Oct 16, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“‘That didn’t work’ is cool, but ‘that won’t work’ is not a way to go through life.” – John Mayer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A triple play from Taiwan Semiconductor (TSM)—beating on earnings, revenue, and guidance—is lifting US equity futures, with technology stocks at the forefront. This rally is notably happening despite the President stating yesterday after the close that, “We are in one now,” in reference to a trade war with China. There are also signs that China’s aggressive stance on rare earth exports could be backfiring, as it has started to cause a more unified front between the US and other international partners.

Today was supposed to be a busy one for economic data, but the government shutdown put the kibosh on that, and the only report released was the Philly Fed Manufacturing report, which came in weaker than expected. The pace of earnings, however, remains active, and once again this morning, we’re seeing generally strong results.

Outside of equities, crude oil is fractionally higher but still well below $59 per barrel, the 10-year yield is trying to hang on to 4%, gold and other precious metals are rallying (what else is new), and crypto is also rallying after what has been a rough week for the sector.

It’s been a somewhat rocky week for US equities, although by the standards of October, it’s hard to get too worked up. After trading at an all-time high intraday last Thursday, the S&P 500 closed modestly lower on the day. That modest decline was followed on Friday by a sharp 2.7% decline in the S&P 500 as trade issues with China and concerns over corporate credit in the auto sector nudged investors to take some risk off the table. This week started on a positive note as the S&P 500 erased half of the losses from last Thursday and Friday, but intraday trading has been more volatile, and there’s been more of a tendency to sell rips than buy dips.

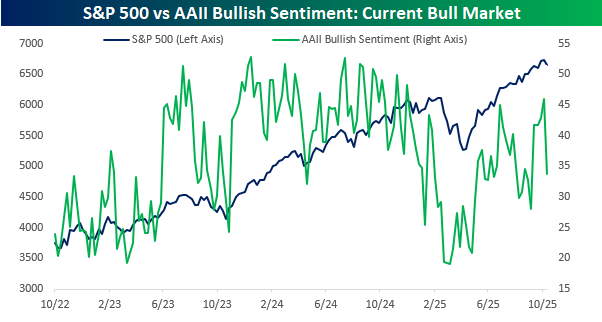

The skittishness showed up in investor sentiment this week as the weekly American Association of Individual Investors (AAII) survey showed that bullish sentiment dropped from 45.9% to 33.7% for the lowest reading in a month. The decline in bullish sentiment comes even as the S&P 500 closed within 2% of a record high yesterday. While bullish sentiment was routinely near 50% throughout 2024 as the market rallied, in the bounce off the April lows, investors have been much less willing to hop on the bandwagon.

Along with the modest weakness in US stocks over the past five trading sessions, global equities have also been under pressure. Of the US-traded ETFs tracking the stock markets of the seven G7 countries, all but France (EWQ) traded lower in the five trading days ended yesterday, and the US was stuck right in the middle with a decline of 1.2%. The biggest laggards have been Italy (EWI) and Germany (EWG) as their the only two below their 50-DMAs. Markets have certainly been on a tear this year as six of the seven ETFs listed have rallied at least 20% this year, but in the short run, they’ve mostly worked off their overbought conditions as France is the only country still in extended territory.

Oct 15, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stock prices have reached what looks like a permanently high plateau” – Irving Fisher, 10/15/29

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a sell-off into the close yesterday, equity futures are rallying this morning on the back of strong rallies in Asia and Europe. S&P 500 futures are up 75 bps while the Nasdaq is up 1%. In the commodities space, crude oil is little changed, while gold is up another 1% and now over $4,200 per ounce.

While there’s little economic data on the calendar again today, it’s been another strong showing for earnings this morning as eight of the ten companies reporting exceeded bottom-line results, while Progressive (PGR) was the only miss. Revenues have also been strong as the pace of beats has been nearly as strong.

