Dec 15, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life’s under no obligation to give us what we expect.”- Margaret Mitchell, Gone With the Wind

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a rough end to last week, bulls are shaking the dirt off their shoulders and looking to make a stand as we head into the final half of the month. Both the S&P 500 and Nasdaq are down fractionally so far this month, but with the seasonally strong second half of the month now here, will the bulls show up?

So far, they’re coming out on the offensive. Futures on all three of the major averages are higher by roughly 0.5%. The 10-year yield is moving lower and picking up in pace to the downside following a weaker-than-expected Empire Manufacturing report. Crude oil is fractionally higher, while gold and Bitcoin move higher.

Asian stocks started the week with broad-based losses. The South Korean Kospi led the losses with a decline of 1.8%, but both the Nikkei and Hang Seng finished down 1.3%. China also finished lower, but the losses were more contained at 0.6%. Besides follow-through from Friday’s losses in the US, the declines in the region also followed weak economic data out of China, where Industrial Production (4.8% y/y) and Retail Sales (1.3% y/y) both missed expectations.

Unlike Asia, European stocks are higher across the board with the STOXX 600 trading up 0.8%, with the UK, France, Italy, and Spain all up over 1% while Germany lags as peace talks in Ukraine continue to drag on.

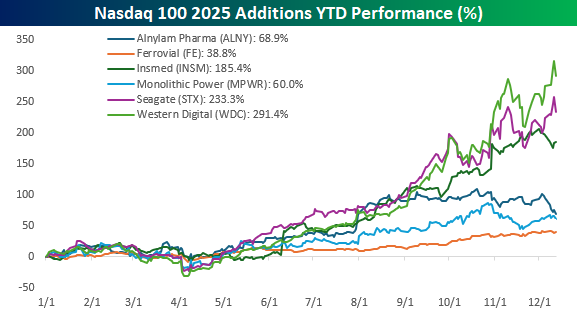

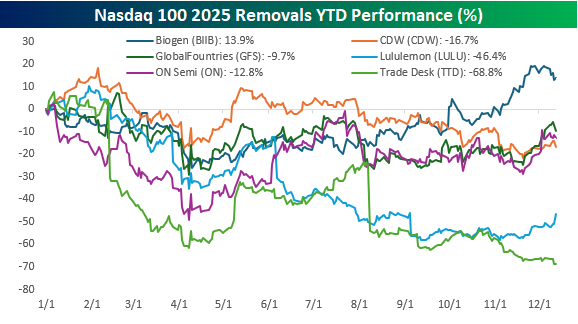

On Friday, Nasdaq announced the annual changes to the Nasdaq 100, and for this year’s shakeup, six stocks will be added and six removed. The new class of 2025 includes Alnylam Pharmaceuticals (ALNY), Ferrovial (FER), Insmed (INSM), Monolithic Power Systems (MPWR), Seagate Technology (STX), and Western Digital (WDC). The six stocks being removed to make room are Biogen (BIIB), CDW (CDW), GlobalFoundries (GFS), Lululemon Athletica (LULU), ON Semiconductor (ON), and The Trade Desk (TTD).

The two charts below show the performance of the six stocks being added and removed from the Nasdaq 100 on a YTD basis, and judging by their performance, one factor that appears to be part of the criteria is popularity. All six of the stocks being added this year have positive returns since the start of the year, and the median gain is 127.2%. Leading the way higher, Western Digital (WDC) and Seagate Technology (STX) have both rallied more than 200%. Even the worst performer of those stocks being added – Ferrovial (FE) – was 38.8%.

Turning to the six stocks being removed, they haven’t exactly shone this year. Five out of six of the stocks are down on the year, and the only winner – Biogen (BIIB) – is up only 13.9%. All totaled, the median performance of the six stocks is a decline of 14.8%.

