Jan 2, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The only true wisdom is in knowing you know nothing.” – Socrates

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As we approached the turn of the calendar, December was flooded with market outlooks for the year ahead, which always present the reader with highly confident expectations for the year ahead. Reading through most of them, the blueprint for the year ahead looks certain – solid earnings growth, two to three rate cuts, higher but stable inflation, and steady economic growth. It’s almost as though the outcome for 2026 has been pre-ordained. If only life were that simple.

All you had to do was watch last night’s Ole Miss/Georgia game to be reminded that even when everyone thinks they know what’s “going” to happen, it’s not uncommon for the opposite to play out. In the week leading up to last night’s game, prediction markets were giving Ole Miss less than a one in three chance of winning. After the game started, the odds for Ole Miss got worse, falling below 20% for much of the game. When the game finally ended just before midnight, though, it was Ole Miss on top by a score of 39-34. Whether it’s in sports, your personal life, or the markets, just because everyone seems to agree on what’s going to happen doesn’t mean that’s what will play out. Expect surprises.

After the weakness to close out 2025, investors are probably surprised to see futures looking so strong this morning. S&P 500 futures are pointing to a 0.57% gain to start the year, while the Nasdaq is on pace for a 1% gain. The 10-year yield is little changed at 4.15% while crude oil is down fractionally at just above $57 per barrel. After a volatile end to 2025, metals have picked up right where they left off last year, but this time on a positive note. Gold is up over 1%, while silver and platinum are up over 4% each.

In Asia, Japan and China were closed, but other major indices in the region traded on a positive note, with Hong Kong up 2.8% and South Korea jumping 2.3%. The only economic indicator of note in the region was South Korea’s manufacturing PMI, which moved slightly back into expansionary territory at a level of 50.1.

European stocks are also positive this morning, with the STOXX 600 up 0.5%, led higher by Italy and Spain with gains of 0.6% each. The gains come despite generally weaker than expected manufacturing PMI readings for the region, where the Eurozone slid further into contraction, and Germany’s reading fell from 48.2 to 47.0.

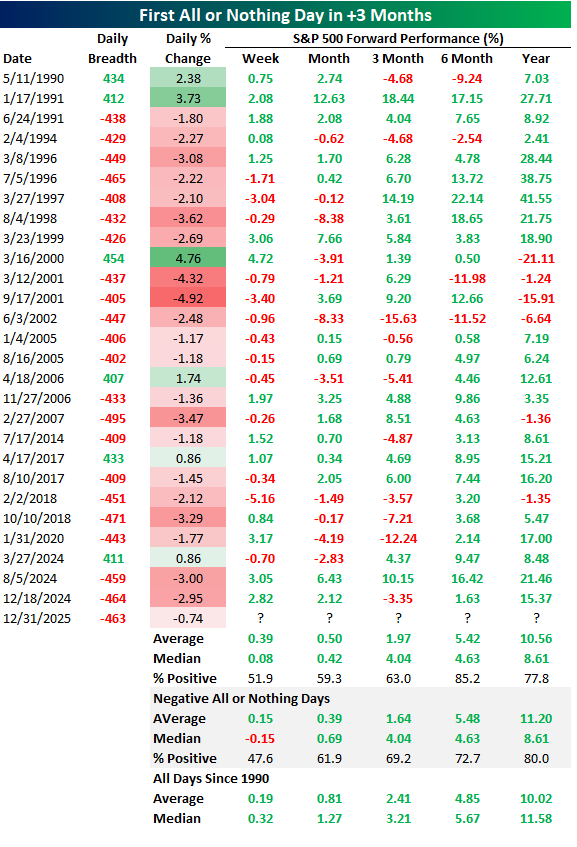

While futures are higher to kick off 2026, 2025 ended like a 500-pound bag of rocks, or more accurately, 482 rocks. The S&P 500 dropped 0.74%, which wasn’t the worst decline considering breadth was exceptionally bad with 482 index members declining versus only 19 rising. We consider an all-or-nothing day when breadth is +/-400, meaning at least 90% of the S&P 500’s constituents rose or fell. Wednesday was the first all-or-nothing day since July 15, when net breadth was -404. As shown in the table below, the first all-or-nothing day in at least three months has typically been followed by gains, but not particularly stronger or weaker than the long-term average. That’s also the case when the first day in at least three months is a ‘nothing’ day like Wednesday was. With that said, in the near term (one week and one month), median returns have been a little bit weaker than all periods after those instances.

