Jun 8, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It takes less courage to criticize the decisions of others than to stand by your own.” – Attila the Hun (attributed)

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are bouncing back to start the new trading week with the S&P 500 trading up roughly 0.7% pre-market, and the Tech-heavy Nasdaq 100 up about 1.3%.

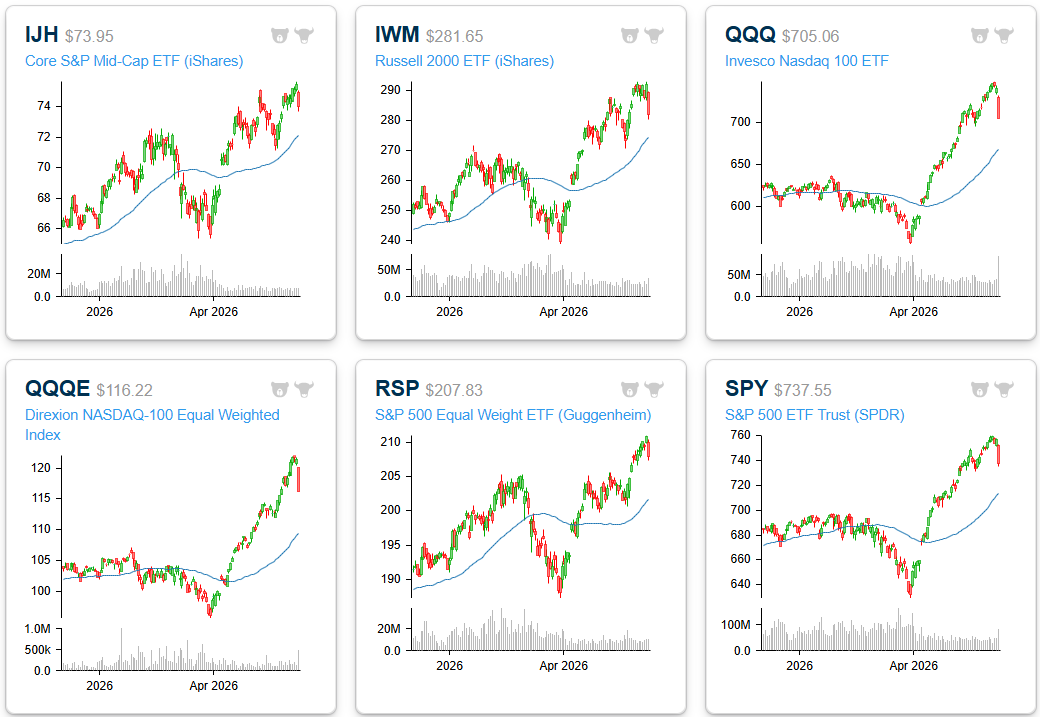

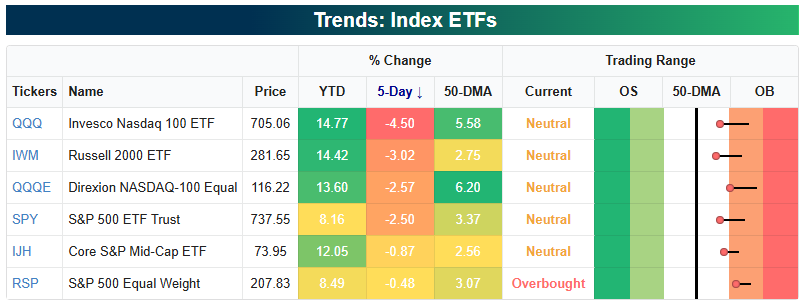

After a 33.7% rally from March 30th through last Tuesday’s close (6/2), traders finally rotated out of the QQQs late last week with a 5% drop from Wednesday through Friday. The S&P 500 ended a nine-week winning streak, and both the S&P and Nasdaq 100 moved out of overbought territory back to “neutral” levels.

As shown below, even with the drop on Friday, there’s still quite a large gap between current levels and the 50-DMA for both QQQ and SPY.