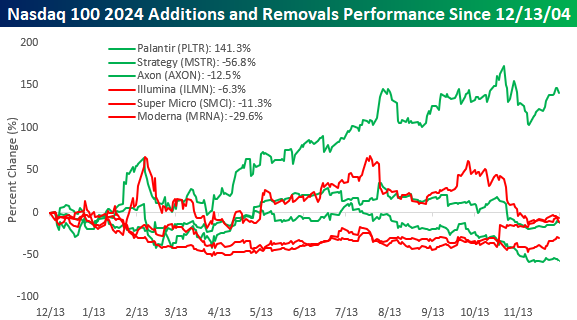

While six stocks are being added and removed this year, last year, there were only three. With one exception, the performance of both the stocks being added and removed from the Nasdaq 100 wasn’t particularly good. As shown in the chart below, shares of Palantir (PLTR) have rallied 141.3% since last year’s announcement that it was being added to the Nasdaq 100, but shares of Strategy (MSTR) and Axon (AXON) are both lower. Likewise, all three of the stocks removed last year are also lower, with declines in the range of 6.3% for Illumina (ILMN) to 29.6% for Moderna (MRNA).

Finally, since we’re talking about the Nasdaq 100, it’s worth pointing out that the index closed below its 50-day moving average again to close out last week as the latest rally off the November lows failed to make a higher high. With megacaps like Nvidia (NVDA), Microsoft (MSFT), and Oracle (ORCL) faltering recently, it’s showing up in the performance of indices they dominate, like the Nasdaq 100.

Dec 12, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Feel the city breakin’ and everybody shakin’, and we’re stayin’ alive, stayin’ alive” – Stayin’ Alive, Bee Gees

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to catch Bespoke co-founder Paul Hickey on Making Money with Charles Payne today at 2 PM Eastern on Fox Business.

Saturday Night Fever was released 48 years ago today, and when you think of that movie, “Stayin’ Alive” is the song that comes to everybody’s mind. With the S&P 500 closing at a new high yesterday, we can’t think of a song much better for the current market.

Ever since October 2022, the bull market has been ‘kicked around” by skeptics almost since the day it “was born.” The kicks came from all angles. Throughout the last three years, there have been repeated events that supposedly spelled the end of the AI rally. In the Summer of 2024, it was the unwind of the yen carry trade. Earlier this year, the haphazard rollout of US trade policy caused a tariff tantrum and raised concerns that Brand USA had lost its luster. Now, the fact that the Fed is cutting rates and rates at the long end of the curve aren’t falling has some arguing that the Fed has lost control.

With all these events and the scary headlines that accompany them, we can “understand the New York Times effect on man” and the potential to scare investors out of the market. Time after time (wait, that’s a Cyndi Lauper song), it felt like the market was “breaking and everybody shakin’”, but after the smoke cleared, that wasn’t Tony Manero on the dance floor striking the Disco Finger. No, that was the bull market hitting new highs and “ah, ah, ah, ah, stayin’ alive, stayin’ alive”.

Dec 11, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In today’s regulatory environment, it’s virtually impossible to violate rules.” – Bernard Madoff

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

17 years ago today, all hell was already breaking loose in financial markets as the banking sector had imploded three months earlier. Lehman’s bankruptcy accelerated a chain of failures and near-failures in some of the country’s most well-established banks. As if the market needed any more bombs hurled at it, along came the “Breaking News” interruptions on the news channels of a Ponzi scheme surrounding a man named Bernie Madoff. We’ve come a long way in the last 17 years, and after yesterday’s Fed meeting, the S&P 500 is back right near record highs and has rallied nearly 10-fold after accounting for dividends.

This morning, equity futures are taking a breather. Oracle (ORCL) earnings after the close last put renewed doubt on the AI trade, and the stock is down 13% as investors question whether the company can fund its ambitious capex plans. If that magnitude of decline, it would be the stock’s largest downside gap in reaction to earnings since at least 2001. Make sure to read our detailed discussion of ORCL earnings and investor concerns regarding the stock and the AI trade in the commentary section of today’s report.

