Jan 30, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Hi-yo, Silver! – The Lone Ranger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Warsh it is. After months of speculation in the horse race among potential candidates, President Trump announced his boardroom decision, and the winner of “The Apprentice: Federal Reserve” is Kevin Warsh. Futures initially sold off sharply when news of the nomination first hit the tape last night; they have since recovered much of those losses. The major averages are now looking at more modest declines of 0.50% or less. It remains to be seen how Kevin Warsh will act when he’s in the Chairman’s seat, and while he may be considered as more hawkish than some of the other nominees, he’s well respected by the street. Furthermore, all worries over Fed independence over the last six months can probably be put to rest.

It was a lower session to close the week in Asia, as major country benchmarks ended the week with mixed returns. Japan finished the week down 1% while China was down less than half that. On the upside, the Hang Seng had a much better week, rallying 2.4%, but couldn’t hold a candle to South Korea, which rallied 4.7%. Japanese yields pulled in a bit after Tokyo CPI decelerated from 2.0% to 1.5% y/y.

In Europe, it’s a much more positive tone this morning as the STOXX 600 is up nearly 1% with Spain’s 1.8% rally leading the way, although no major benchmark is up less than 0.5%. Banks are seeing some of the largest gains, but the rally has been broad-based with Energy and Materials being the only sectors in the red, while advancers outpace decliners at a 5-2 rate. In economic data, Eurozone GDP rose more than expected 0.3% while CPI in Spain declined more than expected (-0.4% m/m).

The only economic data on the calendar today in the US is PPI at 8:30 and Chicago PMI at 9:45, but the main area of focus will be the President’s nomination of Kevin Warsh to replace Powell. PPI came in much higher than expected on both a headline (0.7% vs 0.3%) and core level (0.5% vs 0.2%), so that has pushed futures down a bit again.

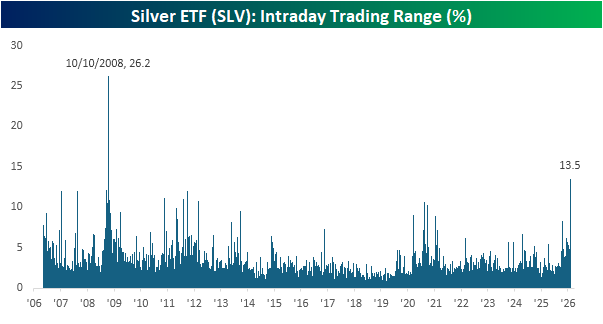

It seems fitting that on the anniversary of the Lone Ranger radio debut in 1933, we’re getting some historic moves in silver over the last 24 hours. Let’s start with the Silver ETF (SLV). In yesterday’s session, the ETF traded as high as $109.83 before cratering to $96.74 and then settling at $105.57. From its intraday high to its intraday low, though, SLV traded in a 13.5% range which was the second largest intraday range in the ETF’s history, trailing only the “marathon” 26.2% intraday range on 10/10/08 during the thick of the financial crisis.

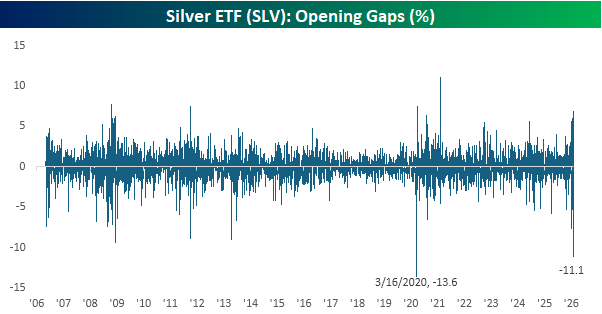

As if yesterday’s session wasn’t enough volatility for you, this morning, the SLV ETF is on pace to gap down 11.1%, which would be just the second time in its history that it opened down more than 10%. The only larger downside gap was a 13.6% decline on 3/16/20 during the heart of the Covid crash. In terms of yesterday’s range and today’s downside gap, recent activity in SLV is right up there with levels of volatility we saw during major market crises. What’s the issue this time around? The really amazing part about today’s downside gap in SLV, though, is that if current levels hold through the end of the day, it will still be up on the week!

