Feb 24, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a review of the latest Fedspeak in addition to all the further pain in software names (pages 1 – 3). Next up, we show where some outperformers were today in addition to an update on regional Fed indices (page 4). After that, we provide a review of the latest positioning data (pages 5 & 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 24, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Domino’s Pizza’s (DPZ) Q4 2025 earnings call.

Domino’s Pizza (DPZ) is the world’s largest pizza company by retail sales, operating over 21,000 stores globally through a franchise-heavy model with roughly 7,186 US locations. As the dominant player in quick-serve (QSR) pizza with approximately 25% US market share, the company offers insight into consumer spending patterns across income cohorts, the evolving economics of delivery versus carryout, and the competitive dynamics of value-driven restaurant businesses. Management guided to 3% US same-store sales growth in 2026 against what they expect will remain a pressured macro backdrop. CEO Weiner introduced the ambition of doubling US retail sales from roughly $10 billion over time, benchmarking against QSR category leaders with 40-50% share. Pricing was flat in Q4, yet estimated franchisee store profitability grew to approximately $166,000, management’s “profit power” thesis in action. The company grew all income cohorts in 2025, pushing back on the lower-income consumer weakness narrative prevalent across QSR. On aggregators, management stressed they haven’t reached fair share on Uber or DoorDash and are growing those platforms carefully to ensure new orders are genuinely additional rather than cannibalizing their own direct channels. DPZ reported better-than-expected revenue on weaker EPS, as the stock climbed 4.1% on 2/23…

Continue reading our Conference Call Recap for DPZ by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Feb 24, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Home Depot’s (HD) Q4 2025 earnings call.

Home Depot (HD) is the world’s largest home improvement retailer, operating 2,359 stores across the US, Canada, and Mexico, with $164.7 billion in fiscal 2025 sales. The company serves both Do-It-Yourself consumers and professional contractors, and its recent acquisitions of specialty distributors SRS and GMS have expanded its reach into roofing, building materials, and the professional trades. Management described a year of stable but subdued demand, with full-year comps up just 0.3% as housing turnover remains near 30-to-40-year lows and large discretionary projects stay pressured. CEO Ted Decker called big-ticket discretionary recovery the “telltale” for a market turn, one they have not yet seen. On tariffs, the team said pricing actions on mid-single-digit exposure are largely complete, translating to roughly 3% SKU-level price increases. SRS gained roofing market share despite industry shingle shipments falling 28% in Q4 to their lowest level since 2019, though aggressive pricing will weigh on Q1 margins. Fiscal 2026 guidance calls for flat-to-2% comps, with EPS growth of flat-to-4%. On better-than-expected results, HD shares opened 3.3% higher on 2/24…

Continue reading our Conference Call Recap for HD by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Feb 24, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t know what happened. It was just euphoria. I can’t even explain what I was feeling, just pure joy.” – Charlie McAvoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After trading uniformly higher earlier, equity futures are mixed this morning, with the S&P 500 fractionally lower, while the Nasdaq is higher. Investors are still reeling from yesterday’s tech sell-off, as markets start to think that AI-disruption will negatively impact just about every business and sector. Treasury yields are little changed, but at 4.03%, the 10-year yield is near the low end of its range. Crude oil is modestly higher but still hovering around $66 per barrel, while gold is down over 1% and Bitcoin is down another 2% and barely hanging on to $63,000.

In Asia, Japan, South Korea, and China were all firmly higher as the latter returned from the Lunar New Year holiday, while India and Hong Kong were both down over 1%. In Europe, trading has been directionless in early trading with the STOXX up 0.2%, but at the country level, performance has varied between gains and losses.

