May 19, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future starts today, not tomorrow.” – Pope John Paul II

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures have been losing steam as we approach the opening bell, with the biggest recent winners leading the losses. S&P 500 futures are indicated to open nearly 0.5% lower, while the Nasdaq is poised to gap down 0.75%. Treasuries aren’t doing much this morning as the 10-year yield is modestly lower but still above 4.6%. Crude oil is little changed but elevated as the Middle East is on edge over whether the US will launch a new round of attacks on Iran. Gold and Bitcoin are both fractionally lower.

In Asia, it was a mixed session with the Nikkei down 0.5% following a modestly stronger than expected GDP report, while China was up nearly 1%. With AI-related stocks coming under pressure yesterday, South Korea fell 3.3%.

With tech and AI-related stocks leading the selling pressure, European stocks are much more immune, and the STOXX 600 is bucking the trend of weakness with a gain of 0.8%. Germany is leading the way higher with a gain of 1.4%, while Italy lags with just a marginal gain.

In the US today, it’s a quiet day for data with Pending Home Sales at 10 AM. On a housing-related note, though, shares of Home Depot (HD) are trading marginally lower after reporting earnings this morning. Management noted that while the consumer continues to “defer their spending on larger projects…consistent with what they’ve told us the last few years,” they remain engaged.

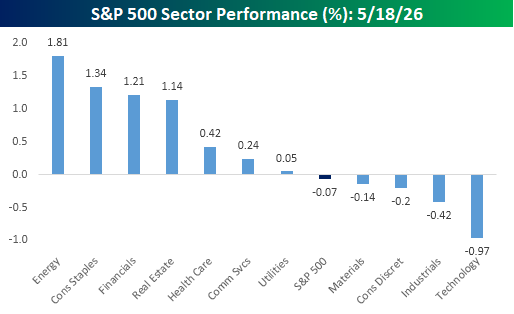

Divergent market breadth usually gets the most attention when the S&P 500 trades higher, but the net number of stocks trading higher on the day is negative. Yesterday was the opposite, where the S&P 500 traded lower, but most stocks in the index finished the day higher. At the sector level, yesterday was also net positive as seven sectors traded higher while just four traded lower. With Technology being one of those sectors that traded lower, though, it dragged the entire market into the red with it.

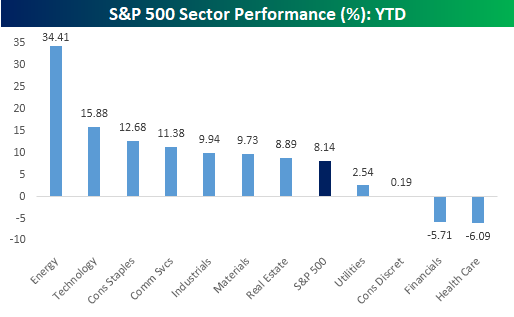

For all the talk recently about how narrow breadth has been, the YTD picture of sector performance is also surprisingly positive. While the S&P 500 is 8.1% higher YTD, seven sectors have outperformed the index on a YTD basis, while just four have declined.

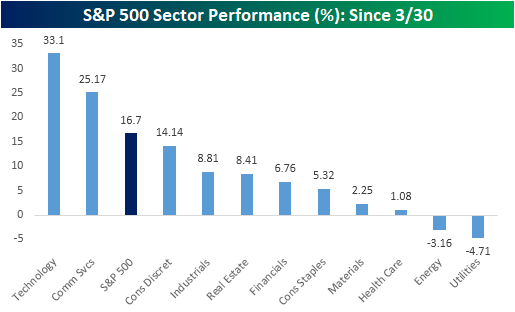

Where the big breadth divergence has occurred is since the low on 3/30. In the seven weeks since then, the S&P 500 is up 16.7%, but just two sectors – Technology and Communication Services – have outperformed. What really stands out is how many sectors have outperformed the S&P 500 by A LOT since 3/30. As shown in the chart, besides Technology and Communication Services, the only other sector that is even close to performing in line with the index is Consumer Discretionary.

