Mar 9, 2026

Log-in here if you’re a member with access to the Closer.

- Markets continue to try to make sense of the Iran situation, making for a historic reversal today for crude prices.

- High volatility has showed that it works both ways with both crude and equities rebounding from sizable losses.

- Preliminary EPA estimates showed that nearly a third of consumer vehicles sold were EVs, hybrids, or fuel cell last year.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 9, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no instance of a nation benefitting from prolonged warfare.” – Sun Tzu, The Art of War

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If there’s ever a day that feels like a Monday, today is it. As much as we may like daylight savings time for the later sunsets, we could do without the later sunrises after already missing an hour of sleep. Couple that with triple-digit oil prices and much lower equity prices, and we almost wish our alarms didn’t go off this morning.

Equity futures are down over 1% across the board this morning, treasury yields are higher with the 10-year yield now up to 4.17% (it was below 4% less than two weeks ago), and WTI crude oil is up over 10% to $102 per barrel. Incredibly, that’s down around 15% from just under $120 overnight. There’s been no flight to safety in gold either, as prices are down over 1% there too.

Equities in Asia plunged overnight, with the Nikkei down over 5%, while South Korea fell 6.0% after circuit breakers were triggered during the session. In China, CPI for February rose much more than expected, rising 1% after an increase of 0.2% in January. And that was before the spike in oil prices. European equities are also down more than the US. The STOXX 600 is down 1.6% with France down over 2% and Spain down just under 2%. We can try to read into different catalysts for the weakness, but it’s pretty much all oil. Until those prices stop rising, equity prices will continue falling.

The economic calendar is quiet today, and there will be no Fedspeak as the blackout period ahead of next week’s meeting started this weekend. The economic calendar will be very busy, though, with CPI on Wednesday, Jobless Claims, Housing Starts, and Building Permits on Thursday, and Personal Income and Spending, as well as GDP, among others, on Friday.

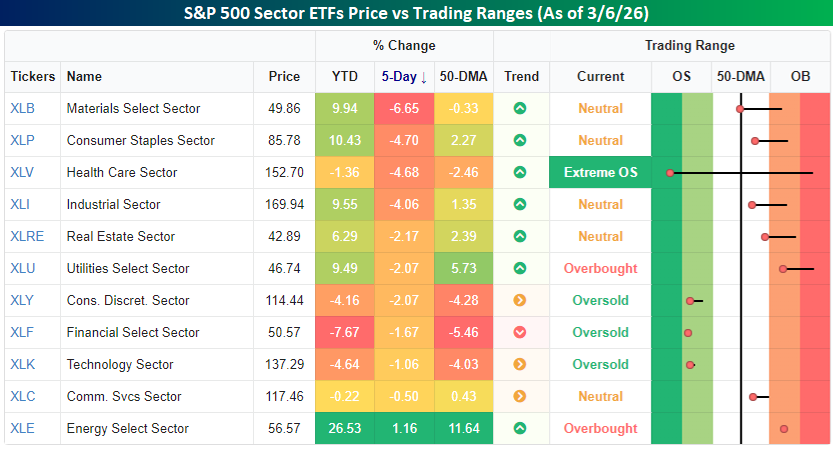

The war in Iran hasn’t had much of a benefit on any sector, except, of course, Energy. Since the fighting broke out just over a week ago, Energy has rallied over 1% while every other sector is in the red, with nine down more than 1%. Four sectors declined by over 4%, with Materials leading the losses at 6.65%, followed by Consumer Staples, Health Care, and Industrials. Health Care’s losses have taken that sector into ‘extreme’ oversold territory after trading in ‘extreme’ overbought territory just over a week ago. War has a way of changing market conditions very quickly!