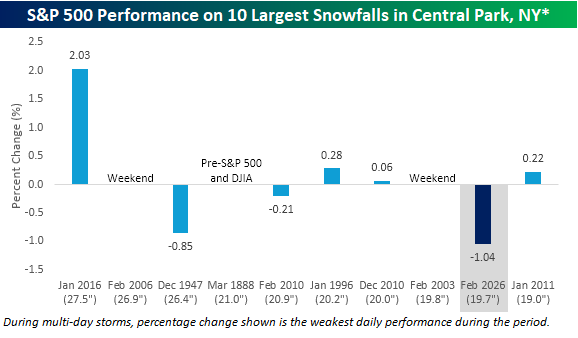

Let’s start with yesterday’s blizzard in the Northeast. With 19.7 inches of snow in New York’s Central Park, it was the ninth-largest snowfall in New York City history. While travel bans were in place around the New York tri-state area, the bears had no trouble getting to work. With the S&P 500 down 1.04%, it was the worst single-day performance for the S&P 500 during one of its ten-largest snowstorms on record. As shown in the chart below, during the prior top ten snowstorms for New York City, the weakest single-day performance during one of these snowstorms was a decline of 0.85% on 12/26/1947.

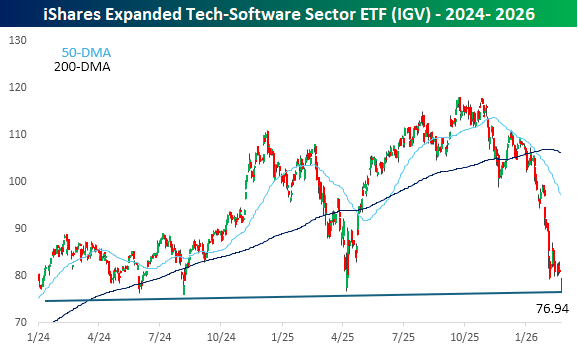

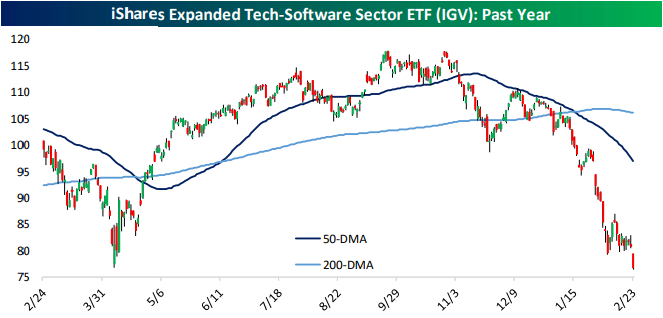

As it has been for some time, the software sector was responsible for much of yesterday’s weakness. The iShares Expanded Tech-Software Sector ETF (IGV) fell close to 5% and to its lowest level on an intraday basis since August 2024 as the lows from earlier this month broke like a hot knife through butter.

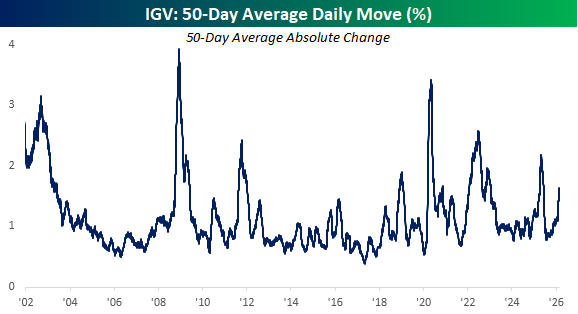

While software has been weak, it hasn’t necessarily been as volatile as you would expect. Over the last 50 trading days, IGV’s average daily change has been a gain or loss of 1.6%. While that’s elevated, it’s hardly anywhere near a historical extreme. Even in early 2025, the average daily change was much higher at over 2%.

