Apr 28, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“People generally see what they look for, and hear what they listen for.” – Harper Lee

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Sentiment surrounding AI is really something these days. On one day, you can have stocks surging on the idea that companies can’t get their hands on enough compute, and then the next day, they sell off sharply because there’s not enough demand. It’s like the line from The Rime of the Ancient Mariner, “Water, water, everywhere/Nor any drop to drink”. This morning, the Nasdaq is leading futures lower on a report in the Wall Street Journal that OpenAI missed year-end user and revenue targets, raising questions over whether all of the investments in the sector will eventually pay off. These are legitimate questions to ask, but if the article is based on year-end 2025 targets, a lot has changed between now and then regarding OpenAI’s growth (Codex) and the sector.

Nasdaq futures are currently down more than 1% while the S&P 500 is indicated 0.65% lower, while oil prices have surged more than 5%, taking WTI back above $100 per barrel. The impact of that increase in oil prices can’t be overstated either. While oil prices surge, gold prices are sharply lower (-2.6%), while Bitcoin is down less than 1%.

In Asia, stocks were mostly lower, with South Korea being the only exception (+0.4%). Japan and Hong Kong were both down 1% while China declined only 0.2%. The BoJ left its policy rate unchanged, but it was a fractured vote with three of nine voters pushing for a rate hike.

In Europe, it’s a mixed picture. With much less tech exposure than the US, the STOXX 600 is unchanged on the session while Italy leads the way higher (+0.9%) and Germany lags (-0.2%).

In the US today, it’s a relatively quiet day for data with the FHFA House Price Index at 9:00, and the Richmond Fed and Consumer Confidence reports for April hitting the tape at 10 AM.

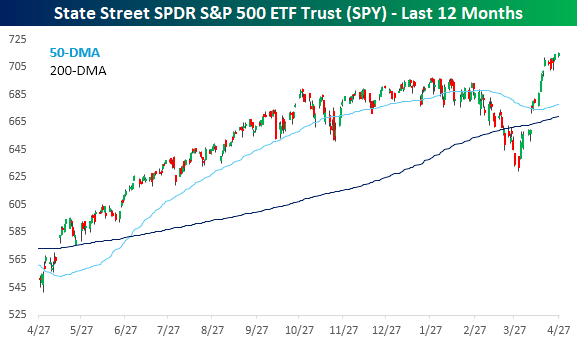

The S&P 500 hit both a new intraday and a closing high yesterday as the bull market continues to reconfirm itself with six closing record highs since 4/15. The index has had a parabolic run this month, and while a pullback or consolidation wouldn’t surprise anyone, the index should find decent support at the prior highs from late last year/early this year.

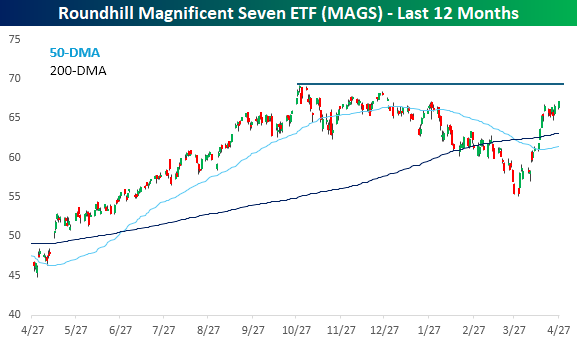

Over the last several years, whenever the market hits new highs, we look to see what’s driving the move higher. Is it the mega-caps or the rest of the index? Starting with the mega-caps, it’s been a strong month for the group, and while the group rallied nearly 1% yesterday to provide some positive momentum, it remains well below its prior all-time highs from last fall. At yesterday’s close of $67.08, the MAG7 ETF (MAGS) is still nearly 3% below its prior peak.