After trading down close to 1% overnight, though, S&P 500 futures have rebounded and are now down just 0.3% while the Nasdaq is down 0.5%. Treasury yields are down another 3 basis points (bps) to 4.13%, and crude oil is down below $58 per barrel, falling over 1%. Gold is fractionally higher, but Bitcoin and other crypto assets have reversed all of their gains from the prior 24 hours.

In Asia, stocks traded mostly lower, with the Nikkei down 0.9% and South Korea down 0.6% as ORCL’s earnings dragged on the region. In Europe, though, we’re seeing modest gains across the board with the STOXX 600 trading 0.2% higher.

In the US, the only economic data release on the calendar this morning was jobless claims. Initial claims came in higher than expected at 236K (versus 220K), erasing all of last week’s surprising decline. Meanwhile, continuing claims showed a sharp decline, falling to 1.838 million, or 100K less than expected. The continuing claims number is lagged a week, so the sharp drop in initial claims last week was likely a holiday quirk.

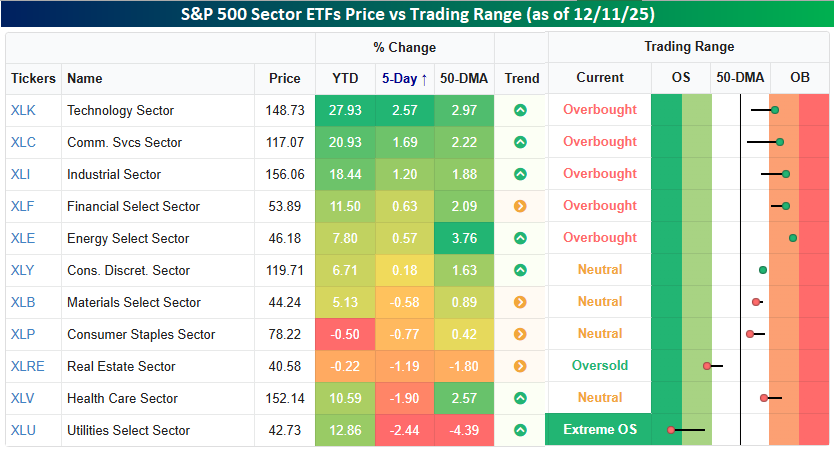

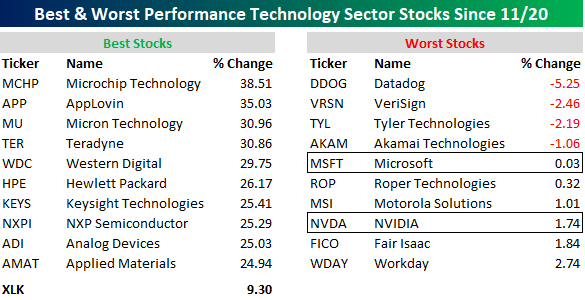

The S&P 500 closed within fractions of a new high yesterday, and the same sectors that have driven the market this year are the ones that have driven the rally over the last week. As shown in the snapshot below, Technology, Communication Services, and Industrials are the only two sectors up over 1% in the last five trading days, and they’re also the three best-performing sectors this year.

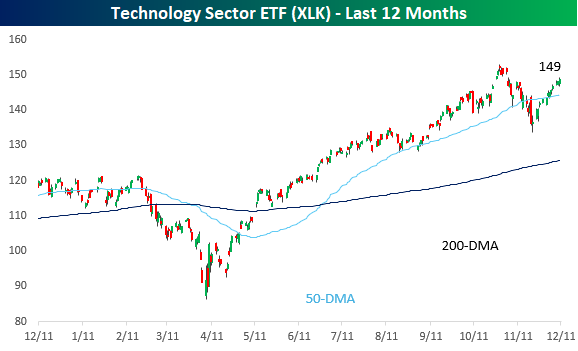

While the S&P 500 closed within whiskers of a new high and tech has led the rally, the Technology sector still has a ways to go before hitting a new high, as yesterday’s close was more than 2% below the late-October high. What stands out about the chart, though, is how much green there has been in the candles since the November low.