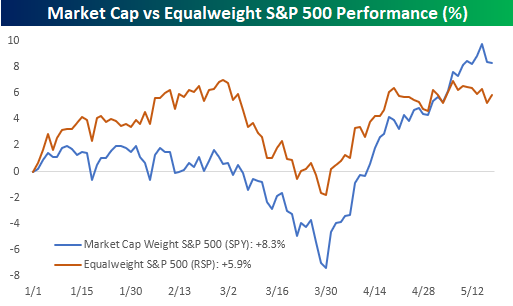

Comparing the performance of the market cap and equalweight S&P 500 so far this year, while the market cap-weighted S&P 500 has outperformed, it’s not as though the divergence has been all that wide. While there have been times throughout the year when one version has significantly outperformed the other, in the bigger picture, they have largely cancelled each other out.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 18, 2026

Log-in here if you’re a member with access to the Closer.

- Agricultural commodities have begun to breakout after a long term triple bottom.

- Urea prices have begun to fade as phosphate prices have begun to inflect higher.

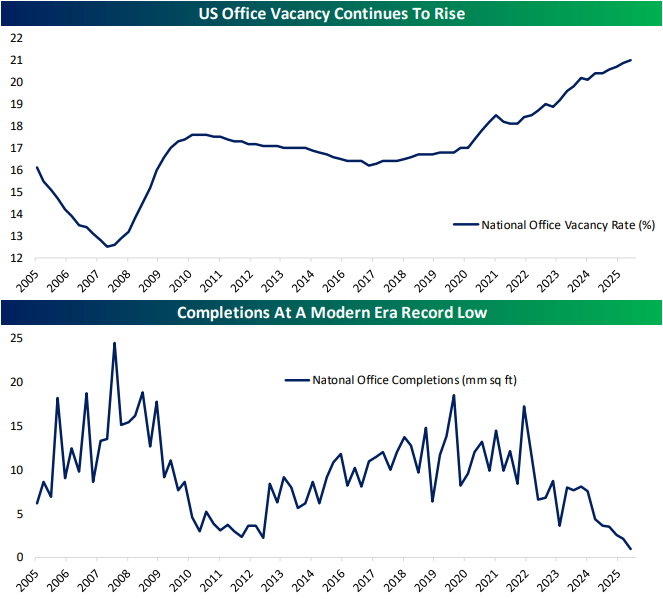

- US office vacancy rates hit a new record high of 21% in Q1 while office completions have fallen to a record low

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

May 18, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future starts today, not tomorrow.” – Pope John Paul II

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last week’s Trump-Xi summit, which failed to produce any meaningful results, coupled with data suggesting inflationary pressures in the economy, has left stocks facing an uphill battle. That pressure has continued into the new week. S&P 500 futures were firmly lower but have rebounded on reports from Iran that the US will offer a temporary waiver on Iranian oil sanctions. Both the S&P 500 and Nasdaq were indicated to gap down by about 0.5% at the open, but are now just modestly negative, while the 10-year yield is fractionally lower. Crude oil prices are modestly higher, and gold and Bitcoin are lower, with the latter trading back down below 77K.

In Asia, it was a mixed session with Japan and Hong Kong both down 1% while South Korea had a fractional gain of 0.3%. Economic data in China disappointed with April Retail Sales rising just 0.2% while Industrial Production missed forecasts by close to two full percentage points (4.1% vs 6.0%).

In Europe, the STOXX 600 is down 0.4% with Italy down close to 2% after reporting a smaller-than-expected March trade surplus. The UK is trading 0.3% higher as reports suggest PM Starmer is planning to step down.

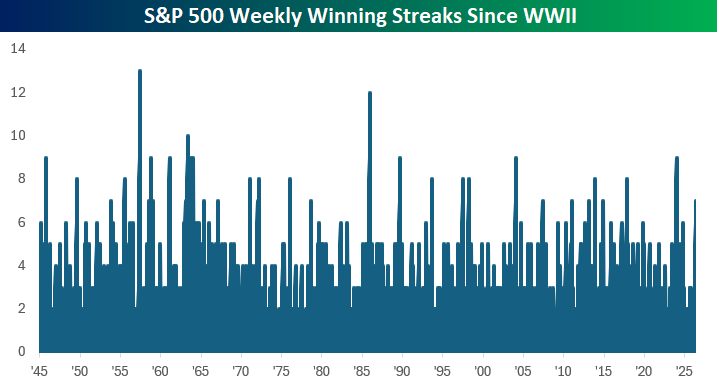

Last week ended on a down note with the S&P 500 declining through the last two hours of the trading session to finish down near the lows of the day. It was a close call at the end of the day on Friday, but the S&P 500 managed to clock its seventh straight week of gains. That’s the longest winning streak since a 9-week streak of gains in December 2023 and the 34th streak of at least seven weeks since WWII.

