May 11, 2020

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

When futures opened last night, it was looking like there would be some positive follow-through from last week’s rally, but the gains evaporated overnight as weakness in Europe dampened sentiment on our side of the Atlantic. As things stand now, the S&P 500 is looking at a gap down of 0.80%. Crude oil was also weaker but has reversed into positive territory after Saudi Arabia announced a unilateral 1 million barrel per day production reduction. On the data front, it’s a quiet start to the week, but there’s still a number of earnings reports on the calendar

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, economic data out of Europe and China, and the latest stats and figures surrounding the COVID-19 outbreak.

From a seasonality perspective, this morning’s weakness doesn’t seem out of line. From our Seasonality Tool, the S&P 500 is currently entering what has historically been one of the weakest periods of the year. As shown below, the S&P 500’s median performance from the close on 5/11 through 5/18 has been a decline of 0.65% which ranks in just the 9th percentile for all one week periods of the year. The S&P 500’s median one-month return is positive at 0.37% but still ranks below the 30th percentile of all rolling one month periods. While one week and one month returns come in at the low end of the historical range, the S&P 500’s median three-month gain of 3.08% ranks considerably better in the 61st percentile of all rolling three-month periods.

May 8, 2020

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

We’ve just seen what is probably the worst jobs report in the life of anyone reading this. That’s the bad news. The good news? Hopefully, we’ll never see a report like this again! Today’s April Non-Farn Payrolls report is definitely great fodder for headlines heading into the weekend, but it is what it is. Everyone is expecting it, so it shouldn’t surprise anyone. Economists and market watchers will take great pains to dissect the numbers, but keep in mind that there are lots of distortions, and once all the revisions are made in the months ahead, the numbers will likely change a lot.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, a discussion of the move into negative territory for Fed Funds futures, and the latest stats and figures surrounding the COVID-19 outbreak.

It came right down to the wire yesterday, but the Philadelphia Semiconductor Index (SOX) finished up 1%+ for the fourth straight day. Sure, the gain was only 1.01%, but 1% is 1%. Thursday’s gain wasn’t the only ‘modest’ 1% gain of the current streak either. Starting with Monday, this week’s daily gains for the SOX were 1.03%, 1.68%, 1.08%, and 1.01%. That works out to a total four-day gain 4.9%, and while 4.9% is nothing to sneeze at, there has never been a four-day streak of 1% gains for the SOX that resulted in a smaller cumulative gain. Not only that, but the SOX is still below where it closed last Thursday (before Friday’s 5% decline). It’s not too often that a stock or index rallies over 1% for four straight days and still is in the red over the prior five days!

However weak the current streak of 1% gains is for the SOX, it still goes down as the longest such streak since December 2016. Also, if the SOX does manage to rise 1% again today (as it is currently trading in the pre-market, it would be the longest streak of 1% gains in over a decade!

We’ve covered breadth in these emails a lot this week, so we might as well check up on the SOX to see how breadth looks in the semis. Unlike the Nasdaq, which was showing a modest divergence with price since the end of April, breadth for the SOX has actually been slightly stronger than price, and that’s a good thing.

May 7, 2020

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Yesterday was a positive open for the US equity market, but all of those gains melted throughout the trading day and the day was capped with a sharp drop into the close. Today, futures are once again indicating a higher open. In fact, just before the release of weekly claims, futures were right at their highs of the session. After a higher than expected print of 3.169 million relative to expectations of 3.0 million, though, we’ve given up some of those gains, but we’re still firmly in positive territory. Looking on the bright side, at least claims have dropped for five straight weeks now. We’ll see what happens at 4 PM.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, Chinese export data, and the latest stats and trends on the COVID outbreak.

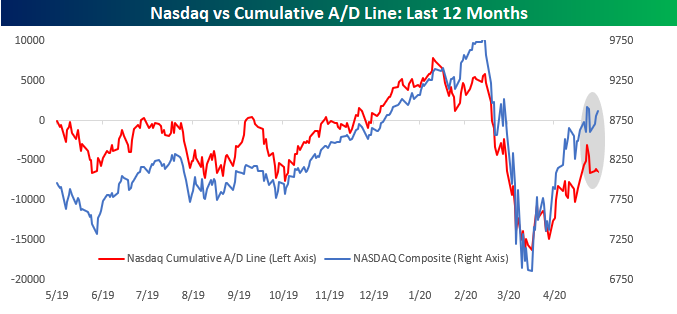

In yesterday’s email, we took a look at breadth in the S&P 500, but we all know that the Nasdaq has been the real star of the show. This morning, we wanted to provide a quick look at breadth in the Nasdaq. All we’ve heard recently is that the ‘big five’ of Microsoft, Apple, Amazon, Alphabet, and Facebook have been driving the market, especially the Nasdaq. The reality isn’t quite the case. While it’s true that back in February, the Nasdaq’s cumulative A/D line made a lower high just as the Nasdaq peaked, ever since then, breadth has been tracking price pretty closely. Through the end of April, for example, both price and breadth were at post 3/23 highs.

