Jun 3, 2026

Log-in here if you’re a member with access to the Closer.

- Strategic petroleum reserves continue to experience a record drawdown as distillate inventories approach multi-decade lows.

- Even after an updated methodology was introduced in 2022, the explanatory power of the ADP payrolls estimate for the official BLS data is very low.

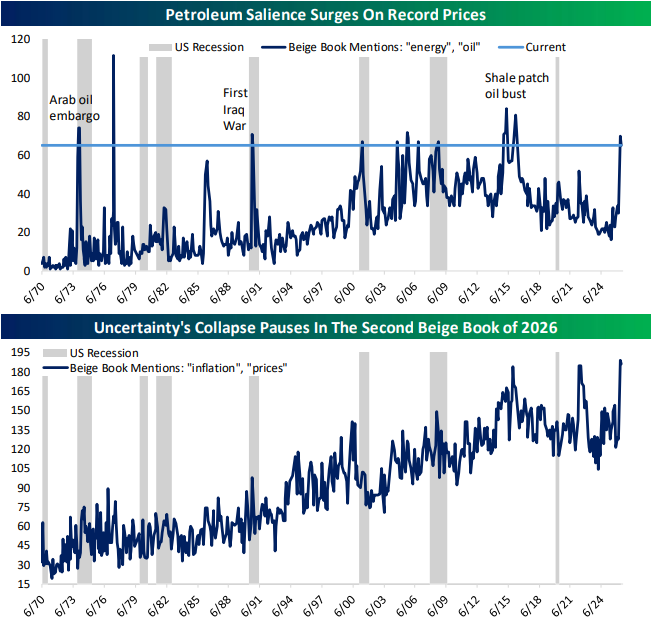

- The latest release of the Beige Book showed slightly weaker evaluations of the economy relative to the prior release as inflation and energy mentions were commonplace.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 3, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I never learned anything while i was talking.” – Larry King

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We’ve seen a mixed picture in equity futures this morning, with the S&P 500 indicated to open less than 10 bps lower while the Nasdaq looks to open 0.2% higher as strength in tech stocks continues to drive the market higher. Treasury yields are slightly higher, with the 10-year up 2 bps to 4.48% while the 30-year yield once again flirts with 5%. Oil prices are 2% higher as the US and Iran traded military strikes overnight, threatening to upend any hopes for a resolution in the war. Gold prices are down almost 1% while Bitcoin is basically unchanged.

Asian markets were mixed again overnight. The Nikkei surged 2.5% to a record high, fueled by technology stocks. Stocks in Hong Kong moved in the opposite direction, falling 1.6%, while China was up slightly and South Korea was closed for a holiday. Service sector PMI indices for May were released and generally were in line with or better than expected.

European stocks have been moving in more unison this morning, and the direction is lower. The STOXX 600 is down 0.5% with a 1.1% decline in Germany leading the way lower, while Spain bucks the negative tide with a rally of 0.3%. The weakness comes despite stronger-than-expected PMIs for the services sector, as renewed tensions between the US and Iran and new proposed tariffs from the US take on a greater significance.

In the US this morning, we’ll also get updated PMI readings for the Services sector along with Factory Orders and Durable Goods, but all that will come after the 8:15 release of the ADP Employment report, which just hit the tapes and came in stronger than expected at 122K versus forecasts for an increase of 120K.

There’s been some incredible streaks unfolding over the last several weeks. Heading into the start of tomorrow’s Memorial Tournament, the world’s number one golfer, Scottie Scheffler, had finished within the top 25 of all 11 tournaments he played in this season, extending his streak dating back to August 2024 to 32. In the modern era (since 1983), Tiger Woods holds the title for most consecutive top 25 finishes with 38 in a streak that stretched from the 1999 Buick Invitational to the 2001 Phoenix Open.

In the NBA, the New York Knicks have won 11 straight playoff games heading into the start of today’s NBA Finals. The only two other teams to win more straight playoff games in a single postseason were the Golden State Warriors (15) in 2017 and the San Antonio Spurs (12) in 1999. Both teams ultimately won the championship, with the Warriors beating the Cavaliers in five games and the Spurs beating the Knicks in 5.

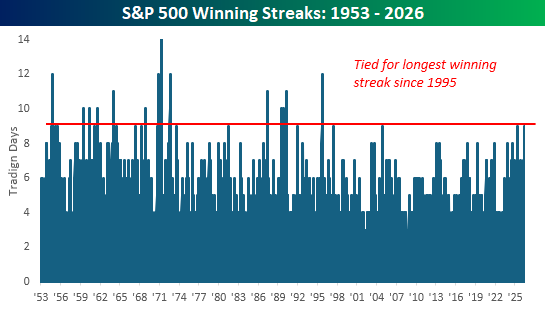

Within the market, we’ve also seen some incredible streaks. In Monday’s Chart of the Day, we highlighted the back-to-back monthly gains of more than 5%, and then on Tuesday, we provided an analysis of the S&P 500’s streak of 21 straight days of closing more than 5% above its 50-DMA. Some other notable streaks worth noting involve the number nine. Heading into this week, the S&P 500 was up for nine straight weeks, and yesterday, the index closed higher for the 9th day in a row!