We’ve all said things that we wish we could take back, and we can all come up with countless examples involving a boss, friend, family member, spouse, and/or our kids. You don’t need us to give you examples. In a less personal sense, it’s always funny to look back at past comments from public figures and, with the benefit of hindsight, see how foolish or wrong their comments turned out to be.

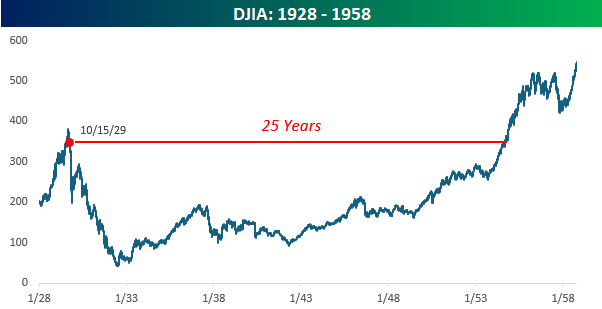

The stock market has seen a lot, but one of the most famously disastrous comments was made exactly 96 years ago today when an economist named Irving Fisher spoke at an industry trade dinner in New York. Fisher was one of the most well-known economists of his generation. Joseph Schumpeter called him the “greatest economist the United States has ever produced”. His theories on the velocity of money helped him forecast swings in inflation and the economy, and he wrote a weekly economic column that was read by millions of readers. He spoke to audiences all over the country, and they hung on every word.

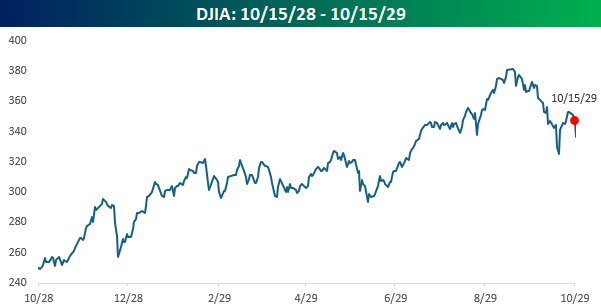

The most famous or infamous of those speeches came on 10/15/29 when he made the quote above, and then followed it up later on in an informal Q&A session, saying he expected “to see the stock market a good deal higher than it is today, within a few months.”

When Fisher made those comments, the equity market was coming off a solid year of gains. While the Dow was down about 8% from its September high, it was still up over 40% in the prior year. And that was coming off what had been one of the strongest four-year stretches in stock market history, where the index had tripled! Given the path equities had taken, Fisher’s comments were hardly out of consensus. At that point, gains were expected.

While investors were feeling entitled to gains, what the market giveth, it can quickly take away. The day after his comments, the Dow fell by over 3%. Then, after a one-day bounce of 1.7%, it had back-to-back declines of over 2.5%. Then, it kept falling from there. On 10/23, the DJIA fell 6.3%. On 10/24, it fell another 2%. Then, on 10/28, the crash came as the Dow fell 13% followed by another decline of 12% the day after that. Just after Labor Day of 1929, the Dow was at record highs, basking in the heat of the roaring 20s. Now, less than two months later, it was down 40%.

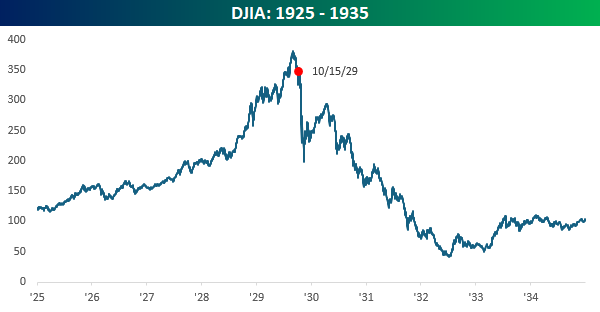

Looking at a ten-year window of the Dow from 1925 to 1935, from its peak in 1929 to the low three years later, it lost nearly 90% of its value. The economy sank into the Great Depression, erasing generations of wealth and causing permanent damage to the fabric of the US economy. Maybe not creative, but destruction nonetheless!