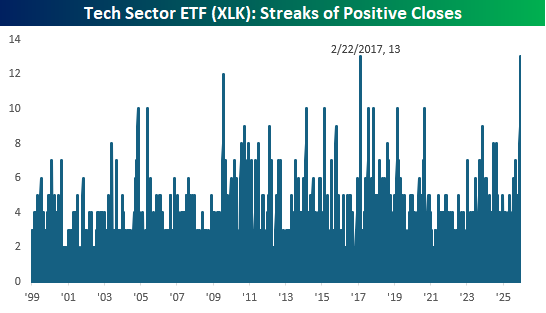

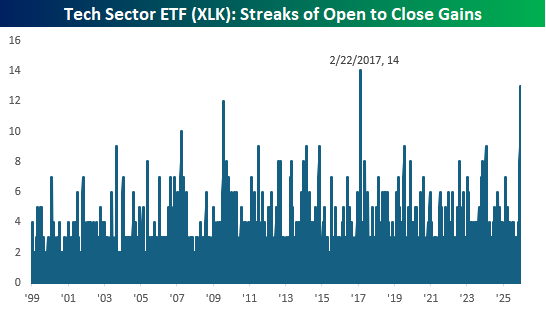

In fact, with 13 straight days of gains and 13 straight days of positive returns from the open to close, the Technology sector ETF (XLK) is knocking on the door of history. The 13 days in a row of daily gains are tied for the longest in the ETF’s history, dating back to 1999. The only other streak as long ended in February 2017. Similarly, the streak of open-to-close rallies is just one shy of the 14-day streak that also ended in February 2017.

What surprised us most about the Technology sector’s recent run is the stocks that have been driving the bus. Nine Technology sector stocks are up over 25% since the close on 11/20, and the majority are semiconductor stocks. One semi-stock not on the list of winners, though, is Nvidia (NVDA). While it’s not down since 11/20, NVDA’s 1.74% gain ranks as the eighth-worst performance in the sector. Also on the list of laggards is Microsoft (MSFT), which is barely higher since 11/20 (+0.03%). These two stocks collectively account for about 25% of the entire Technology sector, but as they have tread water over the last two weeks, the sector they dominate has still rallied over 9%. Is the baton being passed?

Dec 10, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I am in a charming state of confusion.” – Ada Lovelace

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

On a Fed day, we’d normally say that wherever the futures are in the pre-market, don’t expect the market to be there after the decision is announced, let alone after Powell talks. Based on recent history, though, volatility on Fed days has been muted. As we noted in today’s Chart of the Day, the S&P 500’s average absolute daily change on the last five Fed days has been among the most muted relative to any other rolling five Fed day period since 1994. So, maybe the muted moves in futures markets are on to something!

Outside of equities, the 10-year yield is up 2 bps and back above 4.2% as part of a global move higher yields. Crude oil prices are also up fractionally but still below $58 per barrel, while the slide in natural gas continues as prices break below $4.50. Metal prices are all over the map as gold prices are slightly lower, while silver rallies over 1% and platinum falls over 1%. In the crypto pace, it’s also a mixed but downwardly biased morning as bitcoin falls 1%.

International markets have also been quiet overnight and this morning ahead of the Fed, as most major benchmarks saw, or are seeing, modest declines. Chinese CPI was weaker than expected, falling 0.1% versus forecasts for an increase of 0.2% while PPI in Japan was right in line with forecasts.

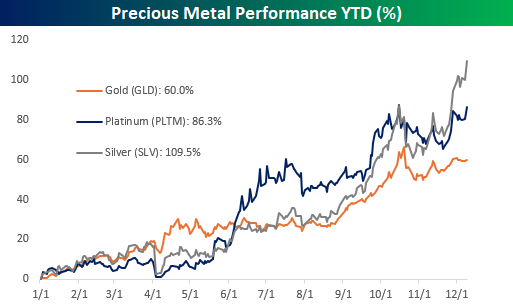

Warren Buffett has famously said of gold that it “gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again, and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.” While other precious metals like platinum and silver have more industrial uses than gold, based on public records, it has been decades since Buffett has been active in them. The primary reason Buffett has generally avoided commodities is that they are essentially a bet on future supply and demand rather than income-generating assets.