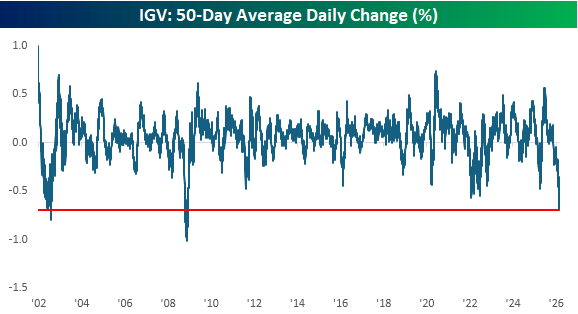

Where the moves in IGV have been extreme, though, is in terms of the average daily percentage change (not the absolute daily change but the average of the trailing 50-day changes). As of yesterday’s close, IGV’s average daily change was a decline of 0.69%, which ranks as one of the most negative readings in the ETF’s history. In fact, the only times that IGV was more of a one-way trade to the downside were during the Financial Crisis and at the end of the dot-com bust.

Feb 23, 2026

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a review of the latest Fedspeak in addition to all the further pain in software names (pages 1 – 3). Next up, we show where some outperformers were today in addition to an update on regional Fed indices (page 4). After that, we provide a review of the latest positioning data (pages 5 & 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Feb 23, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t know what happened. It was just euphoria. I can’t even explain what I was feeling, just pure joy.” – Charlie McAvoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Confusion regarding the state of global trade following Friday’s Supreme Court decision striking down the President’s reciprocal tariffs has futures lower to kick off the week. The fact that some form of armed conflict with Iran looks increasingly likely also hasn’t helped. As if that weren’t enough, while the blizzard in the northeast doesn’t have any direct market impact right now, it has effectively paralyzed a central area of economic activity for the day, and air traffic, so it will have some economic impact as well. Crude oil is fractionally higher at close to $67 per barrel; gold is up 2% and looks to be making a new run at its January highs; and silver is up over 5%. Bitcoin, however, is down 2% as some investors are starting to question whether it’s even an effective store of value anymore.

Overnight in Asia, China remains closed for the Lunar New Year, and Japan is also closed, but South Korean stocks traded up nearly 1%, which nowadays doesn’t even register as an impressive move. In Europe, the STOXX 600 is down modestly in a mixed session where Italy and Spain are both up roughly 1% while Germany dips about 0.5%. The disparate performances stem from strength in banks and weakness in industrials (more German-focused).

Datawise, there’s not a lot on the calendar today. At 8:30, we got the Chicago Fed National Activity Index. That will be followed by Factory Orders at 10, and the Dallas Fed at 10:30. Fed Governor Waller is also speaking this morning, and he’s on the wires saying that a March rate cut will depend on the state of the labor market, which he sees as likely remaining weak going forward, citing potential pressures from AI.