Dec 31, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“For eleven months and maybe about twenty days each year, we concentrate upon the shortcomings of others, but for a few days at the turn of the New Year we look at our own. It is a good habit.” – Arthur Hays Sulzberger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We made it (almost) through another year. Regardless of your political leanings, one thing we can all probably agree on is that with Trump as President, there’s never a dull moment. It was true in his first term, and the first year of his second term has proved no different. For all the uncertainty and volatility this year, though, it’s ironic to think that the VIX is closing out 2025 at under 15 and not far from its lows of the year!

Futures are lower this morning, with the S&P 500 indicated to open 0.21% lower while the Nasdaq is down 0.30%. A decline today would make it four straight days of declines to close out the year. Despite the gains for the year, 2025 is going out with a whimper.

Outside of equities, the 10-year US Treasury yield is down 2 bps to 4.1% while crude oil is fractionally higher. While most areas of the financial markets are quiet today, the real action is in metals, where the CME has lifted margin requirements for the second time in a week! Gold is down 1.6%, while silver is down over 8% and platinum is sinking over 10%. Silver is on pace for its fourth straight day of 7.5% daily moves, while platinum has had four straight 5%+ daily moves.

In Asia overnight, the Nikkei was closed, but most other indices in the region finished the last trading day of the year higher as China’s manufacturing PMI moved slightly back into expansionary territory (50.1) and came in higher than expected. In Europe, the tone is less positive this morning as the STOXX 600 trades down 0.2% in a session where many countries are closed for trading, and those that are open will close early. Technology is leading the losses with a decline of 0.6%.

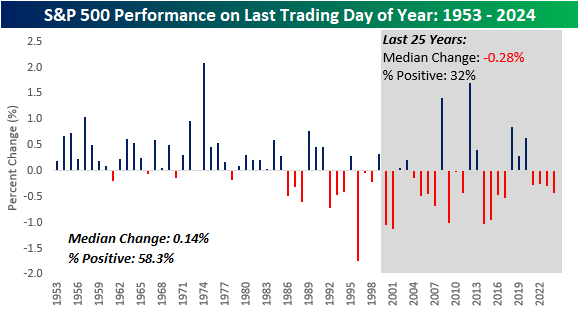

Equities are on pace to close out the last session of the year with losses, and that’s a trend that has become increasingly common in recent years. The chart below shows the S&P 500’s historical performance on the last trading day of the year since 1953. The S&P 500’s median performance has been a gain of 0.14% with positive returns 58.3% of the time.

While the long-term performance has been positive, more recent returns have been weaker. If the S&P 500 finishes lower today, it would be the fifth straight year that the index traded lower on the last session of the year, and that would be the longest streak since at least 1953. Besides just the last four years, though, the pattern of the last trading day of the year has been lower. Since 2000, the S&P 500’s median change on the last trading day of the year has been a decline of 0.28%, with gains less than a third of the time. If there’s any consolation for bulls, in years when the S&P 500 was up over 15% YTD heading into the final session of the year, the median gain on the final day has been a gain of 0.29%, with gains 64% of the time, while in all other years, the median gain was just 0.5%.