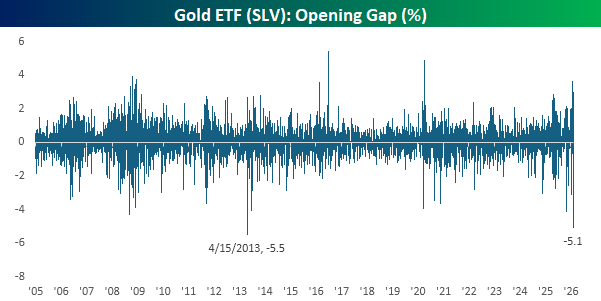

Not to be left out of the volatility party, gold is also poised for a rough start today. The Gold ETF (GLD) is on pace to gap down 5.1%, which would also be the second-largest downside gap in its 20+ year trading history. The only larger downside gap was on Tax Day in 2013, when GLD gapped down 5.5%. Like SLV, though, if current levels hold through the end of the trading day, GLD would also finish the week with a gain!

Jan 29, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You can fool some of the people some of the time — and that’s enough to make a decent living.” – W.C. Fields

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It was only a 0.01% decline, but the S&P 500’s drop yesterday ended a streak of five straight gains. The Nasdaq managed to finish up 0.17%, extending its winning streak to six. This morning, both indices are trading higher, so for the Nasdaq will today be lucky number seven? While Meta (META) and Tesla (TSLA) are doing their part to extend the Nasdaq’s streak, Microsoft (MSFT) is trading the other way after weak margin guidance has that hyperscaler trading down a not so lucky 7% this morning.

Outside of treasuries, the 10-year US Treasury yield is basically unchanged at 4.25%, while the dollar is little changed after a volatile few days to start the week. Precious metals continue to get more precious this morning, with gold up over 4% and breaking through $5,500 per ounce. Silver is up over 5%, platinum is up nearly 5%, and copper is also at a record, trading up close to 7%. For all three metals, their year-to-date gains are leaving equities in the dust.

In Asia overnight, the Nikkei was basically unchanged, but South Korea rallied another 1% as SK Hynix reported strong Q4 results. Hong Kong, China, and India were also higher on the session, while Australia had a marginal decline.

European stocks are mostly higher this morning as the STOXX 600 gains 0.5%, but Germany has been a major outlier with a decline of nearly 1% as earnings results from SAP weigh on the DAX. A January survey of Business and Consumer sentiment came in stronger than expected, showing an unexpected increase relative to December.

With the Federal Reserve behind us, investors will now turn back to earnings and economic data. Earnings this morning have been OK, with EPS and revenue beat rates for the morning coming in at about 67%. The economic calendar is also busy with Non-Farm Productivity, Unit Labor Costs, and jobless claims at 8:30, followed by Factor Orders and Wholesale Inventories at 10 AM.