The chart below shows prior daily winning streaks for the S&P 500, and with yesterday’s gain, the current streak ranks as tied for the longest since 1995. That streak in 1995 lasted 12 trading days and was tied for the second-longest since at least late 1952, when the five-trading-day workweek in its current form started. The longest streak on record was 14 days ending in April 1971.

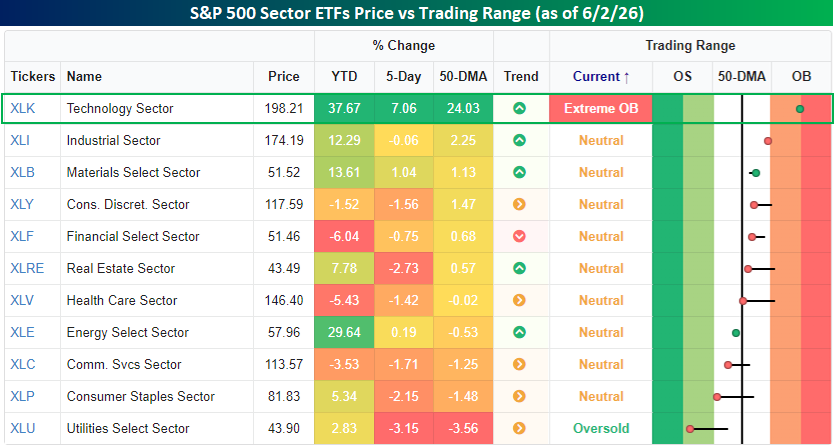

We’ve extensively covered the Technology sector’s outperformance since the March lows. Heading into today’s trading, it’s clearly been a tech and everyone else market. As shown in the snapshot below from our Trend Analyzer, Technology is the only sector trading in “extreme” overbought territory, let alone merely even overbought territory. Further, in the last five trading days, the sector is up over 7%, outperforming the next closest sector by more than seven full-percentage points! Tech doesn’t necessarily have to go down from here, but it’s highly unlikely to keep up this degree of outperformance in the near term.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 2, 2026

Log-in here if you’re a member with access to the Closer.

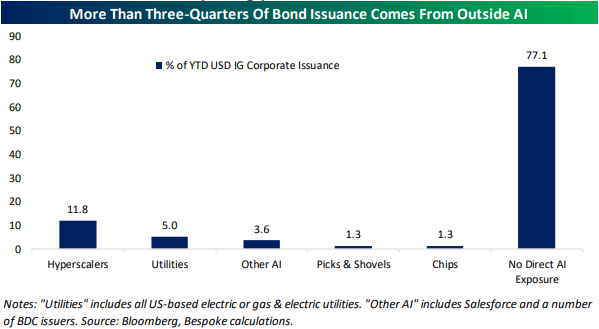

- Credit issuance was extremely strong in May as US corporate bond issuance topped $1trn YTD.

- On news that the CFTC would allow 24/7 financial product trading including crypto perpetual futures, CBOE (CBOE) has fallen 25% in the past ten sessions.

- Private job openings are now the highest since March 2024, and while this series can be a bit volatile, the local trend has started to move slightly higher.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 2, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Though a good deal is too strange to be believed, nothing is too strange to have happened.” – Thomas Hardy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

While Dow futures point to a 0.45% decline at the open, futures on the S&P 500 and Nasdaq are down much less, indicating a decline of less than 0.2%…for now. Crude oil is down 1.5% but still above $90 per barrel, while the 10-year yield declines 5 bps to 4.43%. Gold prices are up over 1% while Bitcoin is down over 3% and back below $70 as traders increasingly lose patience with the crypto space in search of greener pastures.

It’s a quiet day for economic data today, with the 10 AM JOLTS being the only report on the calendar. We’ll also get May vehicle sales data from the major OEMs throughout the day.

Overnight in Asia, it was a mixed session with the Nikkei down 0.3% while Hong Kong and China both rallied. South Korea’s KOSPI experienced a marginal gain of 0.2%, which, relative to recent moves, seems like a decline!

In Europe, the tone is more positive as the STOXX 600 rallies 0.7%, led higher by Italy and Germany. May CPI for the Eurozone increased 3.2% y/y, which was right in line with expectations, while Core CPI was slightly ahead of consensus forecasts (2.5% vs 2.4%).