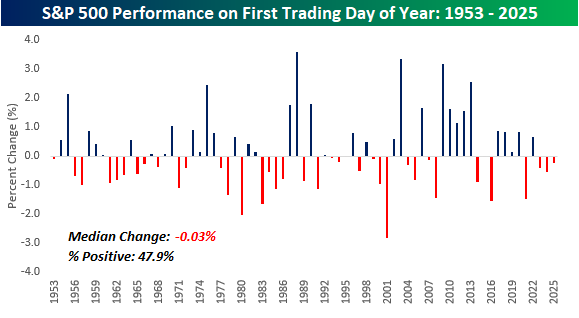

When we turn the calendar to 2026 on Friday, market performance on the first trading day of the year hasn’t been great either. Since 1953, the S&P 500’s median change to start a new year was a decline of 0.3% with gains just under half of the time. The equity market has also traded lower on the first trading day of the year in each of the last three years and four of the last five. Maybe the best idea is to take off until Monday!

Dec 30, 2025

Before getting to this morning’s pre-market analysis, be sure to watch this CNBC segment with Bespoke’s Paul Hickey discussing the market’s set-up heading into 2026.

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I wake up every day and I can’t wait to go to work, and that’s a gift. Not too many people have the opportunity to feel that way.” – Tiger Woods

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

On another likely quiet day for the US markets, futures are lower, but no major index is indicated to open down more than 0.05%, so it wouldn’t take more than a sneeze to flip things around to the positive side. In most other areas of the market, current action is also subdued as treasury yields, crude oil, and crypto assets are all modestly higher. The one area that remains volatile is in the metals markets, as gold is up nearly 2%, while silver is up over 7% and platinum is up over 5%. We saw big negative reversals in these markets yesterday, so if you’re a bull on the sector, you’re breathing a sigh of relief today.

It will be a somewhat busy day for data today as we’ll get the weekly ADP Employment, FHFA House Price Index, and the Chicago PMI for December. The latter report always seems to be negative these days, but expectations are already low at 39.5. In addition to these three reports, we’ll also get the minutes from the December Fed meeting.

In Asia overnight and Europe this morning, it was a tale of two markets as Asia was mostly lower while Europe experienced broad-based gains.

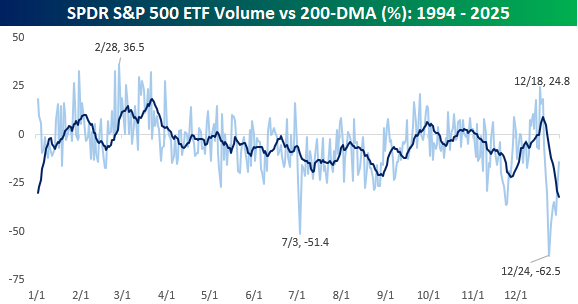

We’re obviously in one of the least volatile periods of the year for stocks, and the chart below illustrates that trend. When it comes to the daily volume in the SPDR S&P 500 ETF (SPY) relative to its 200-DMA, Christmas Eve ranks as the day with the least volume of any day of the year, when the median daily volume has been 62.5% below its 200-DMA. The next closest day in terms of low volume is July 3rd, when the median daily volume has been 51.4% below its 200-DMA. It makes sense that these two days would be quiet, given that they precede holidays, but they’re also both days when the market closes early, so the window for trading is shorter.

What was surprising about this chart is when the high-volume days tend to occur. With September and October being the most volatile months of the year, you would expect to see volume spikes during those months as well. While volume tends to come in above average during the fall, the period of highest volume relative to the 200-DMA occurs in late February and March.