While they don’t produce income, precious metals are commodities that have produced massive capital gains this year. Gold (GLD) has rallied 60%, and those gains look modest relative to the 86.3% gain in platinum (PLTM) and the massive 109.5% gain in Silver (SLV).

For all three precious metals, the YTD gains would be enough to rank near the top of the list in terms of YTD performance. With its 109.5% gain, SLV would be the tenth-best stock in the S&P 500 this year, ahead of Intel (INTC) and behind AppLovin (APP). Nothing against AppLovin and its prospects over the next several years, but 100 years from now, which do you think has a better chance of still being around in its current form? Silver or AppLovin?

While the gains in Platinum and Gold wouldn’t crack the top ten in terms of performance, the former’s 86.3% gain would rank as number 14 in the S&P 500, while Gold would rank number 34.

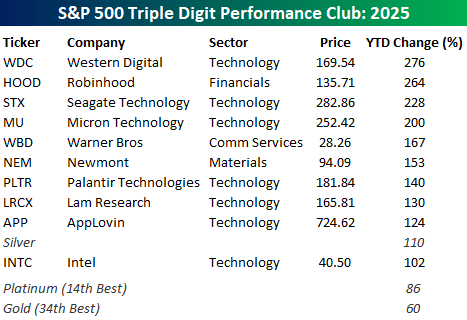

Looking at the ten best-performing stocks in the S&P 500 this year, all of them are up by at least 100%, and all but three are from the Technology sector. The top four performing stocks have not only had triple-digit returns, but they’ve also at least tripled! Sticking to the commodities theme, three of those stocks – Western Digital (WDC), Seagate Technology (STX), and Micron (MU) – all make data storage and memory products, which in the universe of the technology sector have for years been considered commodities as well.

Dec 9, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Lesson Number One: Don’t Underestimate The Other Guy’s Greed!” – Frank Lopez, Scarface

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Bespoke’s Paul Hickey will be on CNBC’s Squawk on the Street today at 10 AM. Make sure to check it out!

Markets remain on snooze with little conviction in either direction this morning, and while investors “waiting for the Fed” has been the excuse, is there really any question over what Powell will say and do tomorrow? Futures are as close to unchanged as you can really get this morning, with the S&P 500 indicated to open up 1 point (0.18%) while the Nasdaq is faring “significantly” worse, down 0.06%. As we wait for the Fed, there is some economic data today. Small Business sentiment hit the tape earlier and came in modestly higher than expected, while JOLTS will hit the tape at 10 AM.

Overnight in Asia, it was a ho-hum session with the Nikkei up 0.1% while China, South Korea, and India were all down fractionally (less than 0.5%). The RBA left rates unchanged but had a hawkish tone. In Europe, the STOXX is down 0.1%.