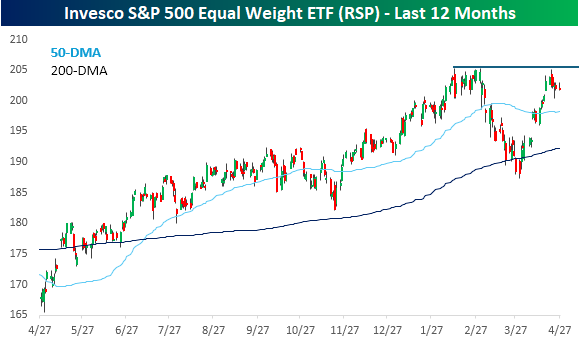

The equal-weight S&P 500, which more accurately reflects the performance of the “S&P 493”, traded down fractionally yesterday, so while it didn’t contribute at all to yesterday’s rally, it is actually much closer to all-time highs than the MAG7 ETF. In any event, though, it’s interesting to see that both the S&P 500 Equalweight and the MAG7 ETF closed more than 1% below all-time highs yesterday, even as the index itself hit a new one.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 27, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Judge a man by his questions rather than his answers.” – Voltaire

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

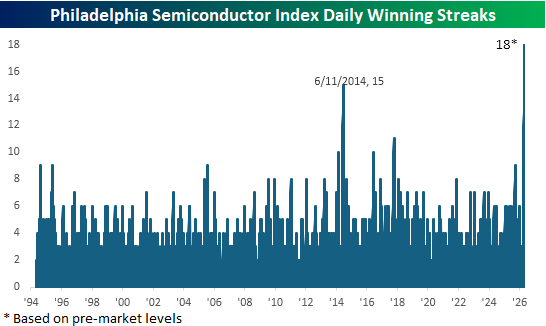

Nasdaq futures are up once again this morning as semis rally another 1.5% in pre-market trading. As a reminder, the Philly Sox semis index is on an 18-day win streak and hasn’t had a down day this month! Meanwhile, traders continue to sell software stocks with the ETF that tracks the group (IGV) down about half a percent ahead of the open. One day soon we expect the long semis/short software trade to unwind; it’s just a matter of when.

As we noted in Friday’s Bespoke Report (read it here if you missed it on Friday), even though the cap-weighted large-cap index ETFs like SPY and QQQ have broken out to new all-time highs, the S&P 500 Equal Weight ETF (RSP) looks quite different.

As shown in the lower left chart below, RSP attempted to break out but failed at resistance. On Friday, SPY rallied 0.8% even though breadth was -146 and the average stock in the index was down 0.2%.

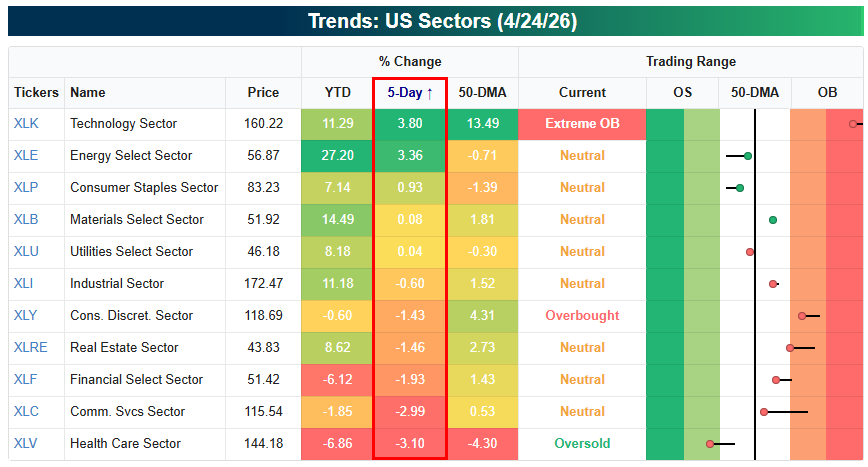

While the Tech-heavy Nasdaq 100 (QQQ) rallied more than 2% last week, the S&P 500 (SPY) was only up 0.5%, and there were actually more sectors down (6) than up (5).

Health Care (XLV), Communication Services (XLC), Financials (XLF), Real Estate (XLRE), and Consumer Discretionary (XLY) were all down more than 1%.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 24, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Let chaos reign, then rein in chaos.” – Andy Grove

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The rally continues to roll this morning as the S&P 500 looks to gap up 0.50% at the open, while the Nasdaq is up nearly triple that amount on the back of strong earnings, specifically from Intel (INTC). There’s also been some positive news out of the Middle East on reports that both the US and Iran will return to the bargaining table. Along with higher stock prices comes lower oil prices as WTI crude trades down 1.5% to $94.45 after trading as high as $97 earlier. Gold prices are unchanged, and Bitcoin is up nearly 1%.

