Apr 26, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “Good ideas are always crazy until they’re not” – Larry Page

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Yesterday’s reversal was a welcome reprieve for bulls, especially after the straight line lower from early last Thursday. From a technical perspective, there’s not much positive to say about the charts of the S&P 500 and the Nasdaq, but to provide an optimistic scenario, we would note that both indices appear to be showing some signs of a reverse head and shoulders. It’s going to take a lot more upside to make these formations look more convincing, and the pattern for the Nasdaq is much looser than the pattern for the S&P 500, but we thought it was worth highlighting.

While the two largest US indices may, and we stress the word may, be showing early signs of a positive pattern, the semiconductors, which typically act as a leading indicator actually opened at their lowest level since Last May on Monday morning. That being said, like the broader market, the SOX did manage to turn things around finishing the day higher by just over 1.75% and outperforming the S&P 500 and the Nasdaq in the process.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Apr 25, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “Thus fear of danger is ten thousand times more terrifying than danger itself.” – Daniel Defoe, Robinson Crusoe

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Last week was a brutal one for US stocks as the Nasdaq, Russell 2000, and the S&P 500 fell at least 2.5%. Sector performance within the S&P 500 was also mostly lower but varied widely. Both Real Estate and Consumer Staples managed to finish the week higher, but every other sector was down at least 1% and in many cases a lot more. Thanks in large part to Netflix (NFLX), the Communication Services sector was down nearly 8%, while Energy, Materials, and Health Care all fell more than 3%. Despite the carnage last week, though, only three sectors head into the new week at oversold levels, and two are actually overbought.

What’s also interesting about last week’s declines was that the selling wasn’t confined to either just the year’s winners or losers. The two worst performing sectors are also the worst performing (Communication Services) and the best performing (Energy) year to date. In other words, there wasn’t a whole lot of rhyme or reason behind the weakness.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Apr 22, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “Interest rates are like gravity on valuations. If interest rates are nothing, values can be almost infinite. If interest rates are extremely high, that’s a huge gravitational pull on values.” – Warren Buffett

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

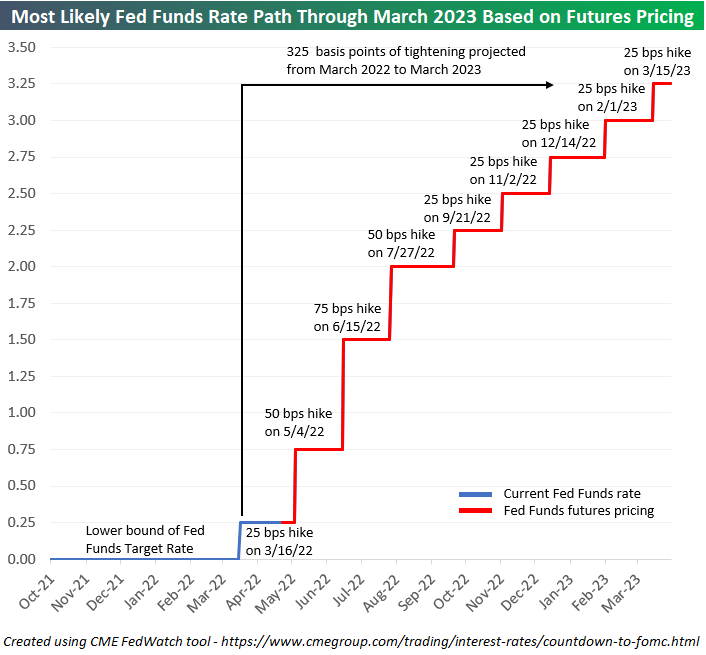

Yesterday’s market sell-off coincided with expectations for an even tighter Fed. As fed fund futures priced in a higher likelihood of tighter policy over the next year, equity prices fell. Below is a chart showing the expected path for the Fed Funds Rate (lower bound) through the March 2023 meeting. Pricing is now suggesting a 50 basis point hike at the May meeting, a 75 basis point hike at the June meeting, and another 50 basis point hike at the July meeting. That would take the Fed Funds Rate up to 2-2.25% (remember, it’s at just 0.25-0.50% now) by mid-July. Talk about a tight summer!

After the estimated 175 basis points of tightening through July, markets are pricing in five more consecutive 25 basis point hikes through March 2023, which would leave the lower bound of the Fed Funds Rate at 3.25%.

If we do see a Fed Funds Rate of 3.25-3.50% by next March, it will be tied for the steepest one-year of tightening since 1989:

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Apr 21, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “In trading, you have to be defensive and aggressive at the same time. If you are not aggressive, you are not going to make money, and if you are not defensive, you are not going to keep the money.” – Ray Dalio

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

As shown below, the 8 largest US stocks are all in the red so far this month for an average decline of 8.2%. The rest of the stocks in the large-cap Russell 1,000 are only down an average of 8 basis points.