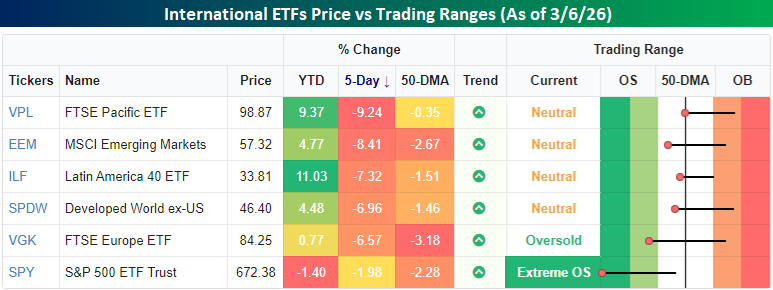

As bad as the US markets have been since the war broke out, it’s peanuts compared to the losses in the rest of the world. Below, we show the performance of various regional ETFs last week. While the S&P 500 was down nearly 2% last week, every other region of the world was down at least 6% and, in most cases, even more. Europe was down 6.6%, emerging markets were down over 8%, and stocks in the Asia Pacific region were down over 9%. As much as higher oil prices are a pain for US consumers and businesses outside of the Energy sector, other areas of the world are much more dependent on external sources for energy than the US.

In terms of the US vs. the rest of the world trade, the Developed World Ex US ETF was down nearly 7%, or five percentage points more than the S&P 500, in a week! As much as the US outperformed the rest of the world last week, it’s still significantly underperforming the rest of the world on a YTD basis (-1.4% vs +4.5%).

With the S&P 500 on pace to gap down 1% at the open for the fourth time in six days today, volatility has been on the rise, and the VIX is trading above 30 for the first time since last spring during the tariff-tantrum. Back then, though, the VIX briefly breached 60 before pulling back. So far during the current war, the highest the VIX has traded is 35.3. Last week may seem like a rough period for the markets, but relative to other points in just the last year, it could be a lot worse. The longer this conflict lasts and oil supplies remain disrupted, the more likely it is that conditions will worsen.

Mar 6, 2026

This Week’s Bespoke Report: Oil’s Record Week, Software’s Comeback, and the Iran Fallout

It was one of the wildest weeks in recent market history. Here’s a look at what we’re covering in this week’s Bespoke Report.

Oil Just Had Its Biggest Week Ever

Crude oil surged 36% this week, the largest weekly gain since at least 1985, after US/Israeli strikes on Iran effectively shut down tanker traffic through the Strait of Hormuz. By Friday afternoon, oil was trading above $91/barrel at its most overbought level in history. In the report, we look at what has historically happened to both oil and equities after spikes like this, and how quickly the pain is likely to show up at the gas pump.

Software Bounces Back

After falling more than 22% in the first two months of 2026, the iShares Expanded Tech-Software ETF (IGV) has rallied nearly 14% in just nine trading days with remarkably steady intraday buying pressure. The Citrini essay that terrified the sector on 2/22 may have marked the clearing-out event. It’s always easier to see in hindsight, but underneath all the snow on 2/23, there was plenty of blood on the software streets. We chart the bounce and put the current streak in historical context.

A Historic Reversal in Positioning

The Iran conflict triggered what looks like a broad deleveraging across institutional portfolios. Everything that worked in January and February stopped working this week, and everything that didn’t work started working. International equities that had been trouncing the US for months got hit the hardest, while the most beaten-down US stocks rallied sharply. We break down the reversal by asset class, country, and individual stock, and we explain why the US held up better than the rest of the world.

The Three-Headed Monster Awakens

Oil, Treasury yields, and the dollar. Our “three-headed monster” indicator just surged to its highest combined level in nearly a year. Two weeks ago, the monster was still asleep. We show where current readings sit relative to 40 years of history and what it has meant for forward equity returns.

Payrolls Go Negative

Friday’s jobs report showed a loss of 92,000 nonfarm payrolls, badly missing the +55K estimate. But the headline number is misleading. A big chunk of the weakness came from a single line item that will almost certainly reverse. We walk through what’s really going on beneath the surface, including what the data says about AI’s impact on younger workers.