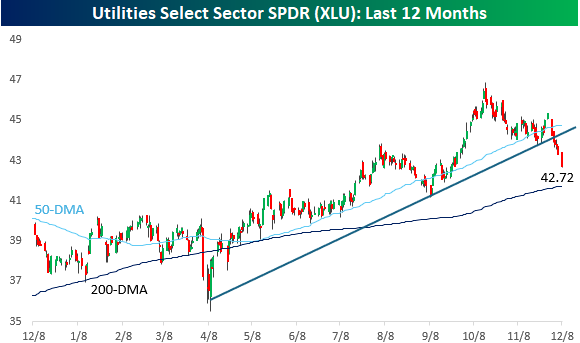

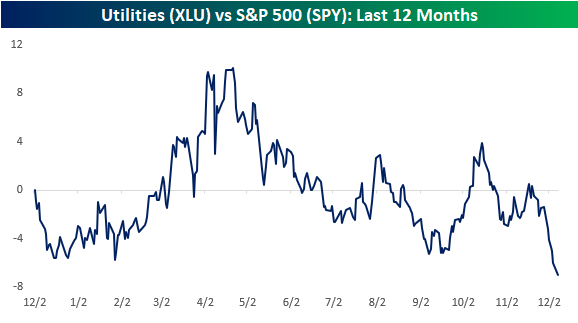

We had a power outage at the Bespoke offices yesterday afternoon, and coincidence or not, have you seen a chart of the Utilities sector recently? After being one of the better performing sectors this year, the sector started to fall on hard times since mid-October, to the point where in late November it broke its uptrend from the April lows. From there, the weakness in the sector picked up in intensity. The fact that longer-term interest rates have been rising hasn’t helped.

The recent weakness in the sector has also brought its relative strength versus the S&P 500 to a new low for the year. After handily outperforming during the tariff-tantrum in the Spring, the sector started performing in line with the broader market. For much of the last six months, its relative strength oscillated above and below the neutral line, but the last two weeks have seen it make a new leg lower.

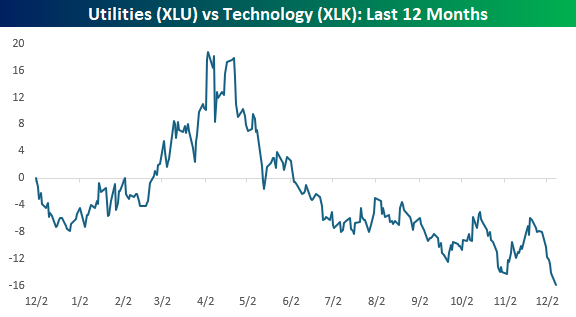

Given the power demands of AI, there have been times in the last few years when Utilities have been considered a technology play, but when you compare the sector’s performance to the Technology sector, it’s not even close. Utilities have been trending lower for the last six months.

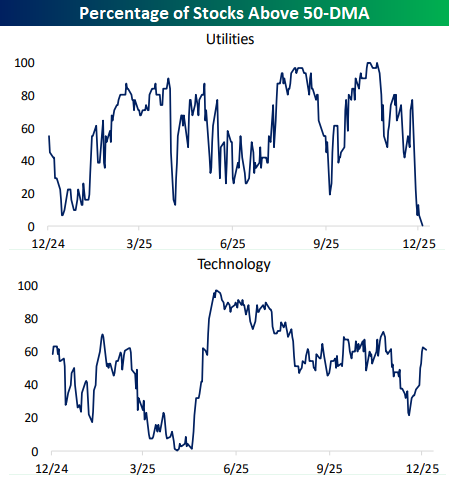

The disparity is also apparent when you compare the percentage of stocks in each sector trading above their 50-day moving averages. The Utilities are experiencing a “blackout” in this metric as not a single sector closed above its 50-DMA yesterday. That compares to more than half of stocks in the Technology sector. After some trial and error last night, Con Ed finally got the power back on in our offices last night, now they need to work on getting some power back to the sector!

Dec 8, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’ve noticed that when people are joking they’re usually dead serious, and when they’re serious, they’re usually pretty funny.” – Jim Morrison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As investors await Wednesday’s Fed meeting, there’s a modestly positive bias to futures as the S&P 500 knocks on the door of a new high. There’s no economic data on the calendar, so the main area of focus is Wednesday’s Fed meeting, where the market is pricing in a greater than 90% chance of a 25 bps rate cut. While a rate cut is a near certainty, the odds of another cut in January are relatively low, and the consensus is that Powell’s commentary will be hawkish.

Stocks in Asia got off to a mixed start on little news. The Nikkei finished marginally higher, but Hong Kong was down over 1% and China was up fractionally as export data showed a 5.9% y/y increase versus forecasts for growth of just 3.8%. Japan’s Q3 GDP was weaker than expected, falling 0.6%, so the slower growth, coupled with higher inflation, spells out a tough recipe for the BoJ.