The S&P 500 closed at record highs just a week ago today, so no matter how steep the selloffs have been over time, the market has always come back. Sometimes, though, the comebacks take longer than others. After the peak this February, it only took a few months. After the 2022 peak, though, it took two years for the market to make new highs. Coming out of the Financial Crisis, it took close to five years. After the dotcom bust, it took seven years. The takeaway is that it’s all about time horizons. If you’re invested in the stock market, long periods of drawdowns shouldn’t necessarily be a baseline expectation, but they should be part of the plan. Coming out of the 1929 peak and Fisher’s comments from October 1929, those levels on the Dow wouldn’t be seen again for another 25 years! That type of drought should certainly not be a base case for investors, but it should provide some balance to a growing feeling of entitlement in some areas of the market where double-digit daily percentage gains are starting to feel like an Inalienable right.

Oct 14, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Pessimism never won any battle.” – Dwight Eisenhower

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If the market rallies on a bank holiday, does it count? Judging by the declines in US equity futures and cryptocurrency markets, it appears not. S&P 500 and Nasdaq futures point to a drop of about 1% at the open, which would erase about two-thirds of Monday’s gain. Declines in the crypto space look even scarier as Bitcoin drops 4% and Ethereum traded back down below $4,000 with a decline of nearly 7%.

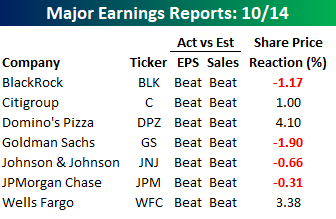

The catalyst for this morning’s weakness stems from continued trade tensions with China as both countries start charging additional fees on each other’s cargo ships, and China imposed further sanctions on certain US shipping subsidiaries. The weakness also comes even after a strong batch of earnings reports on what is really the first busy day of earnings for the Q3 reporting period.

As shown in the table below, of the seven major reports this morning, all seven reported better-than-expected EPS and sales, but only three are trading higher in reaction to the reports. Domino’s (DPZ), Wells Fargo (WFC), and Citigroup (C) are all up 1% or more, while Goldman (GS) leads the declines with a drop of nearly 2%.

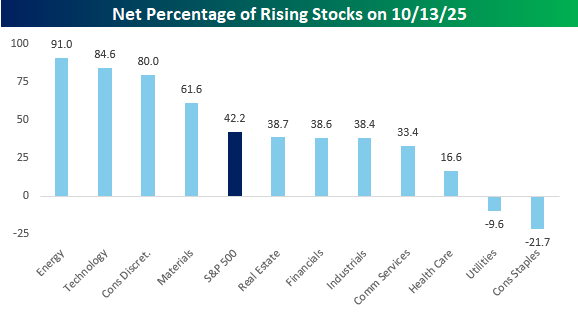

The S&P 500 had a good day to start the week yesterday, but breadth wasn’t exactly strong, especially for a day when the index rallied over 1.5%. As shown in the chart below, only four sectors saw a net of 50% or more of their components finish higher on the day. Energy and Technology led the charge with 90%+ of each sector’s components finishing higher on the day, while Consumer Discretionary (+80%) and Materials (+62%) were the only two other sectors where net breadth was stronger than the S&P 500. On the other end of the spectrum, Consumer Staples (-22%) and Utilities (-10%) both had negative net breadth, while Health Care also was relatively weak at just 17% net positive.

What was unique about yesterday’s trading, though, was that it was an extreme ‘inside’ day for the S&P 500 tracking ETF (SPY). An inside day in the market occurs when the intraday high for a day stalls out short of the prior session’s high, while the intraday low is higher. Not only did we have an inside day yesterday, but the intraday high was 1.3% below Friday’s high, while the intraday low was 1.1% above Friday’s low. We finished the day stuck right in the middle of the prior day’s range!