Overnight, Asia was mixed. The Nikkei finished the last session of the week with a gain of 1%, doubling its week-to-date gain, while South Korea was little changed, keeping its weekly gain at just over 4.5%. China was slightly lower on the session and finished the week up less than 1%.

In Europe, stocks are generally lower, sitting out the tech-fueled rally that US stocks are likely to see at the open. The STOXX 600 is down less than half a percent, but will finish the week down over 2% even as the S&P 500 looks to finish the week higher.

Getting back to the US, it’s a quiet day for economic data with Michigan Sentiment the only report on the calendar. Earlier this month, the flash reading came in at a record low. That’s noteworthy because if those preliminary levels hold, it would be the first time that this index ever hit a record low in the same month that the S&P 500 hit an all-time high. There seems to be a disconnect somewhere.

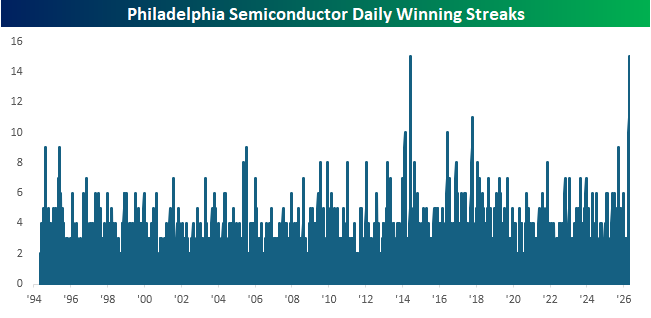

It’s time to dust off the 10,000 hats again, not for the Dow but the SOX. For the first time, the Philadelphia Semiconductor Index (SOX) closed above 10,000 yesterday, and this morning, the Transports of the 21st Century are on pace to trade another 2.8% higher. We’ve been discussing it a lot recently, so excuse us for beating a dead horse, but the SOX is now on pace to trade higher for a record 18 straight trading days. The only other streak that was anywhere nearly as long was in June 2014, when the index traded higher for 15 straight days.

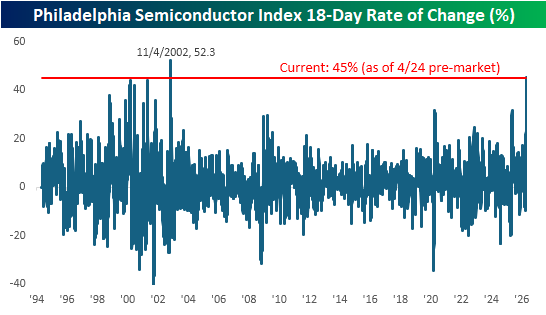

Just as incredible as the 18-day winning streak is the magnitude of the gain during this streak. If the current gains hold through the end of the day, the SOX will have rallied 45% in the last 18 trading days. We’ll say that again, 45%! Even for a volatile index like the SOX, there has only been one other 18-day period in the index’s history when it gained more, and that was coming out of the dot-com crash lows in Q4 2002, when the index was 97% lower than it is now!

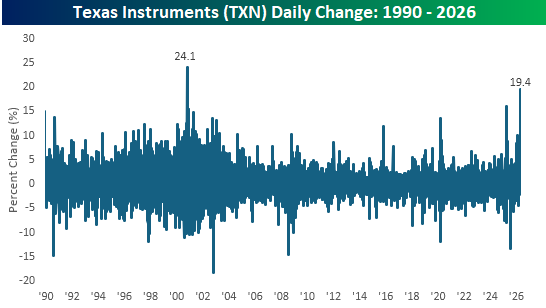

We mentioned the term “dead horse” above, and surprisingly, it’s been stocks that were considered left for dead driving most of the gains. For starters, during yesterday’s session, Texas Instruments (TXN) rallied 19.4% on the back of its Q1 earnings report. Since 1990, there has only been one other day when the stock rallied more, and that was in October 2000.