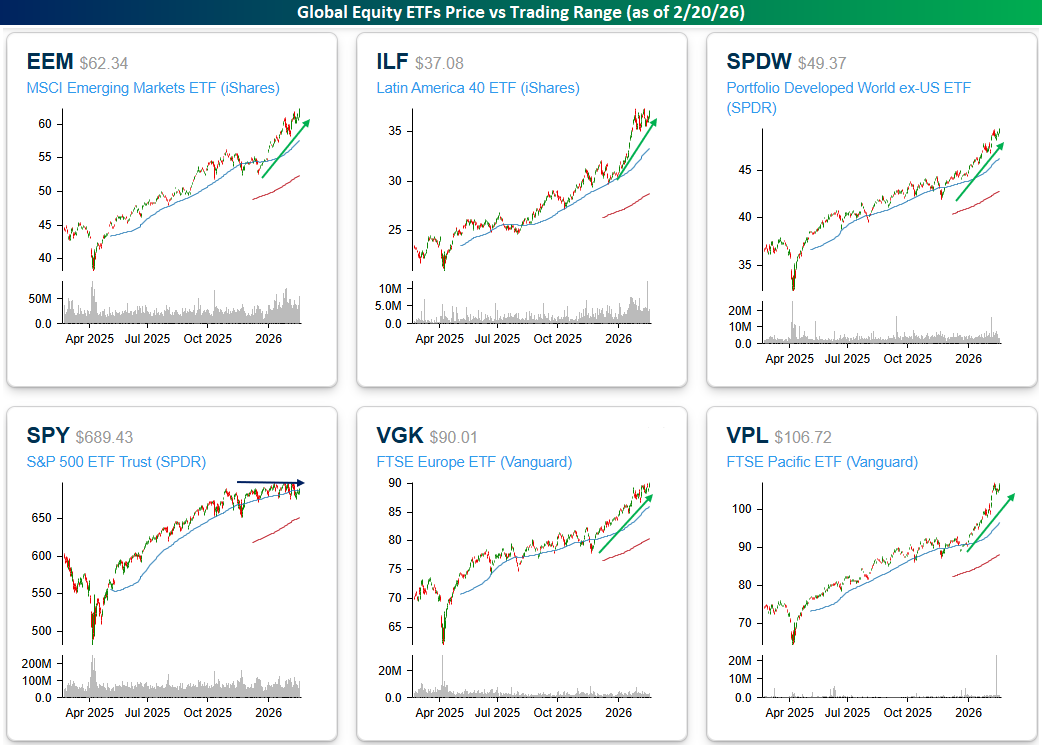

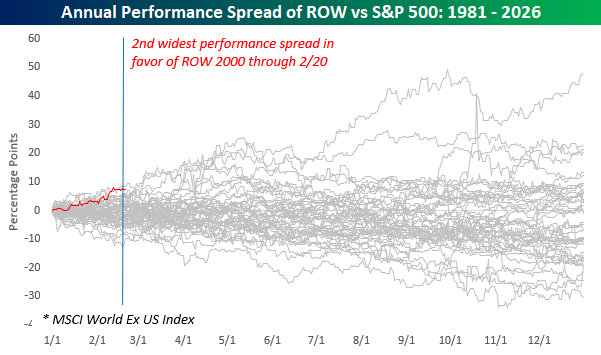

The US is on top of the hockey world this morning after Sunday’s dramatic OT win, and investors are hoping some of those gold-medal vibes rub off on the stock market. As we highlighted in Friday’s Bespoke Report, through the first several weeks of 2026, US stocks have underperformed stocks from the rest of the world to a near-historic degree. As shown in the chart below, the only year since 1980 when the S&P 500 underperformed the rest of the world by a wider margin was in 1984, and barely at that.

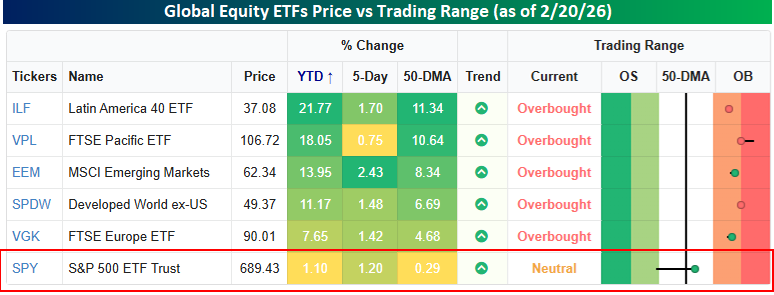

The graphic below puts the short-term US underperformance into even better perspective. Major international regional equity ETFs headed into the weekend on power plays at overbought levels (1+ standard deviation above their 50-DMAs), while the US was short-handed in penalty-killing mode and scrapping to get back above its 50-day moving average. YTD, European equities, as measured by the FTSE Europe ETF (VGK) were outperforming the S&P 500 by more than six full percentage points, but the other four regional ETFs shown were all outperforming by at least 10 full percentage points, with Latin America (ILF) outperforming by 20 percentage points – in less than two months! How the lines have shifted!

A look at the six price charts also shows the disparity between US and international stocks. Five of the charts shown are in clear, well-defined uptrends, while the US has been stuck in neutral between the blue lines, unable to push the puck into the zone, but also successfully fighting off any bearish attacks into their defensive zone.