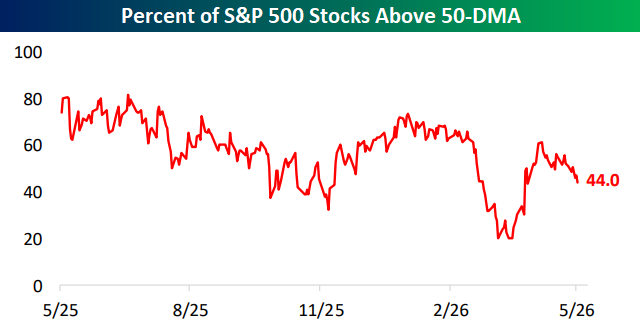

While the S&P 500 may have finished last week higher, breadth remains weak. As of Friday’s close, just 44% of stocks in the S&P 500 were trading above their 50-day moving average, which is hardly the type of reading you would expect to see with a market right near record highs. After a sharp rebound off the April lows, the percentage of stocks above their 50-DMA has been steadily declining for a few weeks now, even as the index has continued higher.

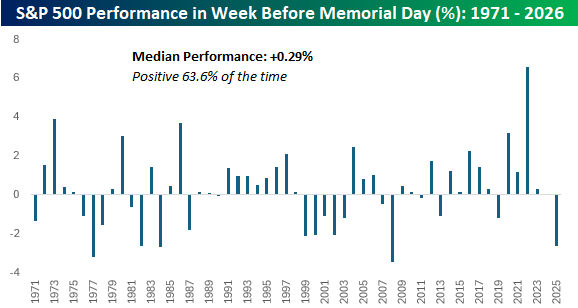

It doesn’t officially start for another month, but the unofficial start to summer kicks off this weekend, just after the unofficial end to earnings season on Thursday, when Walmart (WMT) reports. In the week leading up to the summer season, stocks have tended to have a modestly positive return. Since 1971, when the last Monday of May became the official observance of Memorial Day, the S&P 500’s median performance during the week was a gain of 0.29% with positive returns just under two-thirds of the time. That said, last year’s decline of 2.6% leading up to Memorial Day weekend was the worst pre-holiday performance for the S&P 500 since 2007, and the fifth worst since 1971. Who wants a hot dog with their burger!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 15, 2026

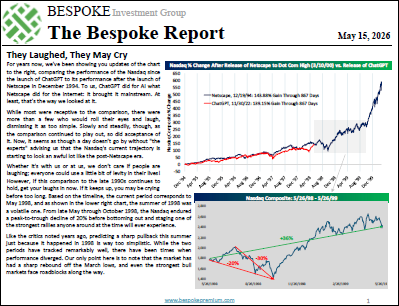

The S&P has continued to leg higher in a picture-perfect breakout that now looks less like a “V” and more like a checkmark.

The market continues to follow the post-Netscape pattern, and more and more investors are starting to embrace the comparison. Is now the wrong time to be rooting for that comparison?

We cover everything going on across markets and the economy in this week’s Bespoke Report newsletter.

To read this week’s newsletter and gain access to the rest of Bespoke’s daily research, start a 30-day trial to one of our three unique membership levels. CLICK HERE to sign up today!

May 15, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I always like to look on the optimistic side of life, but I am realistic enough to know that life is a complex matter.” – Walt Disney

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It may be Friday, but investors are in no mood to celebrate as equity futures are sharply lower. The Nasdaq is leading the losses, declining 1.28% while the S&P 500 is poised to open down by just under 1% (-0.90%). Treasury yields continue to march higher as they have all week, and in the commodity space, WTI crude oil is spiking 3% to just under $104 per barrel while gold is down over 2.5%. Bitcoin is also lower, falling by just 1%.

The weakness in US futures follows a lousy night in Asia. The Nikkei fell 2%, China was down over 1%, and South Korea plunged over 6%. Following these declines, all of Asia’s major indices finished the week lower. Higher yields contributed to the negative tone, and in South Korea, a potential labor strike at Samsung pressured that stock.