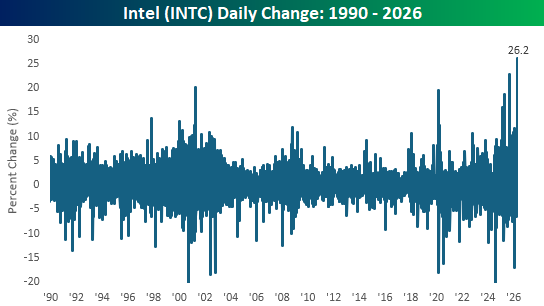

As mentioned above, today’s driver of the semis rally is Intel (INTC). After an earnings triple play yesterday, the stock is trading up over 26% in the pre-market, which would rank as the stock’s best day since at least 1990. While the old guard of semis has been rallying, the AI bellwether of the group, Nvidia (NVDA), continues to lag, at least relatively speaking. Since the 3/30 low for the SOX, NVDA is up “only” 20%, or less than half as much as the index, in which it is easily the largest component by market cap.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 23, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Better three hours too soon than a minute too late” – William Shakespeare, The Merry Wives of Windsor

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Squawk on the Street yesterday to discuss energy, midterms, and the markets. To view the segment, click on the image below

Equity futures traded sharply lower overnight on concerns of renewed military action in the Middle East. Since then, the negative sentiment has receded on reports out of China that the US and Iran will return to the bargaining table, and futures are well off their lows. S&P 500 and Nasdaq futures are now flat, while the Dow, being dragged lower by a decline in IBM, is indicated to open down 0.35%.

Treasury yields are marginally higher this morning, with the 10-year yield ticking above 4.30%, while crude oil is now lower after trading much higher overnight. Gold prices are fractionally lower, and Bitcoin is still down 1.5% at just under $78K.

Asian stocks were mostly lower overnight, with South Korea the standout gainer among a sea of red. Higher oil prices were the primary driver of the weakness. In terms of economic data, though, flash PMI readings for April in Japan, India, and Australia came in higher than expected. European stocks are also trading tentatively this morning as the STOXX 600 trades down 0.3%, with France the only gainer. Like Asia, the flash PMI reading for the Eurozone Manufacturing also unexpectedly showed an acceleration.

Besides the pickup in earnings flow, the economic calendar is busy this morning with jobless claims at 8:30, flash PMI readings at 9:45, and then the KC Manufacturing report at 11 AM. On the sentiment front, if should come as no surprise that AAII’s weekly survey saw a big uptick in bullish sentiment, rising from 31.7% up to 46.0%, which isn’t far from the 52-week high of 49.5% in January.

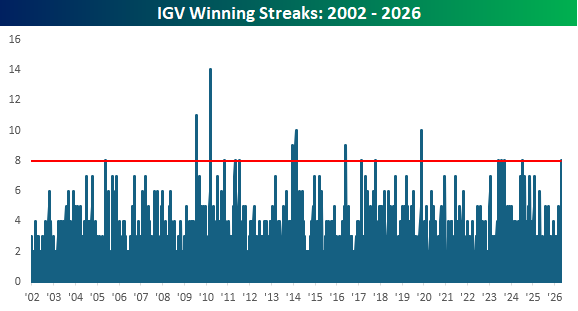

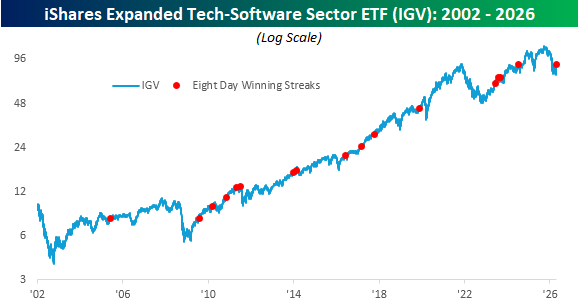

Semis and software have generally moved in opposite directions this year, but over the last several days, both have moved higher. Semis extended their streak of daily gains to a record 15 trading days yesterday, and the streak in software stocks has been half as long. As shown in the chart below, the iShares Expanded Tech Software Sector ETF (IGV) has traded higher for eight straight days, making it tied for the longest daily winning streak since late 2019. With the ETF trading down close to 3% this morning, though, we wouldn’t bet on the streak extending to a ninth day.

The chart below shows a long-term look at IGV’s performance, with red dots showing every prior eight-day streak. Only once, in the summer of 2011, did one of these streaks coincide with a notable peak in the sector, as the majority occurred within various stages of longer-term uptrends. This current streak has been somewhat unique in that IGV is trading so close to a low.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 22, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When you sell your great companies and add to the losers, it’s like watering the weeds and cutting the flowers.” – Peter Lynch

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to check out Paul Hickey on CNBC’s Squawk on the Street today at 10:30 Eastern.