The S&P 500 Keeps Bouncing

The S&P 500 opened down 1% or more on three separate days this week and managed to claw back each time. That’s only happened 13 times in SPY’s history since 1993. We look at where those prior weeks fell on the chart and what happened next.

That’s just a recap of some of the topics covered in this week’s Bespoke Report, our flagship weekly newsletter. This week’s edition is 29 pages of charts, tables, and in-depth analysis. If you’d like to dive in further, you can start a Bespoke trial to read the full report and get access to all of our daily research.

Mar 6, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I never worry about the problem. I worry about the solution.” – Shaquille O’Neal

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Did you know that there’s an employment report today? With geo-politics in the forefront, economic data has largely taken a back seat this week, but the data will keep coming (unless there’s a shutdown, of course!), and heading into this morning’s report, the S&P 500 and Nasdaq are indicated to open down by between 0.75% and 1.0%, continuing a week of lousy market action. Treasury yields are higher, crude oil is surging, and gold is fractionally higher.

In Asia, most major indices were flat to lower, but still finished the week sharply lower, with the Nikkei down 5.5%, China down 2.1%, and South Korea down more than 10%. In Europe, the losses are even larger, with the STOXX 600 down over 1%, taking its decline for the week to over 5%. Across the continent, every major benchmark is down over 5% this week.

Besides the Employment report, Retail Sales also hit the tape at 8:30. The employment report was a disappointment across the board as Non Farm Payrolls fell 92K versus forecasts for an increase of 55K, and the Unemployment Rate increased to 4.4% versus forecasts for 4.3%. Average hourly earnings were slightly higher than expected, rising 0.4% versus forecasts for an increase of 0.3%. As bad as that report was, it will be interesting to see if there were any weather-related impacts. While the jobs picture was weaker, Retail Sales came in better than expected.

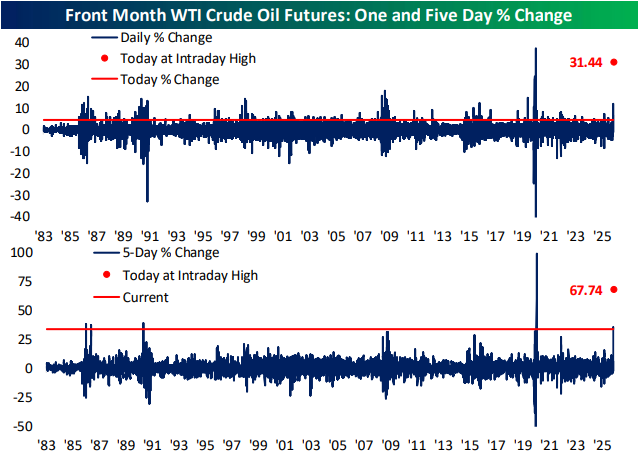

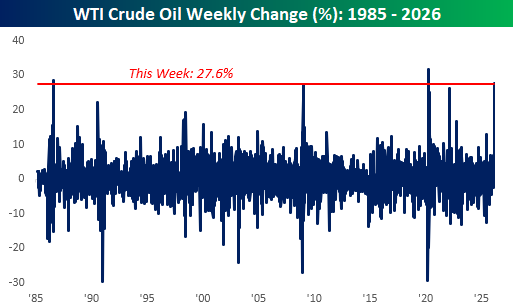

When markets opened for trading on Monday, and crude oil prices rallied a bit over 5%, it was viewed as a surprisingly muted reaction to a monumental event in the Middle East. It looked like we got off easy. As the days have gone on and the conflict has continued, crude oil prices rose every day this week with a 4.7% gain on Tuesday, a 0.1% gain on Wednesday, an 8.5% gain on Thursday, and what’s shaping up to be a 6.5% gain today. The frogs in the market pot had no idea what was coming.

Adding them all together, WTI is on pace for a 27.6% gain this week, which would rank as the third-largest weekly gain since at least 1985. The only two larger gains were 31% in early April 2020 during Covid and 28.4% in August 1986 when OPEC announced a surprise production cut. One-week rallies of this magnitude aren’t very common.