Inside days in SPY where both the intraday high and intraday low were more than 1% below or above the prior session’s extreme have been extremely rare. Since 1993, there have only been 11 other occurrences, with the most recent occurring back in April, right after the tariff-tantrum low. But before that, you have to go back to December 2020, and then before that, August 2015.

Oct 13, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Riches don’t make a man rich, they only make him busier.” – Christopher Columbus

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a bout of ferocious selling on Friday for stocks and into the weekend for cryptocurrencies, investors took some time to think things through over the weekend, and they’re taking a more optimistic tone. Futures on the S&P 500 are 1% higher, while the Nasdaq trades up more than 1.5%. Bonds are closed for Columbus Day, but gold is sharply higher with a gain of over 2% and trading just under $4,100 per ounce. Crude oil is also bouncing back with a gain of 1.5% but is still trading below $60. It certainly could be worse, but even with this morning’s gains, the S&P 500 is still down well over 1% from Thursday’s close. The President may not like to see the stock market trade lower, but all the talk with China seems to have taken the shutdown off the front page of the business section.

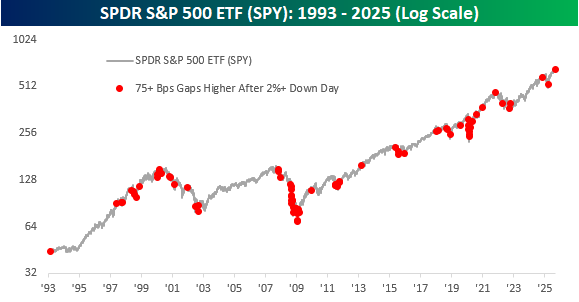

S&P 500 futures are still up over 1% but off their highs from earlier in the session. We looked at all prior periods when the S&P 500 SPDR ETF (SPY) fell 2% in a session and then gapped up at least 75 bps at the open the following day. We originally looked at 1% upside gaps, but with SPY now teetering on a 1% gain, we widened the band. The overall results of both analyses were very similar, though.

The long-term chart of SPY below shows every prior occurrence when SPY gapped up at least 75 bps after a 2%+ down day since its inception in 1993. While there were plenty of similar occurrences during the bear markets of 2000 to 2002 and 2008 into early 2009, there have also been plenty of other occurrences at various points in the market cycle.

Oct 10, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want a happy ending, that depends, of course, on where you stop your story.” – Orson Welles

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are modestly positive this morning following comments from potential Fed chair-in-waiting Christopher Waller, who said he expects the Fed to cut rates further this year, but at a ‘careful’ pace. Long-term treasury yields are notably lower as the 10-year yield trades down nearly 5 basis points to 4.10%. After dropping below $4,000 per ounce yesterday, gold is up nearly 1%, trading at $4,010. Crude oil prices are down over 1% on the prospects of peace in the Middle East, and crypto trades modestly higher at just about $121K.

With the government still shut down, the only economic data on the calendar is the University of Michigan Sentiment report, and Chicago Fed President Goolsbee will speak at a bank conference shortly after the open. Speaking of economic data, the BLS has recalled furloughed staff this morning to ensure that the September CPI report gets released by the end of the month.

Asian markets were weak overnight, with the notable exception of South Korea, which rallied 1.7%. Japan, Hong Kong, and China, however, were all down 1% or more. Japanese PPI increased 0.3% m/m, triple the rate of consensus expectations, solidified market expectations for another rate hike this year. Despite Friday’s decline, the Nikkei finished the week 5.1% higher while Hong Kong traded down 3.1% and China was up fractionally.

In Europe, equity markets have been much tamer this morning. The STOXX 600 is little changed, and no major country’s benchmark index is up or down more than 0.3%, and most are on pace to finish the week with modest gains or losses.