It looks like a two-day losing streak was all the Nasdaq needed to recharge from the impressive 13-day streak the index ripped off from the March lows. Following news that President Trump extended the ceasefire with Iran, Nasdaq futures point 0.75% higher while the S&P 500 looks to gap up 0.60% at the open. Treasury yields are lower, with the 10-year hovering near 4.27%, while crude oil and gold rally by 0.50% to 1.0%. The star of the show this morning is Bitcoin, which is up over 4% and trading back above $78K, the highest level since early February.

In Asia, it was a mixed session overnight with the Nikkei up 0.4% and the Kospi adding 0.5%. Hong Kong and India, however, both finished down over 1%. European stocks aren’t looking as positive. The STOXX 600 is slightly lower, with Spain leading the losses, declining 0.5%. In both regions, the key driver of the moves has been Iran and its impact on energy prices.

Here in the US, it will be a quiet session for economic data, but the pace of earnings continues to pick up steam. Some of the more notable reports since the close yesterday include Boeing (BA), Capital One (COF), GE (GE), and United (UAL), and after the close, IBM, Tesla (TSLA), Texas Instruments (TXN), and United Rentals (URI) will be the headliners.

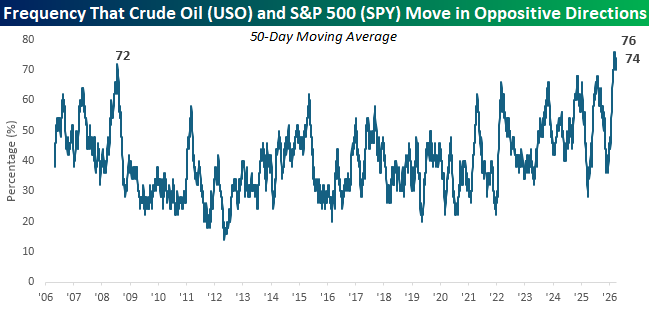

The fact that equity futures and crude oil are trading higher this morning is uncommon relative to recent history, especially since the war started. Over the last 50 trading days, the crude oil ETF (USO) and the S&P 500 ETF (SPY) have traded in the opposite direction (up or down) 37 times (74%). Since the ETF launched in 2006, this is right near the record high of 76%, reached less than two weeks ago on April 9th. Before this current period, the last time the correlation between the two ETFs was at comparable levels was in the summer of 2008, during the early stages of the financial crisis.

Shifting from crude oil, the fuel of the physical economy, to the fuel of the digital economy, semiconductors continued to roll yesterday as the Philadelphia Semiconductor Index (SOX) traded higher for the 15th straight day, tying the record from June 2014. Besides these two periods, there have only been three other periods where the SOX even had a ten-day winning streak.

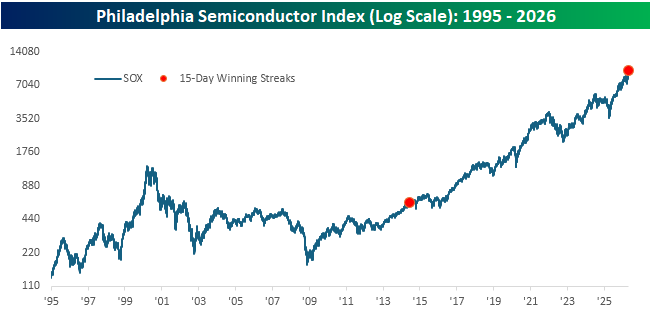

Below we show a long-term chart of the SOX showing when the prior 15-day winning streak occurred with a red dot. That streak capped off a longer run of gains for the index, and while it continued to rally, the pace of the ascent started to slow. From a longer-term perspective, though, it’s amazing to think that in the 12 years since that streak, the SOX has doubled and then doubled again and then doubled again and doubled once more for a total gain of 1,500%. Not bad for 12 years!