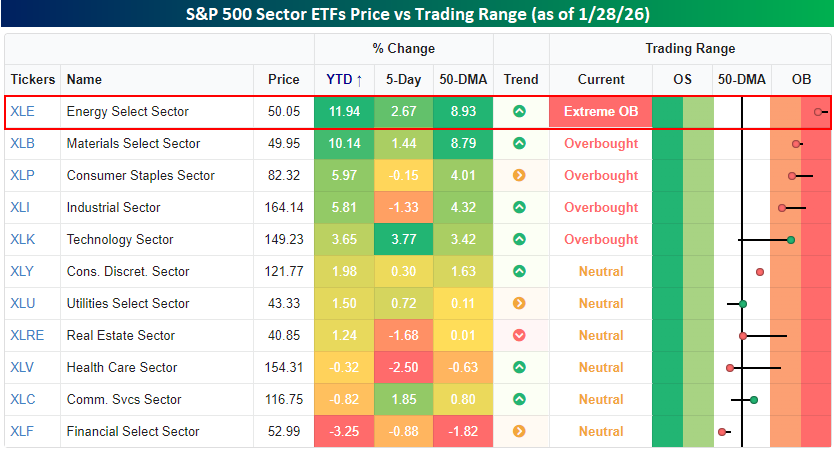

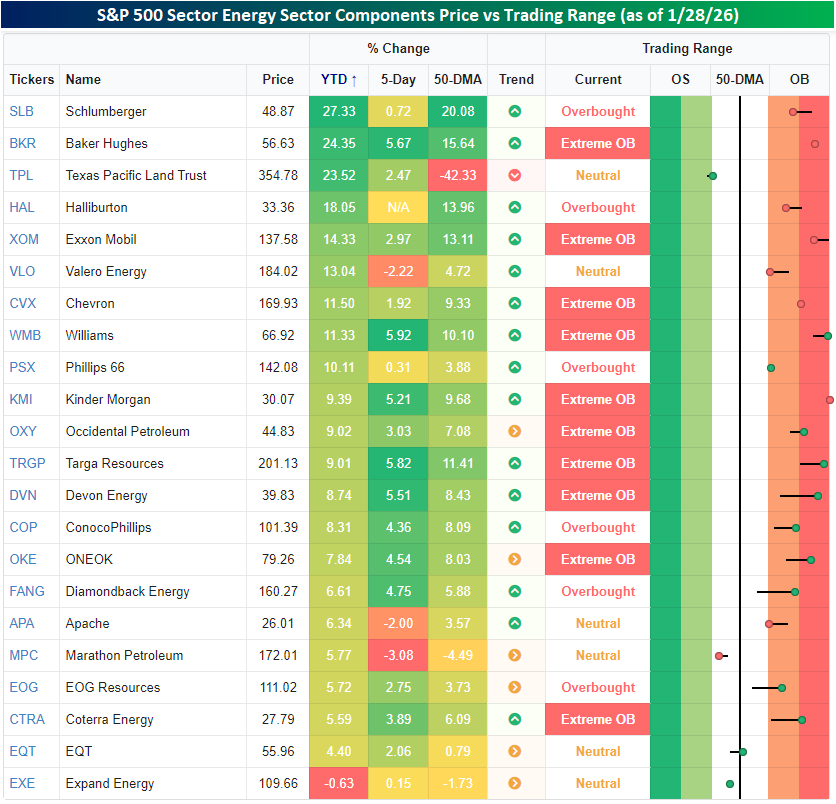

In yesterday’s note, we highlighted the strength in the Energy and Materials sectors and how they were leading all other sectors in terms of year-to-date returns. Through yesterday’s close, Energy and Materials were still leading the performance derby, but Energy is the only sector that remains in ‘extreme’ overbought territory (more than two standard deviations above its 50-DMA). Behind Technology, which has had a run this week, Energy is also the best-performing sector over the last five trading days.

Crude oil prices are up over 12% this year, and natural gas enjoyed a surge during the cold snap, although the contract roll has brought front-month futures prices back down to a three-handle this morning. You don’t have to look any further than these moves in the underlying commodities to understand why energy stocks are doing so well, but strength within the sector, while broad-based, hasn’t been uniform.

As shown in the snapshot below, all but one of the sector’s 20+ components are up YTD. The only outlier is Expand Energy (EXE), which is fractionally lower for the year. On the upside, the two leading stocks in the sector this year have been Schlumberger (SLB) and Baker Hughes (BKR), with gains of more than 20%. Both stocks gapped sharply higher following the early January arrest of Maduro in Venezuela and basically haven’t looked back since. Of the nine stocks in the sector up at least 10%, though, there’s been a smorgasbord of exploration companies, integrated oil companies, and even refiners.

Jan 28, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future doesn’t belong to the fainthearted; it belongs to the brave.” – Ronald Reagan, 1/28/1986

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are modestly higher again this morning, with the S&P 500 indicated to open up 0.25% while the Nasdaq is looking much stronger, gaining 0.85% as positive earnings reports in the Technology sector drive the sector’s gains. Investors are selling treasuries as the 10-year yield pushes 4.25%.

Gold is surging again today after yesterday’s comments by the President regarding the dollar, and the SPDR Gold ETF (GLD) has already rallied at least 1% for six straight days! Silver is also strong this morning, and the Silver ETF (SLV) has rallied at least 3% for four straight days! Investors are in such a ‘buy anything mode’ that even Bitcoin is rallying more than 1%, taking it back above $90K.

In Asia overnight, most major indices were higher. Hong Kong led the way with a gain of more than 2.5%, and South Korea’s Kospi tacked on 1.7%. A 40-year JGB auction in Japan was met with strong demand as the bid-to-cover ratio came in at 2.76, which was the strongest since last March. As we said, they’re buying everything this morning!

Well, maybe investors aren’t buying everything. In Europe, stocks are lower across the board. The STOXX 600 is down 0.5% with France, Italy, and Spain both down over 1%. Luxury stocks are weighing on stocks in the region following earnings from LVMH after the close yesterday, which we covered in last night’s Closer.