You can see the pullback into neutral territory in the snapshot of key index ETFs from our Trend Analyzer:

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 5, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, choose one of our three member plans today!

This week’s report covers all you need to know about the market this week, including historic moves in major indices and an insatiable demand for equities. Give it a read!

Jun 5, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Inspiration usually comes during work, rather than before it.” – Madeleine L’Engle

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s already been a busy week for employment-related news, and most of it has been good. This morning’s labor report will trump all the other reports and help dictate the direction of the markets heading into the weekend and whether the current streak of weekly gains extends to double digits. Wherever the report comes in, though, remember that it is only one snapshot of a much larger mosaic. Odds are it will be revised multiple times over the next several months (years).

Heading into the last session of the week, equity futures are mostly lower. The Nasdaq is indicated to gap down more than 1%, while S&P 500 futures point to a 0.5% decline, and the Dow is indicated slightly higher. If all of this sounds familiar, it’s because the setup was the same yesterday. There are not really any catalysts to blame for the weakness, except that investors are growing increasingly apprehensive about putting new money to work after the massive tech rally and a coming avalanche of supply.

Outside of equities, treasury yields are modestly lower, with the 10-year yielding just below 4.47%. Oil is slightly higher with WTI at $93.25 per barrel as prospects of a peace deal with Iran continue to dangle just over the horizon that we can never seem to reach. Gold is slightly lower, and Bitcoin is down another 2% and approaching $62K.

In Asia, markets closed out a mostly negative week on a down note, with the Nikkei and Hong Kong falling over 1% while South Korea plunged 5%. In Europe, markets are moving in the other direction. The STOXX 600 is up 0.3%, led higher by Spain, which is up 1%. The gains come despite Q1 GDP being revised from growth of 0.1% to a contraction of 0.2%. That was the first negative quarter for the region since 2021.

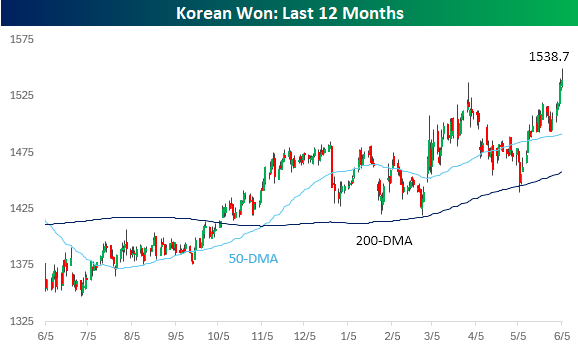

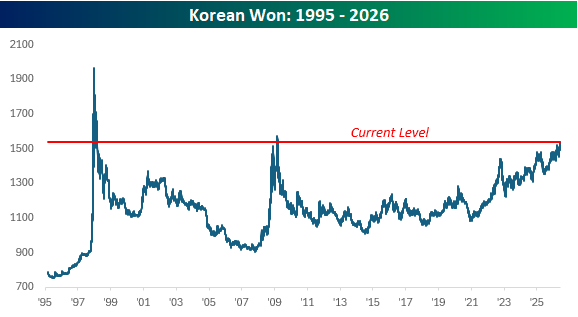

Besides the declines in Asian stocks overnight, the Japanese yen and South Korean won have been weak. Just weeks after the BoJ intervened in the market to defend the currency, the yen has resumed its slide, pushing towards a psychologically important level of 160 versus the dollar. In South Korea, the won has shown steady weakness against the dollar for over a year now (rising line in chart), and just last night traded at its weakest level versus the dollar since 2009.

Many comparisons have been made between the current market environment and the late 1990s, and weakness in Asian currencies can just be added to the list. In 1997, we had the Asian currency crisis, which spawned a global market sell-off, so it’s only natural to raise an eyebrow when you see headlines about the South Korean won hitting multi-year lows versus the dollar.

A look at the long-term chart for the won, however, shows that at this point, the decline looks nothing like the weakness we saw in 1997 and 2008. In both of those periods, the weakness went parabolic, whereas the current period of weakness has been a steadier grind. If the slope of the line starts to steepen, though, put on your seatbelt.