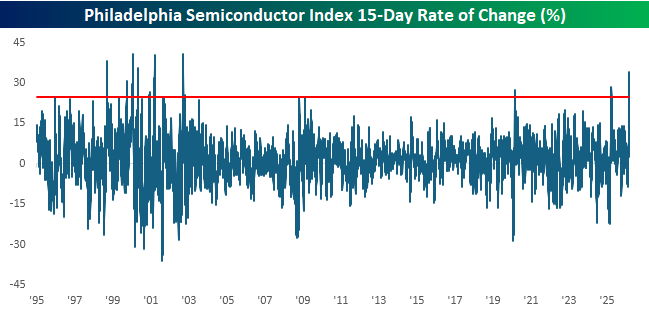

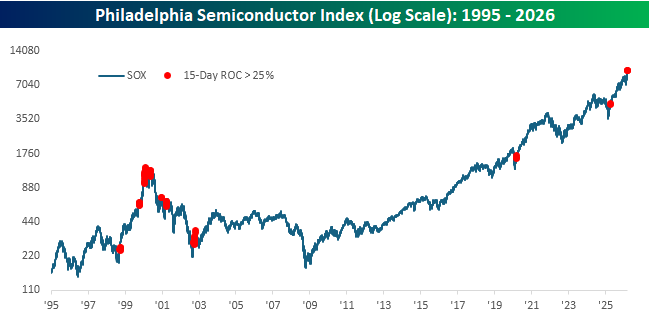

What’s just as impressive as the SOX’s 15-day winning streak is the 34% rally it has experienced during that span. That’s the largest 15-day gain for the index since October 2002, coming out of the dot-com lows. As shown in the chart, these types of moves were somewhat more common during the late 1990s and early 2000s, but have been very uncommon since.

Again, looking at these occurrences on a long-term chart of the SOX shows that most were exclusive to the period after the 1998 Russian Debt Crisis through the lows of the dot-com crash. Since then, the only two others were coming out of Covid and the tariff-tantrum. What has also been uncommon is for these moves to cap off rallies to all-time highs. That only occurred in late 1999 and early 2000. Gulp.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Apr 21, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Success flourishes only in perseverance — ceaseless, restless perseverance.” – Baron Manfred von Richthofen

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The Nasdaq may have broken its 13-day winning streak yesterday, but it’s looking to start a new one this morning. Futures on the S&P 500 and Nasdaq are both up nearly 0.5%, while the Dow, powered by a 7% rally in UnitedHealth Group (UNH), has that index on pace to gap up 0.65% at the open. Treasury yields are slightly higher, with the 10-year yield just under 4.26%, while crude oil is fractionally lower at just under $90 per barrel. All in all, it’s been a quiet overnight session as markets await the outcome of the latest on-again, off-again peace talks between the US and Iran. President Trump will also be interviewed on CNBC at 8:30, so investors will be focused on that for any potential headlines. Will he be talking about Iran, Kevin Warsh, or maybe even “Tim Apple’s” retirement?

In international markets overnight, Asian stocks were higher across the board, with South Korea surging 2.7% to a new record high and erasing all its 20%+ decline from late in the first quarter. European stocks are also trading with a positive bias, with the STOXX 600 0.2% higher, led by Germany and Spain, which are up 0.5%.

On the US economic calendar this morning, we’ll get Retail Sales at 8:30, and then Business Inventories and Pending Home Sales at 10 AM. The earnings calendar will also continue to pick up after the close with Capital One (COF), Intuitive Surgical (ISRG), and United Airlines (UAL) all on the calendar.

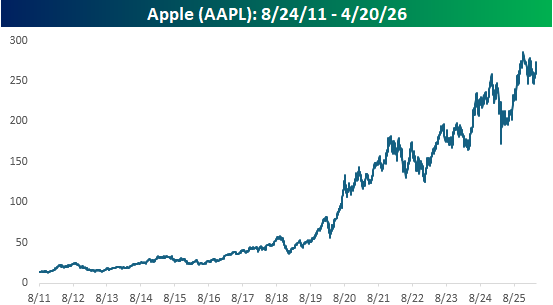

One of the world’s largest companies marked the end of an era last night when Apple (AAPL) announced that CEO Tim Cook would retire effective September 1st, just over 15 years after taking the helm in August 2011. During Cook’s tenure, AAPL’s stock rallied more than 1,900%, which works out to an annualized gain of 22.8%, or nearly 10 percentage points more than the 13.0% gain for the S&P 500!