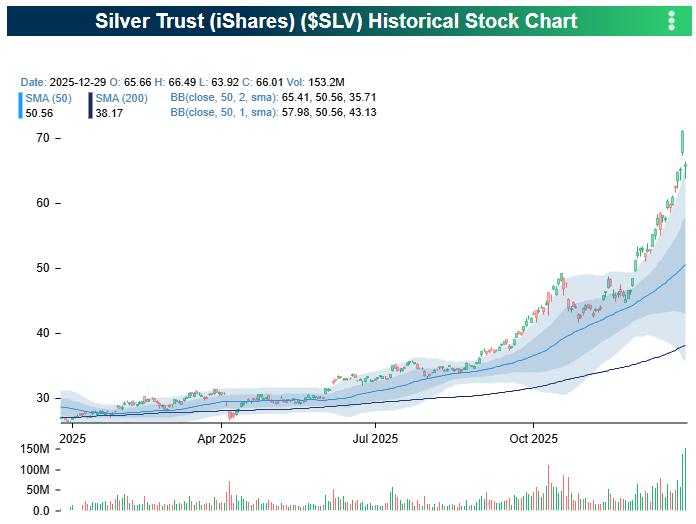

One area of the market where volumes weren’t light yesterday was in the commodities market, and more specifically, Silver. The iShares Silver Trust (SLV) had its highest volume day since February 2021, and after hitting a record high last Friday, plunged over 7%, forming a massive island reversal. As shown in the chart below, the gaps between last Friday’s trading range and the day before (Thursday) and the day after (Monday) were extremely wide, with more than a full percentage point separating the sessions on both sides.

Dec 29, 2025

Before getting to this morning’s pre-market analysis, be sure to watch this CNBC segment with Bespoke’s Paul Hickey discussing the market’s set-up heading into 2026.

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Investors should purchase stocks like they purchase groceries, not like they purchase perfume.” – Benjamin Graham

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

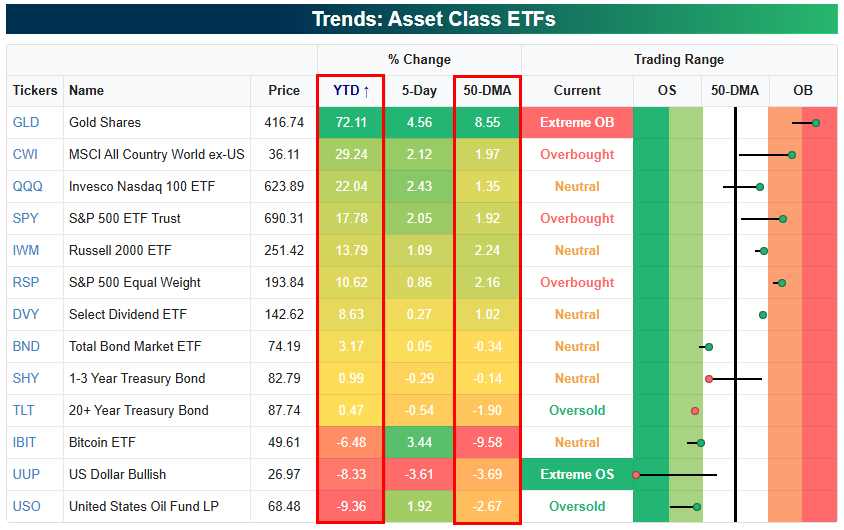

With just three trading days left in the year, below are a number of snapshots from our Trend Analyzer tool highlighting where various asset classes, sectors, and large-cap stocks stand on a year-to-date basis and relative to their 50-DMAs.

Gold (GLD) is now easily the top performing major asset class in 2025 with a 70%+ gain. The next-best is the “rest of world” equity market with the all country ex US ETF (CWI) up 29.2% YTD. The Tech-heavy Nasdaq 100 (QQQ) ranks third with a 22% gain.

There are three key asset classes in the red this year: Bitcoin (IBIT), the dollar (UUP), and oil (USO).

Of the ETFs shown, the dollar (UUP) is the most oversold heading into year end, while gold (GLD) is the most overbought.

Looking at major domestic equity index ETFs, mid-caps have been “mid” in 2025 with only single-digit gains, while large-caps are up closer to 20%. Heading into 2026, every single index ETF shown is above its 50-DMA, with the large majority overbought.

Dec 26, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Destiny is what you are supposed to do in life. Fate is what kicks you in the ass to make you do it.” – Henry Miller

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Good morning and happy Friday, on what is likely to be one of the most uneventful trading days this year. US equity futures are fractionally lower, treasury yields are little changed, and crude oil is slightly higher. The only area of the market with real activity is in gold and other metals. The yellow metal is up “only” 0.75% to $4,537 per ounce, but silver is up close to 4%, while Platinum is up double that, trading at 2,414.40 per ounce. On December 10, platinum closed at $ 1,647.50, and in the 16 days since then, it has rallied by 47%.