Weakness in Asia worked its way into Europe, and stocks are likewise lower across the board with declines of more than 1%. Here again, the primary culprit is higher yields, although CPI in Italy rose less than expected.

Getting back to the US, there’s not much in the way of earnings reports this morning, but at 8:30, we’ll get the release of the May Empire Manufacturing report, followed by Industrial Production and Capacity Utilization at 9:15.

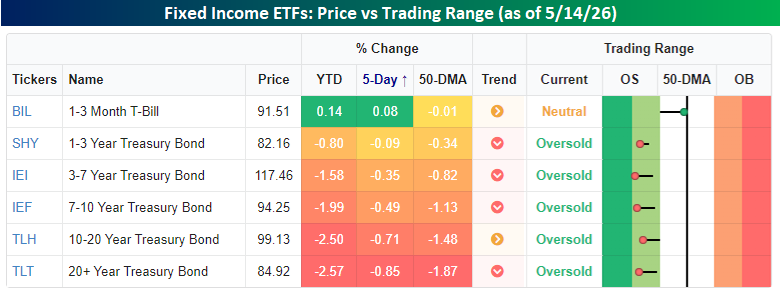

With inflation headlining the week’s economic data, and much of it surprising to the upside, yields have been an unavoidable and uncomfortable focus for investors. Almost across the entire yield curve, we’ve seen yields move higher this week, pushing the prices of the underlying bonds lower.

The snapshot of Treasury ETFs across the yield curve shows the story. Except for the shortest duration treasuries, prices have moved lower over the last five trading days (since last Thursday’s close), and the magnitude of the declines increases the further you go out on the curve. The magnitude of the declines hasn’t been extreme, but any treasury ETF with a duration of more than a year is currently oversold and will only get more oversold at the open today. YTD, it’s also been a year to forget, with declines nearly across the board.

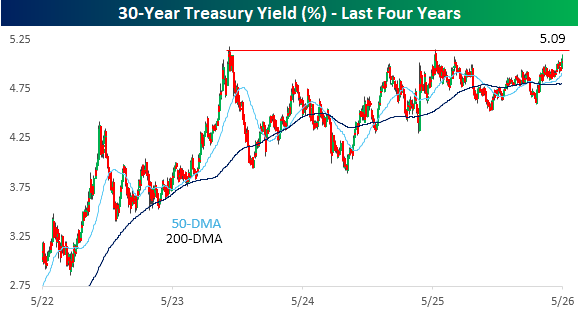

Of all the points on the yield curve, the 30-year is probably at the biggest crossroads. For nearly three years now, right above 5% has been a level the 30-year has flirted with multiple times, but each time it got there, the sellers didn’t have the firepower for a meaningful breakout. This week has been the third major test of that level as the yield pushes up towards 5.10% this morning. Will the third time be the charm or a strikeout?

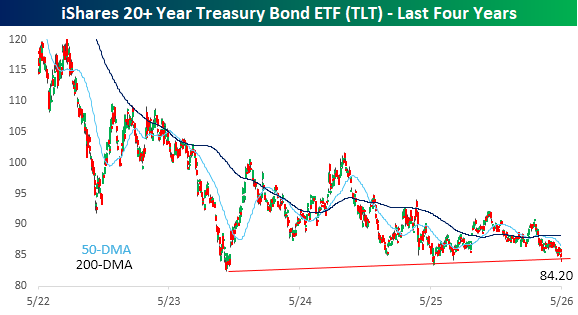

The iShares 20+ Year Treasury ETF (TLT) is the opposite of the 30-year yield. Prices plunged during 2022 and into early 2023 as the Fed hiked rates and inflation surged. As price pressures eased, yields and treasury prices stabilized, and while there was a rally off the 2023 lows into mid-2024, momentum quickly stalled out. Ever since then, prices have been stuck in the mid-80s, and this morning, TLT is trading down over 1% and testing support right around $84. It’s been a multi-year bear market for fixed income in the post-COVID era, and if these support levels don’t hold, the sector could be in store for a new leg lower.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 14, 2026

Log-in here if you’re a member with access to the Closer.

- The rebound in AI Doom stocks has broken over the past week while proxies for OpenAI have ripped higher.

- The past month has seen a historic consistency of new highs despite breadth hardly notching any new highs.

- Both import and export prices rose significantly more than expected in April data.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!