As incredible as the stock’s performance has been, it ranks only 38th among current members of the index. Among the current group of trillion-dollar stocks, AAPL trails Alphabet (GOOGL), Amazon (AMZN), Broadcom (AVGO), Nvidia (NVDA), and Tesla (TSLA) but is ahead of Microsoft (MSFT), Berkshire Hathaway (BRK/b), and Walmart (WMT). Meta (META) wasn’t even public when Cook took over as CEO, as its IPO wouldn’t be for another eight to nine months in May 2012.

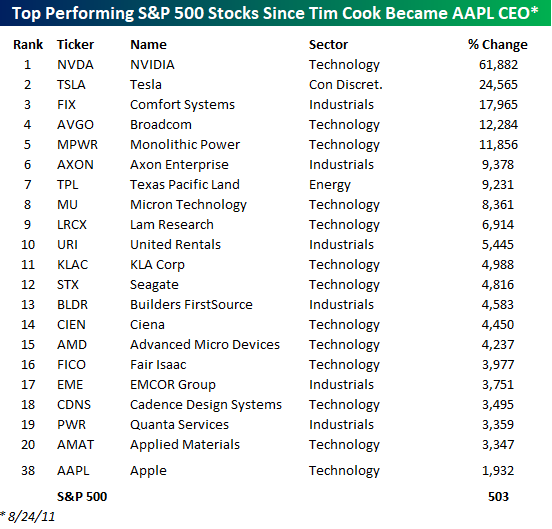

The table below lists the 20 top-performing stocks in the S&P 500 since Cook took the helm at AAPL. NVDA’s 61K% gain is more than double the next closest stock (TSLA) and more than 30 times the gain of AAPL! There are three other stocks – Comfort Systems (FIX), AVGO, and Monolithic Power (MPWR) that have rallied more than 10,000%. While most have become household names, not all have. If you asked the average person to comment on the names listed below, many would probably see names like Comfort Systems (FIX) or Monolithic Power (MPWR) and ask why a mattrass company and utility are on the list, not knowing that the companies provide essential cooling (FIX) and power management systems (MPWR) for the data centers that power AI.

A look at AAPL’s performance under Cook shows what, in retrospect, looks like a steady uptrend with higher highs and higher lows, although there have been plenty of times along the way where the road ahead looked very uncertain. When Cook took the helm, AAPL was trading at a split-adjusted $13 per share. Yesterday, it closed just above $273, off nearly 5% from its all-time high of $286.19.

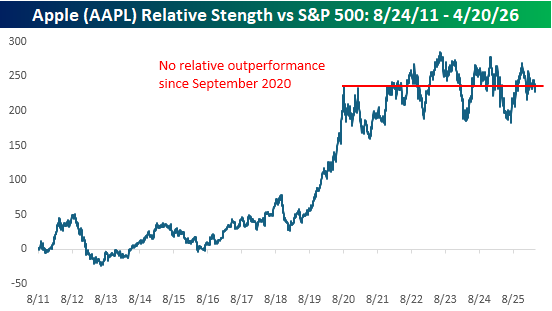

As steady as the rally in AAPL looks, the stock has seen a major shift in at least one respect over the last five years. For more than a decade, from the launch of the iPod through the launch of the iPhone, right up until Covid, AAPL was a steady alpha generator versus the market. A look at its relative strength versus the S&P 500, though, shows a sideways pattern that has been in place for more than five years. Will the new CEO “Ternus” around?

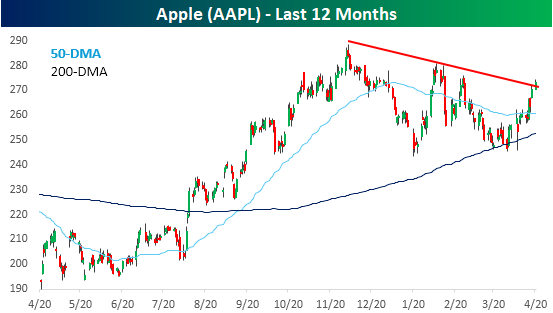

Looking at AAPL’s performance on a short-term basis shows the stock at an important juncture. After trading in a steady downtrend since its high late last year, AAPL tested that downtrend line over the last couple of days and appears to be stalling. While the stock successfully tested its 200-DMA in March and reclaimed its 50-DMA, the next step on the road to new highs and a potential return to outperformance will be a rally above $275.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.