While it has been a quiet week for US equities, Asian markets haven’t been sleeping on Christmas. Overnight, the Nikkei rallied 0.7% to take its weekly gain to 2.5% while South Korea gained 0.5% for a total weekly gain of 2.7%. There was some welcome inflation news as Tokyo CPI slowed to 2.0% y/y and 2.3% y/y on a core basis. Despite that news, two-year JGB yields hit the highest level since 1996. In Europe, markets are even quieter than they are here as most countries remain closed for the Christmas holiday.

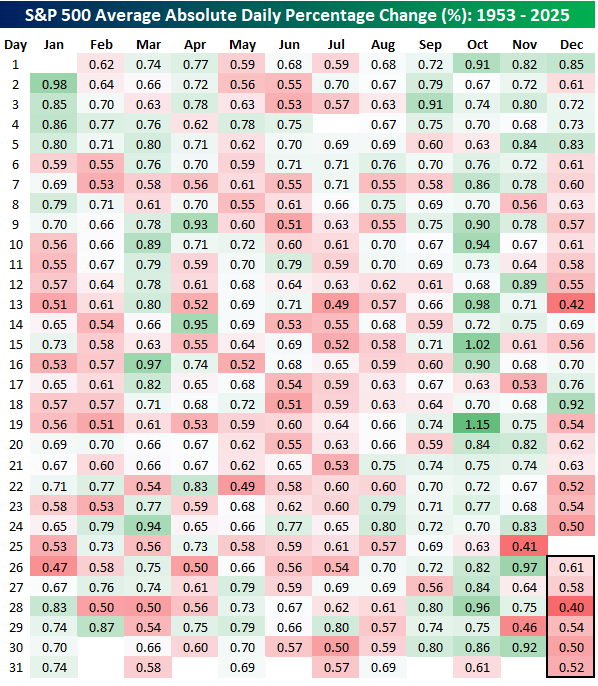

The S&P 500’s average daily move since 1953 has been up or down 0.67%, but that hasn’t been the case in the final week of December or the second half of the month, for that matter. The table below is like the one from our Chart of the Day from Tuesday (12/23), where we looked at the S&P 500’s average and median daily change for every day of the year. In this one, we show the S&P 500’s average daily percentage move (up or down) for every day of the year since 1953.

Volatility on the day after Christmas has been below average with an average daily move of 0.61%, but it still tends to be the most volatile day of the year between Christmas and year-end. The least volatile day of the week and the year, for that matter, is December 28th (0.40%). 12/28 falls on Sunday this year, but volatility on every day of the post-Christmas period is below the overall average. For December, volatility has been below average on 73% of all trading days, and the only month with more below average volatility days is July (80%). Conversely, October has the highest percentage of above average volatility days (87%).

The chart below shows the average absolute daily change for every day of the year (gray line) along with the 10-day moving average. We’re entering the final days of the year, and volatility is very low, but December 31st marks the low point of the year. From there, it will start to rise in the first few days of the new year. For much of the year, though, volatility tends to stick close to the average. The only real exceptions besides late December are mid-July, when volatility is also subdued, and then mid-March and October, when volatility starts to heat up. For now, though, it’s just cold!

Dec 24, 2025

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“One of the most glorious messes in the world is the mess created in the living room on Christmas day. Don’t clean it up too quickly.” – Andy Rooney

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Ahead of a holiday-shortened session (equities close for trading at 1 PM Eastern), US equities are in the Christmas mood this morning as futures are flashing shades of red and green. With the magnitude of the gains and losses being so small (less than 5 bps), futures on some of the indices are even alternating between red and green. Volume is very light, and while we could probably find a ‘reason’ for the modest moves up or down, besides jobless claims at 8:30, there’s nothing really going on.