European stocks are also showing little direction this morning as the STOXX 600 is little changed, and no individual country benchmark index is up or down 0.3%.

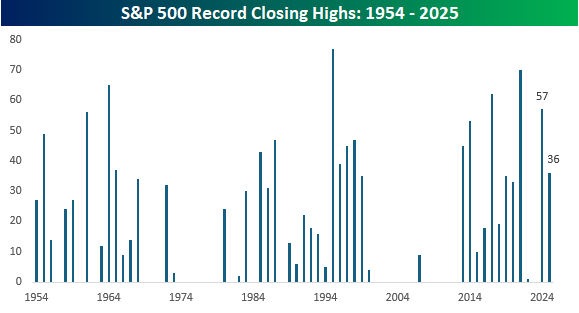

It’s been 28 trading days since the S&P 500 last closed at a record high right before the Fed’s last meeting and Powell’s hawkish cut on 10/29. As we approach this Wednesday’s meeting, though, the S&P 500 is just 30 bps from that October high and its 37th record closing high of the year. With just 17 trading days left this year, even if we hit a record high on every remaining day this year, it wouldn’t be enough to overtake last year’s total of 57, but even if there wasn’t another record high again this year, 36 is still an impressive total.

Since 1953, when the five-trading-day week in its current form started, the average number of record closing highs by year is 18.5. As the chart below illustrates, though, the number can vary widely. In 28 of the last 73 years, there have been no record highs, so there were plenty of valleys after deep bear markets where the market had to rally back over the course of years to dig out of its hole. Earlier this century, there was a six-year drought from 2001 through 2006, and then after just nine record highs in 2007, there was another five-year drought from 2008 through 2012.

Since 2013, there has been just one year without any record highs, while there was just one in 2022. This chart, more than anything, illustrates the nature of the secular bull market US stocks have been in for the last decade or more. As the chart illustrates, though, these periods don’t last forever.

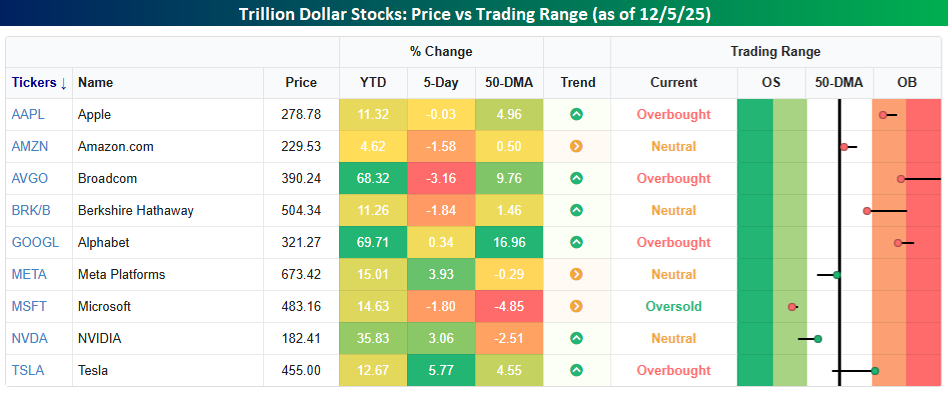

Whether the new highs start flowing again will likely be dictated by the performance of the trillion-dollar stocks. Collectively, the nine stocks in the S&P 500 with market caps of at least a trillion account for nearly 40% of the S&P 500. What’s interesting to note about these nine stocks is that while they’re all up YTD, only three of them – Alphabet (GOOGL), Broadcom (AVGO), and Nvidia (NVDA) – are outperforming the S&P 500 YTD. Not only that, but last week, more than half of them were down, so it’s not as though the group, as a cohort, has become wildly extended. Certain stocks may be overbought in the short-term, but there are also stocks like Meta (META), Microsoft (MSFT), and NVDA that head into the week below their 50-DMAs.