Today in the US, there’s no economic data on the calendar, but at 2 PM, the Fed will announce its latest rate decision, and the market is basically pricing in 100% odds of no change in rates. After the close, though, we’ll get earnings from Meta (META), Microsoft (MSFT), and Tesla (TSLA).

Merriam-Webster’s word of 2025 was slop which described the unending stream of low-quality, computer-generated content that has inundated the internet and social media feeds over the last three years. As much as AI promises to change life for the better, some of the more immediate impacts have been less than compelling. You can’t get away from it!

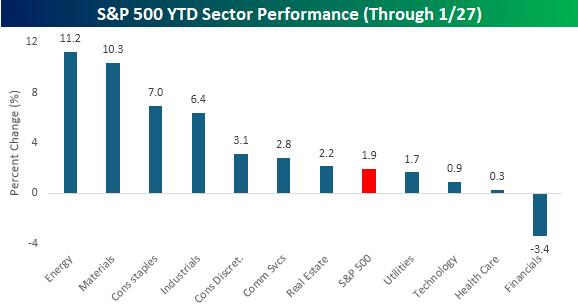

This is not even a month old, but if early indications are accurate, the term broadening could be a serious contender for the word of 2026. Looking at sector performance, the S&P 500 is up just under 2% YTD, but seven sectors have outperformed the index, including Energy and Materials, which are both up over 10%! Behind these two commodity-related sectors, Consumer Staples and Industrials are both up over 5%, while Consumer Discretionary, Communication Services, and Real Estate are all outperforming the index by a small degree.

On the right side of the S&P 500, Technology sticks out like a sore thumb with its gain of less than 1%. Along with Technology, Utilities, and Health Care are also up YTD but still underperforming, while Financials, which started the year off hitting all-time highs, is the only sector in the red for the year.

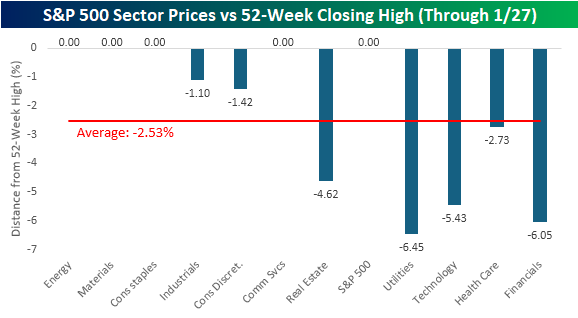

With the market broadening, we found it notable that, along with the S&P 500 yesterday, four sectors also closed at 52-week highs yesterday. Even many of the sectors that didn’t hit new highs yesterday aren’t far. Industrials and Consumer Discretionary are both within 2% of a 52-week high, while Utilities, Financials, and Technology are the only three sectors down more than 5%. The fact that the S&P 500 closed at a record high yesterday and its two largest sectors (Technology and Financials), which together account for nearly half of the entire index, are both down more than 5% from their highs is remarkable.

Regarding yesterday’s trivia, the five other schools to produce a Super Bowl winning QB and at least one US President are:

– Delaware: Biden/Flacco

– Miami (OH): Harrison/Big Ben

– Michigan: Ford/Brady

– Stanford: Hoover/Elway/Plunkett

– Navy: Carter/Staubach

Now to the bonus question. Of the 36 different head coaches to win a Super Bowl title, the school the college/university that has produced the most winning head coaches is Miami University of Ohio. The three Super Bowl-winning coaches who went there were Weeb Ewbank, John Harbaugh, and Sean McVay. Congratulations to everyone who got it right.

Jan 27, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We’re all mad here.” – Lewis Carroll, Alice in Wonderland

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Stocks are poised to build on yesterday’s rally with S&P 500 futures up 0.25% while the Nasdaq gains 0.60%. Treasury yields are slightly higher as the 10-year yield sits just under 4.23% while the dollar is weaker. Crude oil is little changed at $60 per barrel, while natural gas is giving back some of the massive gains of last week with a drop of over 6%. Precious metals are also lower after their surges to start the week, and Bitcoin is slightly higher.

On the data front, we’ll get Case Shiller numbers at 9 AM, and then the Richmond Fed and Consumer Confidence at 10 AM. After those reports, all eyes will shift to tomorrow’s FOMC announcement, although there’s already widespread agreement that rates will be left unchanged, and the upcoming mega cap earnings.

