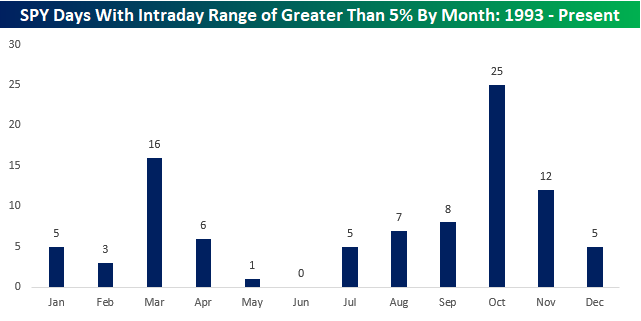

On the flip side, just for fun, we also looked at which months most frequently have seen 5% intraday ranges in SPY. Unsurprisingly, October has been the clear leader with 25, followed by March with 16. Here again, the high frequency of occurrences in March is primarily due to 2020, when there were 12, and the only four other occurrences were in 2009, around the lows of the Financial Crisis.