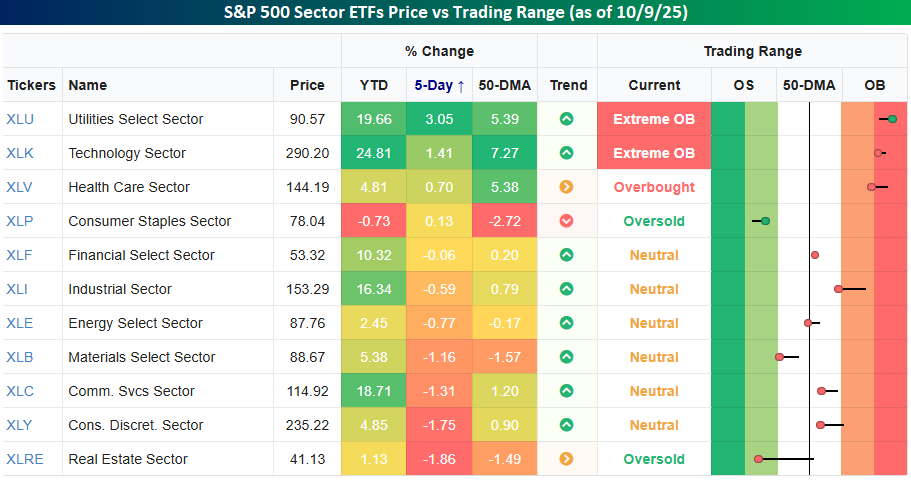

The last five trading days have been full of divergence at the sector level. The S&P 500 is fractionally higher, but seven out of eleven sectors have traded lower, including four sectors – Real Estate, Consumer Discretionary, Communication Services, and Materials – that are down over 1%. The only two sectors with gains of more than 1% are the formerly strange bedfellows of Utilities (3.05%) and Technology (1.4%). Both these sectors are also the only two trading at Extreme Overbought levels.

It wasn’t long ago that Utilities was considered the most defensive sector in the market, while Technology was considered the most risky sector. Like everything else now, it seems, AI has upended prior norms, although given the power-intensive nature of AI-related applications, the moves make sense.

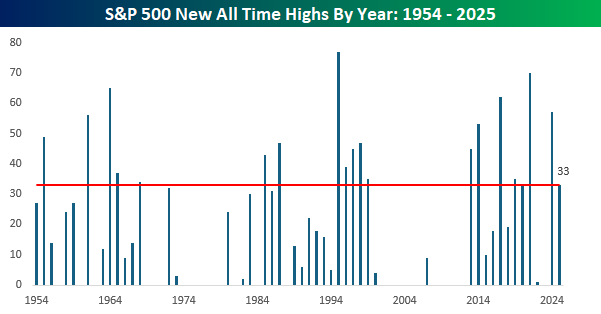

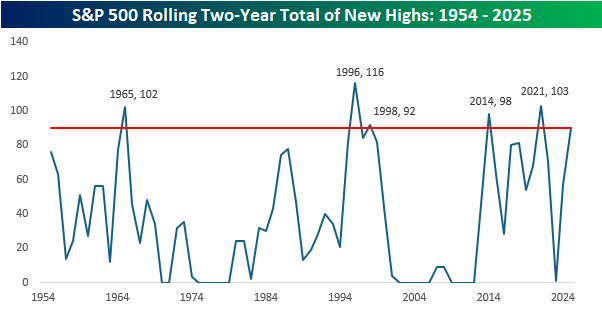

Yesterday was a down day for the S&P 500, but in the seven trading days this month, there have already been five record closes, taking the YTD total to 33. If the year were to end today, 33 record highs in a year isn’t particularly noteworthy as it ranks tied for the 19th most since 1954.

What’s been more impressive is that the 33 record closes followed last year’s total of 57. With 90 record closing highs in the last two calendar years, there have only been five other two-year stretches when the S&P 500 had more record closing highs, and not to jinx anything, but there’s a legitimate chance that by the end of the year, the last two years could end up ranking well into the top five.