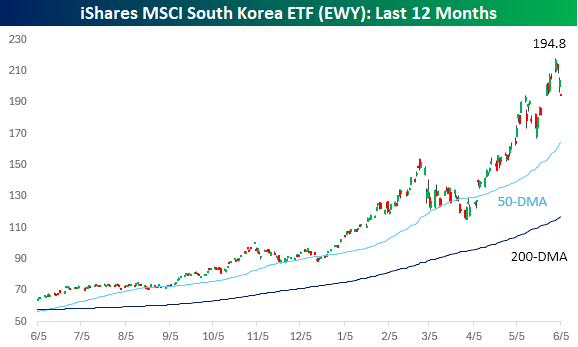

While the won has been weakening, the rate of decline hasn’t been nearly fast enough to offset the rabid gains in the South Korean equity market. Over the last year, the iShares MSCI South Korea ETF (EWY) has more than tripled, rising from around $60 to over $200 earlier this week, and just under $195 in pre-market trading today. At these levels, EWY is holding right at the levels it was after its gap higher in late May after the Memorial Day weekend. If these levels can hold, the recent pullback will look benign, but even after this pullback, prices remain extremely elevated.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 4, 2026

Log-in here if you’re a member with access to the Closer.

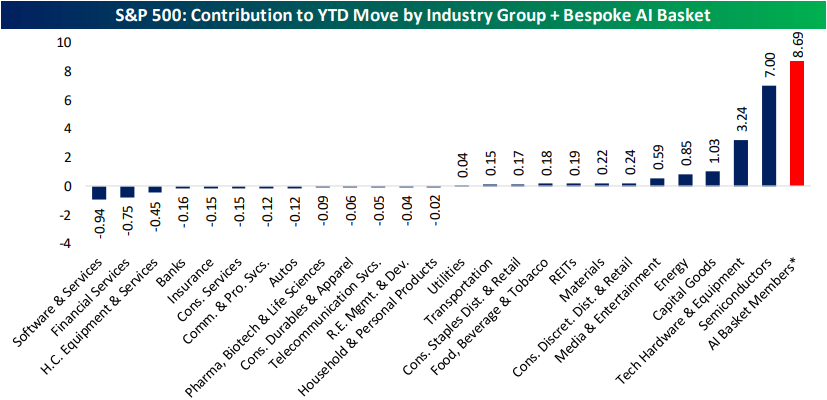

- Low volatility stocks have experienced historic underperformed recently whereas momentum has outperformed massively.

- Tech industries, or more specifically the AI trade, is to thank for a vast majority of YTD gains.

- Home listing prices are down to the lowest level since April 2022 as inventories have risen.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 4, 2026

During the recently-completed Q1 2026 earnings reporting period, there were a total of 184 earnings triple plays out of just over 1,800 individual quarterly earnings reports from US-listed stocks. That’s 86 more than the 98 triple plays we saw during the prior earnings reporting period and 106 more than the 78 reported this time a year ago.

What is a triple play? When a stock reports quarterly earnings, it registers a “triple play” when it beats analyst EPS estimates, beats analyst revenue estimates, and raises forward guidance. We coined the term back in the mid-2000s, and you can read more about it at Investopedia.com. We consider triple plays to be the cream of the crop of earnings season, and we’re constantly finding new long-term opportunities from this basket of names each quarter. You can track the newest earnings triple plays on a daily basis at our Triple Plays page if you’re a Bespoke Premium or Bespoke Institutional member.

To read our quarterly triple play recap and see some of the triple plays with intriguing price charts at the moment, start a two-week trial to Bespoke Premium!

Jun 4, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A good first impression can work wonders.” – J.K. Rowling

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Markets are getting a bit of a reality check this morning as Nasdaq futures are down over 1%, while S&P 500 futures look at a more modest decline of 0.4%. The weakness comes despite crude oil prices trading down over 3% whle the 10-year yield trades down to 4.45%. Gold prices are rallying as investors take more of a risk-off approach, and Bitcoin is down another 3% to less than $64K.