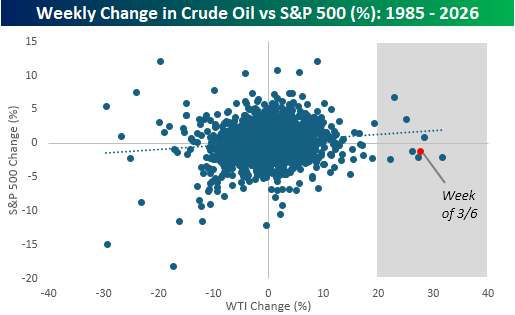

With oil prices up so sharply, it’s not surprising that equities have been under pressure, but looking at past moves shows that the inverse relationship isn’t as strong as you would think. The chart below compares the weekly change in crude oil to the S&P 500 going back to 1985, and there’s little correlation between the weekly direction of crude oil prices and the S&P 500. If anything, the correlation is slightly positive.

The shaded area includes each of the prior weeks when crude oil prices were up 20%, and of the seven occurrences, the S&P 500 was up three times and down four. For all seven weeks, the S&P 500’s median decline was 1.2%. Based on where futures are trading right now, guess how much the S&P 500 is down this week? 1.2%!

Mar 5, 2026

Log-in here if you’re a member with access to the Closer.

- Front month crude oil is setting up for a golden cross; a technical pattern that has historically played out to be less bullish than its reputation implies.

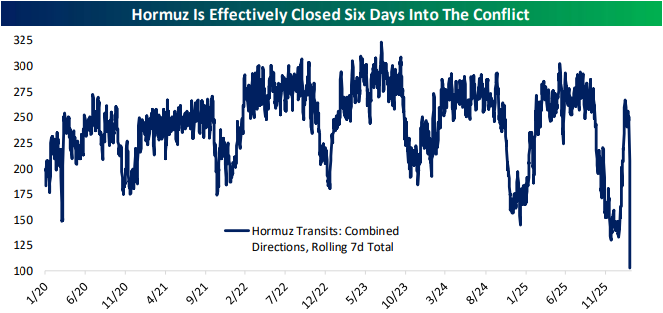

- The closure of Hormuz has resulted in extreme upside skew in options markets for crude oil.

- Labor productivity received material upward revisions for the past six quarters.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 5, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The world makes much less sense than you think.” – Daniel Kahneman

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 crept into positive territory for the week, which was incredible given the circumstances, but futures are set to erase those gains at the open. Both the S&P 500 and Nasdaq are indicated to open down by 0.25%. The biggest driver of weakness is crude oil, where prices are up another 3% to $77. It’s simple at this point: the more crude oil rises, the bigger a headwind it will be for equities.

In Asia, stocks were higher across the board, with the biggest gains coming from South Korea, where the KOSPI rallied 9.6% following the 12% decline on Wednesday. Talk about a rational market! In Europe, the tone is less positive. While markets in the region started the day higher, they have been giving up those gains as the UP open approaches and are now all broadly looking at modest declines.

It’s been a busy morning for economic data, and most of it was better than expected. Initial jobless claims were slightly weaker than expected, and continuing claims were modestly higher. Import Prices were lower than expected, while both Non-Farm Productivity and Unit Labor Costs came in higher than expected.

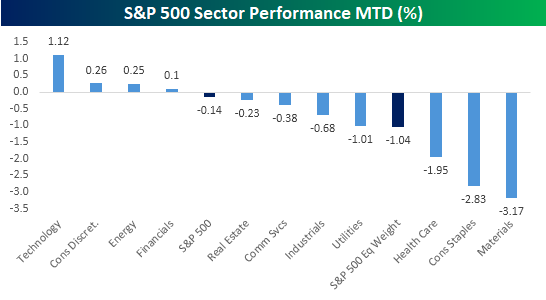

We’re less than a week into the war in Iran, but it’s never too early to see what trends within the equity market may be starting to emerge. At the sector level, you would expect to see a rush into defensive areas as investors rein in risk at the expense of cyclicals. So far, we’ve seen nearly the opposite play out. While the S&P 500 is up so far this week, which is surprising in itself, the four sectors outperforming the market are Technology, Consumer Discretionary, Energy, and Financials. If you had asked most people what sectors would outperform the market following a full-scale breakout of war in the Middle East, the only one of those four sectors that would come to mind is Energy.