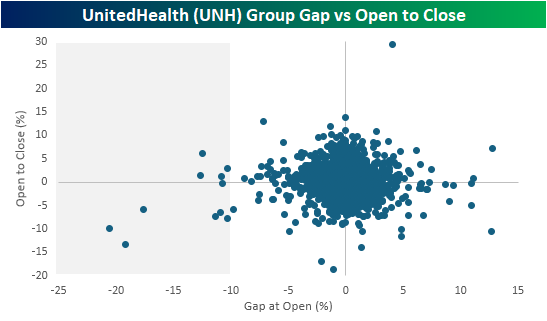

Following last night’s announcement that the U.S. government proposed a much lower-than-expected payment increase of just 0.09% for Medicare Advantage plans in 2027, coupled with a tepid revenue outlook for the year ahead, shares of UnitedHealth Group (UNH) and many of its peer stocks are down sharply in pre-market trading. For just UNH alone, its impact on the Dow Jones Industrials will be a decline of 350 points, so without that, the Dow would be higher.

Looking at a one-year chart of UNH shows that, based on where the stock is trading in the pre-market, it is on track to test support at the low end of its current six-month range, and a break of that level would put the lows from the summer back into play.

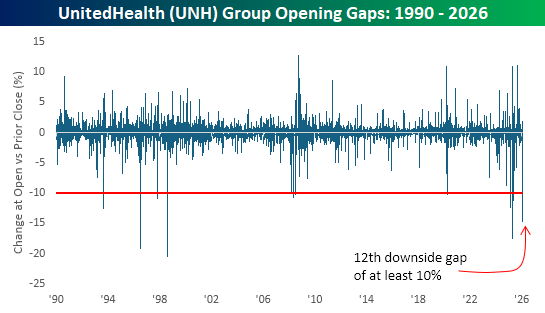

Going back to 1990, today’s downside gap will be the 12th time that UNH has gapped down more than 10%, and the frequency of those downside moves has really increased in pace over the last year. From late 2008 through the end of 2024, there was only one occurrence (during Covid on 3/16/20), but today’s decline will be the fifth in the last year alone!

The scatter chart below compares UNH’s daily opening gaps with its intraday performance from the open to close. The shaded area highlights each time the stock gapped down more than 10%, and following most of those opening declines, dip buyers weren’t quick to step in during the trading day, and in many cases, the stock added significantly to those opening declines.

Trivia Time. We wanted to close today with a little bit of trivia, and this one comes partially from Yahoo! Sports. If Drake Maye wins the Super Bowl this year, the University of North Carolina would be just the sixth school to produce a U.S. president and a Super Bowl-winning QB. What were the other five?

And as a bonus question, 36 different head coaches have won a Super Bowl title. What college/university has produced the most winning head coaches? Check back tomorrow for an answer, or feel free to respond with your guess. No cheating!

Jan 26, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I skate to where the puck is going to be, not where it has been.” – Wayne Gretzky

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As much of the country digs and/or scrapes out from the snow and ice over the weekend, it’s a very lackluster morning for US equity futures. The S&P 500 looks to open 6 bps lower, while the Nasdaq is down slightly more at 19 bps. It’s worth noting, though, that both indices are well off their overnight lows. Treasury yields have a downward bias, with the 10-year yield trading down to 4.22%. Crude oil is slightly lower at just under $61 per barrel, but natural gas is surging more than 10% as it has nearly doubled in price over the last ten days as the US continues to fall into the grip of a severe cold snap. Everything is hot in the metals space, though, as gold now trades above $5,000 per ounce, while silver rallies 8% and platinum gains another 4%. Crypto continues to sit this rally out, though. While it’s higher this morning, those gains follow weakness over the weekend.

Although the Hang Seng managed a slight gain, most other Asian benchmarks were lower to start the week, although Australia and India were closed for a holiday. The Nikkei declined 1.8%, and even South Korea declined 0.8%. The declines in Japanese stocks came as the Yen followed through from Friday’s rally and rallied another 1% on speculation of a possible intervention on the horizon to halt the long-term slide in the currency (more on that below). Chinese stocks were only down fractionally, but there were some reports of possible disagreements between President Xi and one of his top generals, resulting in the removal of the general and other military members.