Asian stocks were lower across the board overnight, following the lead of US equities on Wednesday and the follow-through into the overnight session. The Nikkei was down 1.4%, while South Korea fell 1.8%. European stocks have much less exposure to Technology and are therefore experiencing a mixed picture rather than trading broadly lower. The STOXX is down 0.2% with the UK leading the way lower (-0.7%). On the upside, France is up 0.8% while Spain and Germany are both up over 0.5%.

In the US today, along with jobless claims at 8:30, we also got Non-Farm Productivity and Unit Labor Costs. Initial claims were higher than expected, while Non Farm Productivity and Unit Labor costs both came in light. Later today, we’ll also hear from a few Fed speakers.

The news of Alphabet’s (GOOGL) equity offering earlier this week reinforced the idea that AI investment will remain strong for quarters to come, but equity prices have rallied sharply and reflected much of that, so all it takes is one company to at least temporarily wreck the party. Yesterday, the party pooper was Broadcom (AVGO). While the company reported better than expected EPS, inline revenues, and raised guidance, the magnitude of the beats and the guidance raise wasn’t enough given the run in the stock over the last year.

As a result, the stock is trading down 15% in the pre-market, shaving more than $300 billion off its market cap and dragging the rest of the Technology sector down with it. The S&P 500 Technology sector is on pace to gap down over 2% at the open, while Nasdaq 100 futures are down 1.4%. If you own a tech stock that was up a lot over the last few days, you’re looking at some relatively steep losses this morning.

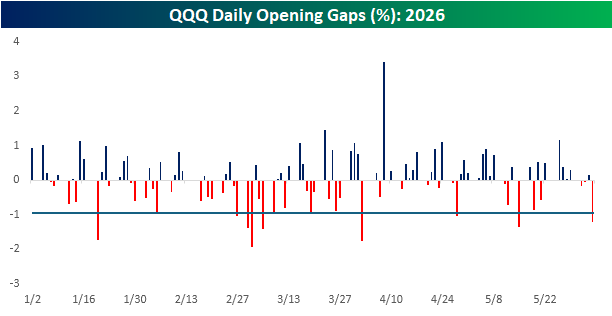

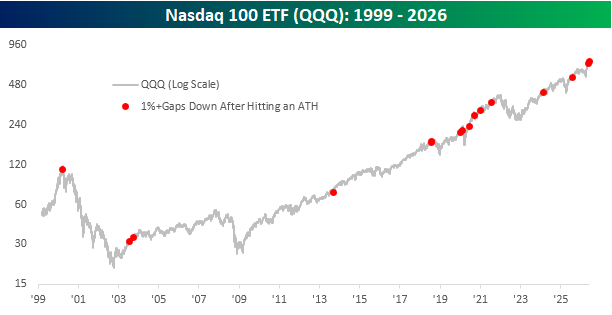

If current levels hold until the open, today will be the Nasdaq 100 ETF’s (QQQ) 9th downside gap of at least 1% this year and the 533rd since its inception in 1999. In other words, these types of declines are relatively common.

What makes this morning’s decline somewhat more unique is that it comes after QQQ traded at an all-time high on an intraday yesterday. Since the ETF’s inception in 1999, there have only been fifteen other occurrences when it gapped down 1%+ the day after hitting an all-time high. Ironically, though, this is the second occurrence in less than a month. Less than three weeks ago, QQQ gapped down 1.34% the day after hitting an all-time high the day before.

The chart below shows each of those occurrences going back to 1999. The first occurrence was in March 2000, coinciding with QQQ’s peak from the dot-com bubble. From there, QQQ fell more than 50% over the next year and ultimately declined more than 80%. First impressions tend to linger, so investors around at the time have nightmares about that type of setup. Besides the March 2000 occurrence, most of the other times that we saw QQQ gap down 1%+ after hitting an all-time high occurred in the middle of longer-term bull markets rather than at the end.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.