While breadth has tracked price pretty closely since the March lows, in recent days there has been a modest divergence between the two. As shown in the shaded region, while the Nasdaq’s price level remains right near its recent highs, the cumulative A/D line has been weaker. At this point, the divergence is small enough that it could be erased in a matter of days, but if this May pattern persists, then it will be a more definite sign of waning participation in the bounce. Today should be a good test for the Nasdaq as we’ve seen a number of smaller stocks in the index trading higher in reaction to earnings.

May 6, 2020

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Futures are off their earlier highs but still indicating a higher open. The big datapoint of the morning was the April ADP Private Payrolls report which came in at 20.236 million- by far the highest ever reading (by a factor of more than 20). While it’s little to no consolation, the print was actually slightly better than expected. Maybe the most impressive aspect of the release was that consensus estimates (20.550 million) were so close to the actual print.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, April PMI data, German Factory Orders, and the latest stats and trends on the COVID outbreak

We’re always paying close attention to market breadth for any signs of potential strength or weakness in the underlying market. The chart below shows the S&P 500’s cumulative A/D line and price over the last year. Comparing the two shows that breadth coming off the March lows has tracked price pretty closely. Just about every higher high and higher low in the market has been confirmed by the S&P 500’s cumulative A/D line, so that doesn’t suggest anything untoward occurring underneath the surface.

While overall breadth is positive, there has been an interesting and modestly negative divergence in breadth on big market days versus big down days. Since the 2/19 high for the S&P 500, there have been a total of 42 trading days where the S&P 500 was up or down 1% or more. On the 20 days where the S&P 500 was up over 1%, the median breadth reading was +370. On the 22 days where the S&P 500 was down over 1%, though, the median breadth reading was considerably more one-sided at negative 439. In other words, on days where the market is down big, investors are taking more of a sell everything approach, whereas on days when the market is up big, they are being more discriminating in their buys.

May 5, 2020

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Just about a month after Major League Baseball would have had its opening day, US markets are poised to open higher today on optimism that the opening day for the economy will be coming a bit sooner than previously thought. California is starting to make plans to open its economy in a limited fashion, and New York has also released its plans for how to reopen as well. We’re not out of the woods yet, but any move in the direction of opening is a good thing, and as long as these measures can be taken while keeping the outbreak in check, additional steps to reopen can continue.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, the German Constitutional Court’s decision ruling on QE, and the latest stats and trends on the COVID outbreak

While the S&P 500 is down modestly over the last five trading days, we’ve seen quite a bit of dispersion in sector performance. At one end of the spectrum, Energy stocks have been on fire rallying nearly 5%. Behind Energy, the only two other sectors that are positive over the last week are Communication Services (XLC) and Technology (XLK). On the downside, Utilities (XLU) are down by nearly as much as Energy stocks are up (-4.46%). Not far behind XLU, Health Care (XLV) and Real Estate (XLRE) are also down over 3%.

Relative to each sector’s 50-day moving average, we’re also seeing a wide range of levels. Of the 11 sectors, six are currently more than 5% above their 50-day moving averages, but after that, the only other sector that is above its 50-day moving average is Consumer Staples and just barely above its 50-DMA at that. While no sectors are currently oversold (more than one standard deviation below its 50-day moving average), Utilities, Financials, and Industrials are all more than 2% below their 50-DMAs.

May 4, 2020

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

After a strong rally in April, US equities have started a bit of a losing streak in the last three days. If this morning’s weakness in futures persists, it would be the longest losing streak in about two months. The negative tone this morning can be blamed on Warren Buffett whose tone at this weekend’s annual meeting wasn’t particularly positive as he disclosed that he has sold his entire stake in the major four airlines making Berkshire a net seller of equities. That didn’t set a particularly positive tone for the opening of futures Sunday night, but we’re currently off the lows, and as we have reminded a number of times over the last few weeks, though, there’s still a lot of time between now and the closing bell at 4PM.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, Markit PMI data, and the latest stats and trends on the COVID outbreak.

A lot of people may have missed it Friday afternoon, but Auto Sales data for the month of April was the worst on record. According to WARD’s data, total sales for the month were just 8.58 million on a seasonally adjusted annualized rate. Going all the way back to 1976, there has never been a weaker month. While the print was weak, it was actually considerably better than consensus expectations of just 7.0 million. So it was an absolutely awful print, but not quite as awful as expected.