The same can also be said for other areas of the financial markets, as the ten-year yield is down less than a basis point, crude oil is up fractionally, and bitcoin is down less than half of one percent. The only area of any movement this morning is in the metals space. While gold is up fractionally (but still above $4,500 per ounce), platinum, silver, and copper are all up at least 1.5%. If you own any of these metals, Merry Christmas indeed.

In Asia overnight, equity markets were mixed. The Nikkei traded down 0.1%, but China managed to trade 0.5% higher. In Europe, it’s very quiet this morning. Germany and Italy are already closed for Christmas, and the STOXX 600 is basically flat.

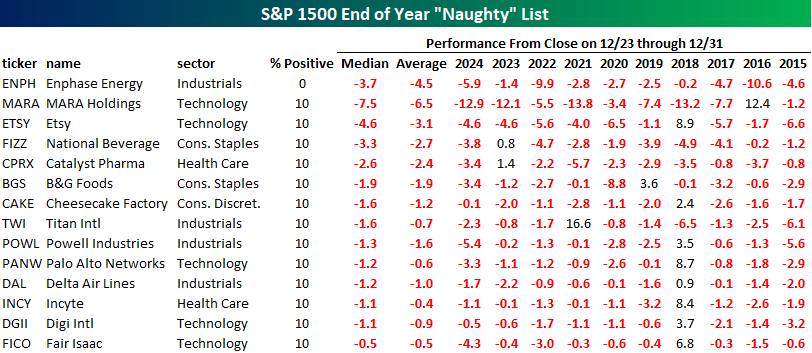

There’s been a lot of gains across financial markets this year, and for US stocks, equities typically also finish the year off with a positive bias. Not all stocks make the nice list, though. The table below shows the 14 stocks in the S&P 1500 that have historically traded lower from now through year-end over the last ten years, with declines at least 90% of the time.

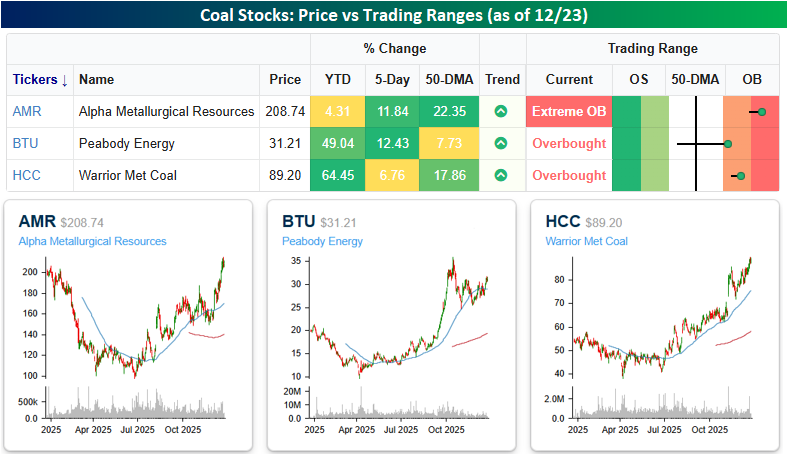

At the top of the list, Enphase Energy (ENPH) has traded lower during this period for each of the last ten years, with a median decline of 3.7%. The remaining thirteen stocks on the list have traded down during this period in nine of the last ten years, and the worst performer of them all is bitcoin miner MARA Holdings (MARA). The stock’s median decline during this period has been 7.5%, including double-digit declines in each of the last two years. Other notable stocks on the list include Palo Alto Networks (PANW) and Delta Air Lines (DAL). All fourteen of these stocks can expect some coal in their stockings tomorrow morning.

Getting coal in your stocking this year may not be the worst gift to get. Looking at the performance of the three major coal stocks this year, two are up at least 49%, while the biggest laggard – Alpha Metallurgical (AMR) is up over 10% in the last week and trading more than 22% above its 50-DMA. All three stocks are up at least 5% in the last week, suggesting that someone has been buying a lot of coal this week. Could it be Santa? Let’s hope not!

For all those who celebrate it, Merry Christmas, and for those who don’t, enjoy the day off!