Oct 9, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Reality leaves a lot to the imagination.” – John Lennon

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are flat with a negative bias this morning as the relentless rally in gold takes a pause, and oil prices see a marginal pullback. Stocks in Asia were higher overnight as China reopened for trading, and shares of Softbank surged more than 10% after announcing a deal to acquire the robotics units of ABB for $5.4 billion. In Europe, trading has been listless with the STOXX 600 down 0.04%.

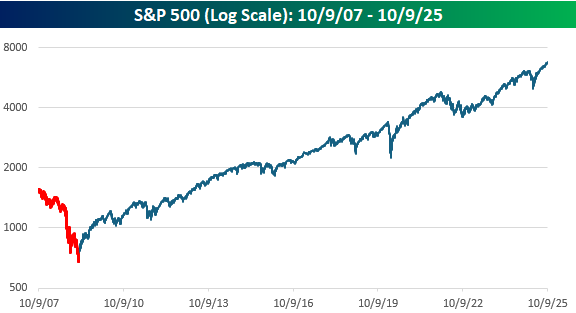

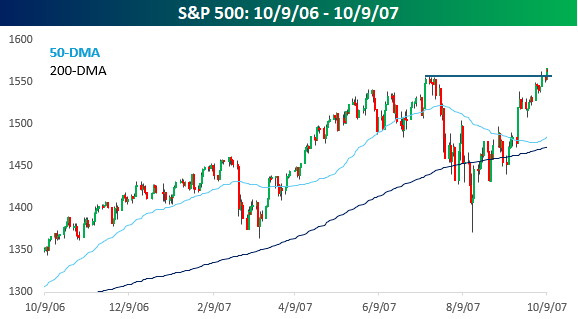

The S&P 500 closed at another all-time high yesterday, just like it did 18 years ago today on 10/9/07. That new high in 2007 followed a late-summer peak-to-trough correction of nearly 12%. It was a time of stress in the financial system as the subprime housing market was in the process of imploding, but the Fed was cutting rates, and the damage ‘appeared’ contained. From a technical perspective, the S&P 500 had traded above resistance to new highs, and the 50-DMA, which has been sloping downwards, turned higher just above its 200-DMA, which was also rising. The one caveat was that the breakout to new highs wasn’t especially convincing, as the S&P 500 had only made a marginal new high.

Investors breathed a sigh of relief on 10/9/07, but in the days that followed, the S&P 500 couldn’t follow through on its breakout, and within days, it was back below its summer 2007 highs. Shortly after that, the wheels came off, and the crash began. A year after the October 2007 high, the S&P 500 cratered more than 40%. As loud as the sighs of relief were in October 2007, they had nothing on VIX screamings towards 80 a year later as the entire banking system was on the verge of collapse.

The experience of October 2007 should serve as a reminder that even in the best times, investors should always be prepared for the possibility that the light at the end of the tunnel is a freight train steaming right at us. It’s only fitting this morning that on the anniversary of the 2007 peak, JP Morgan (JPM) CEO Jamie Dimon is in the news, warning of a correction in the market at some point in the next six months to two years. At first glance, that statement seems like something you would hear coming from Captain Obvious. Of course, there will be a correction in the next six months to two years! Stock market corrections occur on average about once a year, so there may actually be two!

If you read more into Dimon’s comments, though, he’s talking more about a serious bear market than a 10% correction. Even still, six months to two years isn’t really a precise forecast. While Dimon’s comments may not be of much use to investors or traders looking for any direction on where the stock market is going, they are exactly the kind of comments you want to hear from the CEO of America’s largest bank. That’s why JP Morgan Chase is just about the only major bank where the name on the CEO’s door is the same now as it was then. Dimon has earned the right to worry!

As bad as the declines were following the October 2007 high, as we always say when it comes to the market, time heals. It took several years, but eventually the market went on to make new highs, and this morning, the S&P 500 will open more than four times higher than it was when it closed at that peak 18 years ago.