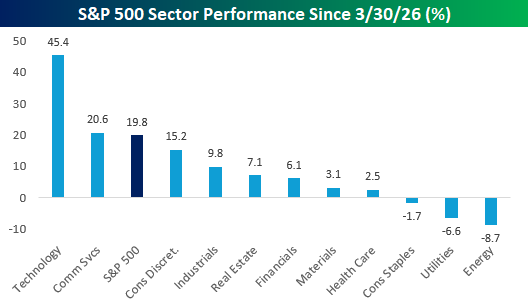

Since the market low at the end of March, the S&P 500 is up just under 20%, but as we are all aware, breadth has been narrow. The lion’s share of the gains has been in the Technology sector, which has rallied over 45%, and the only other sector outperforming the S&P 500 over that time is Communications Services, which is ahead of the index only just barely. The nine other sectors in the S&P 500 are all underperforming the index by a wide margin, including three – Energy, Utilities, and Consumer Staples – which are lower.

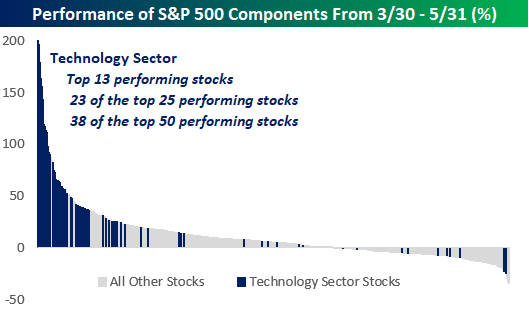

One way to illustrate the dominance of tech since the March low is in the performance of each S&P 500 component. Since the March 30 low, 38 of the top 50 performing stocks are from the Technology sector, including 23 of the top 25 and all of the top 13. It’s been Technology and everyone else.

Of the top performing stocks since 3/30, the tech stocks dominating the list have primarily been – you guessed it – semiconductor stocks, and more specifically memory stocks. Many of these names doubled or tripled in the span of just two months!

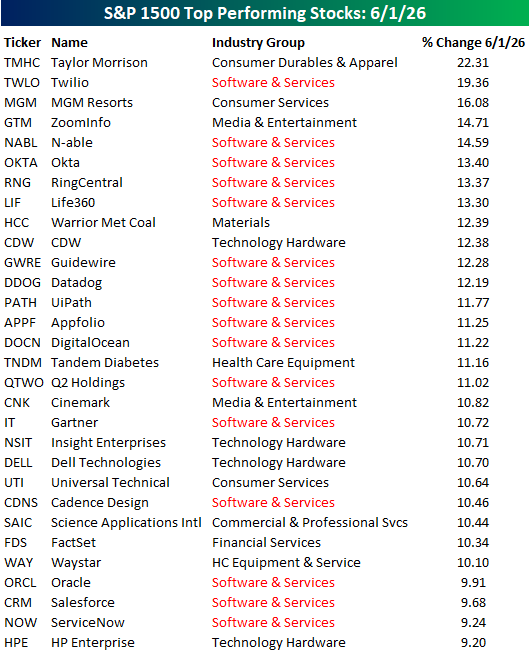

In yesterday’s trading, Technology was once again the top performing sector in the S&P 500 and one of just two sectors to trade higher. In looking at the top performing stocks yesterday, Technology stocks once again dominated the list, but it wasn’t semis. In fact, of the top 30 performing stocks in the S&P 1500 yesterday, not a single semiconductor stock made the list even though Technology was one of only two sectors to trade higher.

As shown in the list below, yesterday’s dominant group within the Technology sector was software stocks. Of the 30 top performing stocks, more than half were from the Software and Services Industry Group.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 1, 2026

Log-in here if you’re a member with access to the Closer.

- While bond yields finished well off season highs, the 2s30s curve is near its flattest levels of the past year while forward inflation pricing is falling despite higher oil prices.

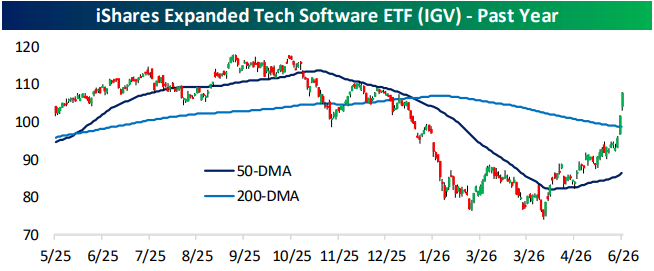

- After back-to-back gains of over 5% on Friday and today, software (IGV) has taken out its 200-DMA and moved into extreme overbought territory.

- Anthropic has filed its draft S-1 confidentially ahead of an IPO and Alphabet (GOOGL) announced it would raise $80 bn in new equity capital.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 1, 2026

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!