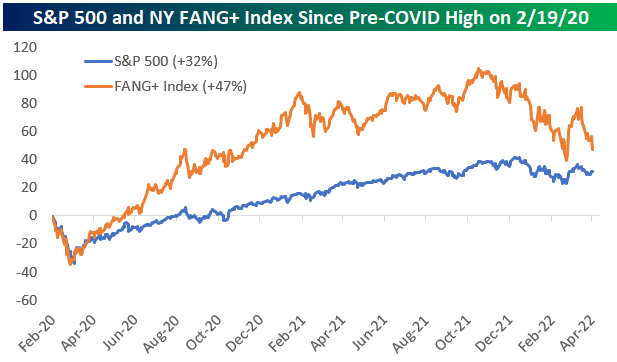

The FANG+ Index is made up of 7 of the 8 largest stocks listed above (excluding BRK/B), but it also includes Netflix (NFLX), Alibaba (BABA), and Baidu (BIDU). Since April 4th, the FANG+ index is down 17%, and it’s down 28% from its highs.

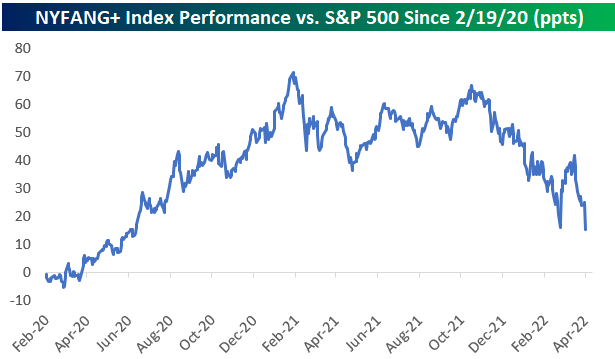

Below we show how the FANG+ index has performed versus the S&P 500 since 2/19/20 – the peak day for the US stock market before the COVID pandemic hit. FANG+ stocks exploded higher in late 2020 and peaked versus the S&P in early 2021 with an outperformance spread of more than 70 percentage points. That outperformance has been eroding rapidly since last November and the spread is only +15 percentage points now.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Apr 20, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “Companies rarely die from moving too fast, and they frequently die from moving too slow.” – Reed Hastings

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

We certainly aren’t going to see rotation into the Communication Services sector at the open this morning with Netflix (NFLX) trading down 25% on earnings. Based on where NFLX shares are trading pre-market, the stock will be in a 63% drawdown from its high just last November. As shown below, this is the fourth time since going public in 2002 that NFLX will have experienced a drawdown of at least 60%.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Apr 19, 2022

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “When something is important enough, you do it even if the odds are not in your favor.” – Elon Musk

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

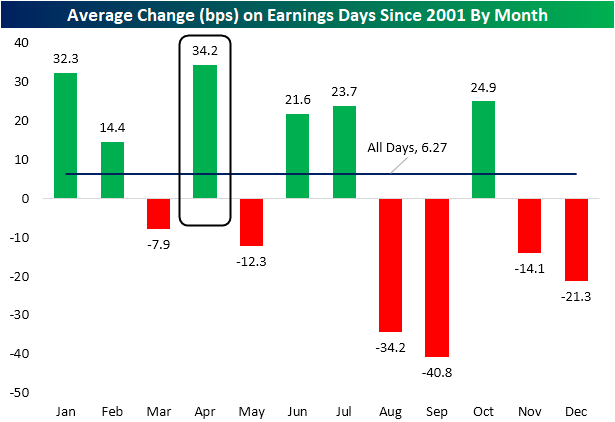

As earnings season ramps up, today we took look at how stocks have historically reacted to earnings reports from a seasonal perspective. The chart below shows the average one-day stock price reaction to earnings reports by month over the last 20 years. This data comes from our Earnings Explorer database that includes one-day share price reactions of more than 150,000 individual quarterly earnings reports dating back to 2001. As shown below, the average company that has reported quarterly earnings in the month of April has gained 34.2 basis points (+0.34%) on its earnings reaction day. That makes April the most bullish month for stocks reporting earnings. Conversely, August and September have been the two worst months to report earnings. Stocks that have historically reported quarterly numbers in August have averaged a one-day decline of 34.2 basis points (-0.34%) on their earnings reaction days. Stocks reporting in September have averaged an even bigger decline on their earnings reaction days (-0.41%). (For companies that report earnings in the morning before the open, its earnings reaction day is that same trading day. For companies that report earnings in the evening after the close, its earnings reaction day is the next trading day.)

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.