The sectors you would expect to outperform in the event of war would be defensives like Utilities, Consumer Staples, and Health Care. But guess what? They’re three of the four worst-performing sectors with declines of at least 1% each! While the S&P 500 is surprisingly higher this week, the rally is primarily due to the 1%+ gain in the Technology sector. On an equal weight basis, the index is down 1.04%, and 60% of its components are down MTD.

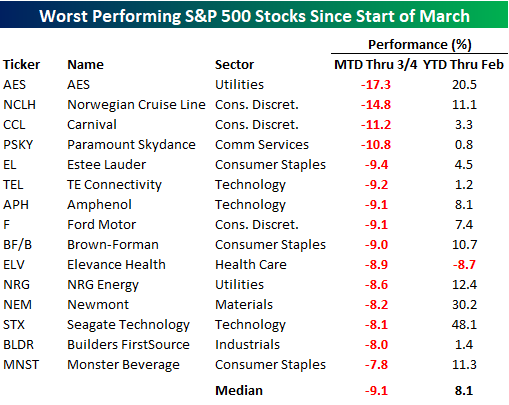

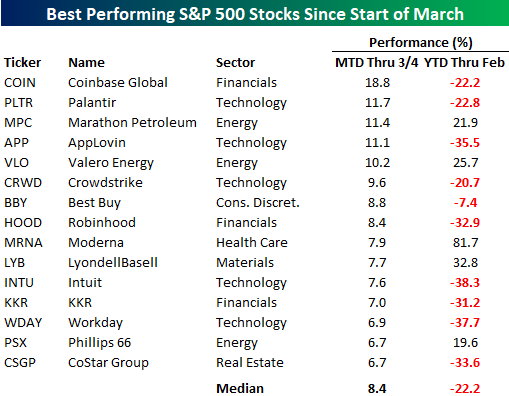

At the individual stock level, the list of winners is mostly devoid of defensive stocks. Instead, it’s littered with stocks that were recently considered some of the hottest growth stocks in the market before falling on hard times in late 2025 and earlier this year. Of the 15 top-performing stocks in the S&P 500 since the war broke out, their average YTD change in the first two months of the year was a decline of 22.2%, and ten of them were in the red. The two top-performing stocks – Coinbase (COIN) and Palantir (PLTR) – were both down over 20% in the first two months of 2026. While PLTR, with its military contracts, benefits from geopolitical instability, it’s hard to look at most of the other non-Energy stocks and see the obvious reason as to why they would benefit.

While the list of winners is mostly stocks that were down sharply YTD, all but one of the stocks on the list of losers were up YTD heading into March. Their average YTD gain was 8.1%, and seven were up by double-digit percentages. Leading the way lower, AES was up 20%+ YTD heading into March, but it has given most of that back in the first few days of March. Behind AES, cruise operators Norwegian Cruise Line (NCLH) and Carnival (CCL), along with Paramount Skydance (PSKY), are the only other stocks down by double-digit percentages. The declines in NCLH and CCL make sense given the geopolitical uncertainty, but the drop in PSKY is company-specific and tied to the merger with Warner.

Looking both at sector and individual stock performance since the war broke out, it seems as though investors have taken a back-to-basics approach, focusing on what had been working rather than what was working at the time that hostilities broke out. Whether that’s due to trade unwinds and short-covering given the heightened uncertainty or a reversion to tech remains to be seen, but in the early going, market performance and internals have done what they always do – surprise nearly everyone.