There’s not a lot going on in European markets as the STOXX 600 is basically unchanged, but most major individual indices are slightly higher.

On the US calendar, it’s a light day with Durable Goods at 8:30, and there’s no Fedspeak as the Federal Reserve is in its blackout period ahead of Wednesday’s meeting.

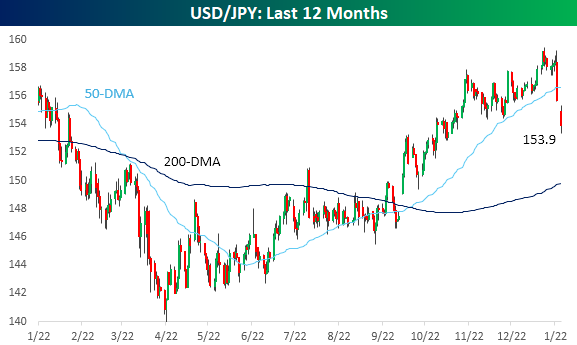

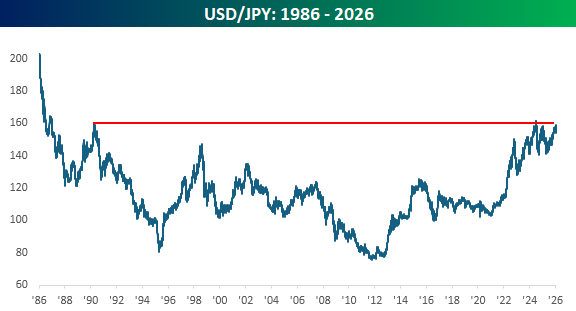

The rally in the yen on Friday took the dollar cross below its 50-day moving average for the first time since early October, and today’s rally has extended those gains to take the currency to its best levels versus the dollar since early November.

From a longer-term perspective, the rally in the yen has occurred at what is turning into a significant support/resistance level. In more recent history, levels around 160 have acted as support for the yen, and that level also coincides with a peak in the cross (low in the yen) from early 1990. And if you want to get creative, you could even make out what looks like an inverse head and shoulders.

We’ve seen a lot of huge moves in commodities over the last several months, and natural gas has started to get into the act over the last two weeks. Ten calendar days ago, on 1/16, natural gas closed at 3.10 MMBtu. This morning, prices are nearly twice as high, and earlier in the morning, they were double the level of the 1/16 close! Looking at the chart of natural gas and its history in terms of how the commodity has performed following prior short-term spikes, buying natural gas today feels a lot like skating to where the puck is rather than where it’s going. And happy 65th birthday to Wayne Gretzky!

Jan 23, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Our conviction in the essential role of CPUs in the AI era continues to grow” – Lip-Bu Tan, Intel (INTC)

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

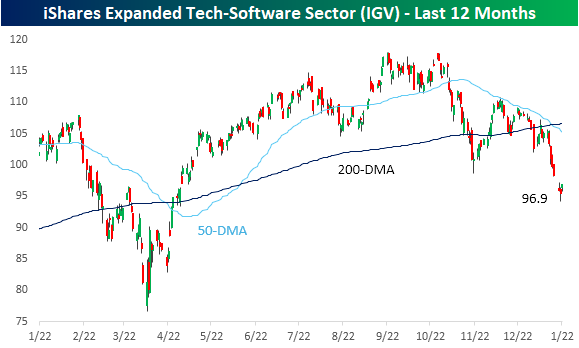

Wait. Isn’t the market up so far this year? For years, investors became conditioned to think that if the market rallies, software stocks will lead the gains. It was nearly 15 years ago, but Marc Andreeson’s famous article titled “Why Software Is Eating the World” reflected a theme that dominated the market for years – it was software’s market, and everyone else was just on the sidelines watching. Based on the last several months of trading, it appears as though the market is seriously questioning whether software has had its fill.

The iShares Expanded Tech-Software ETF (IGV) used to be a guaranteed way for traders and investors to generate alpha, but so far this year, the ETF is down over 5%, and it has pulled back about 20% from its record high in September to levels it hasn’t traded at since late April.

We covered software in yesterday’s Chart of the Day, and we’ll expand on that analysis below. Looking at the software ETF’s ten largest holdings and their performance through Thursday’s close, they’re all down YTD, all down over the last week, all below their 50-day moving averages, and all at oversold levels. Alpha? How about anti-alpha?