Jun 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stocks? We don’t have those Enron-type connections.” – Tony Soprano

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 10, 2026

Log-in here if you’re a member with access to the Closer.

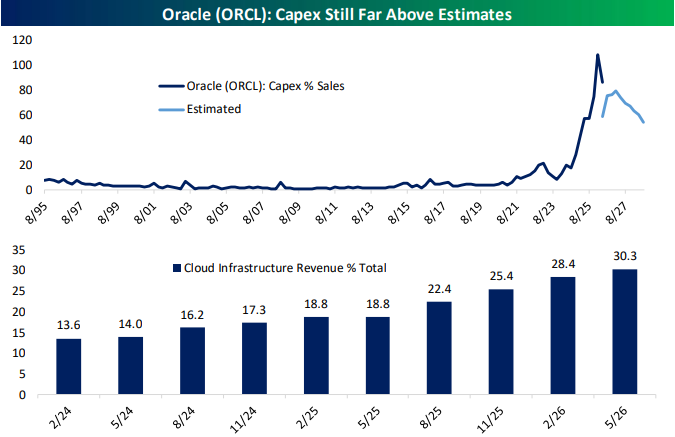

- While Oracle (ORCL) capex appears to have peaked, it still came in at 86% of revenues.

- The recent selloff in equity indices has helped push the forward P/E ratio of the S&P 500 back down to 20.2x, or just below 5% forward earnings yield.

- Petroleum stockpiles continue to rapidly unwind, especially for strategic reserves that are now only 2.4 mm bbls above the July 2023 low.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 10, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I believe in the idea of the rainbow. And I’ve spent my entire life trying to get over it.” – Judy Garland

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

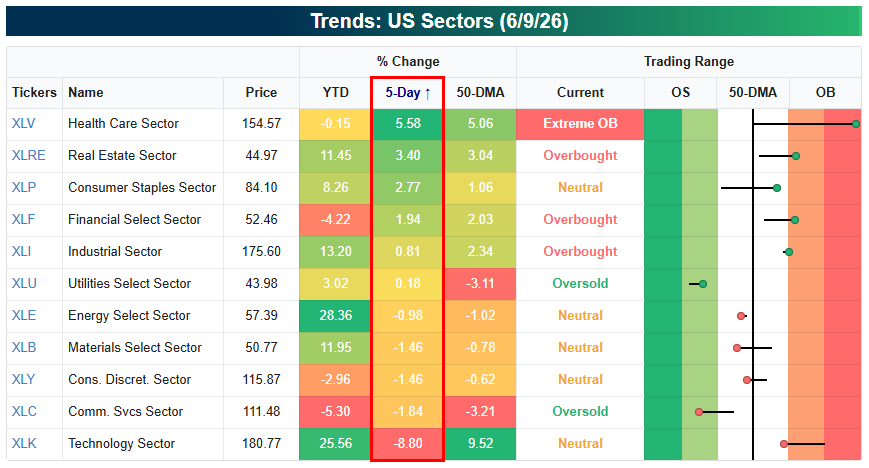

US stocks are down and bond yields up ahead of the open after President Trump suggested on Truth Social that the US will resume bombings of Iran. Leading up to Trump’s comments, futures were already pointed lower, however, led by Tech.

It’s important to note that we’re seeing rotation within the market rather than out of the market. Yes, the broad indices are down because of Tech’s large weighting, but we’ve seen nice gains for sectors like Health Care, Real Estate, Consumer Staples, and Financials as Tech has been selling off.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 9, 2026

Log-in here if you’re a member with access to the Closer.

- Tech has experienced a painful 5-day selloff that has taken it down 8.9% off of its high one week ago.

- Price and breadth were disconnected once again with today marking the 37th time this year that price and breadth moved in opposite directions.

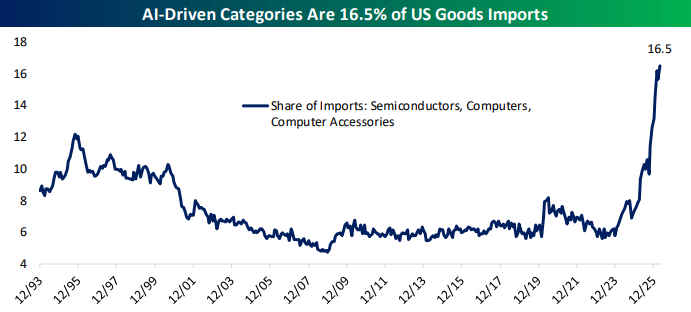

- AI-linked categories of imports continue to rise exponentially; accounting for 16.5% of total goods imports in April

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 9, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s not supposed to be easy. Anyone who finds it easy is stupid.” – Charlie Munger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

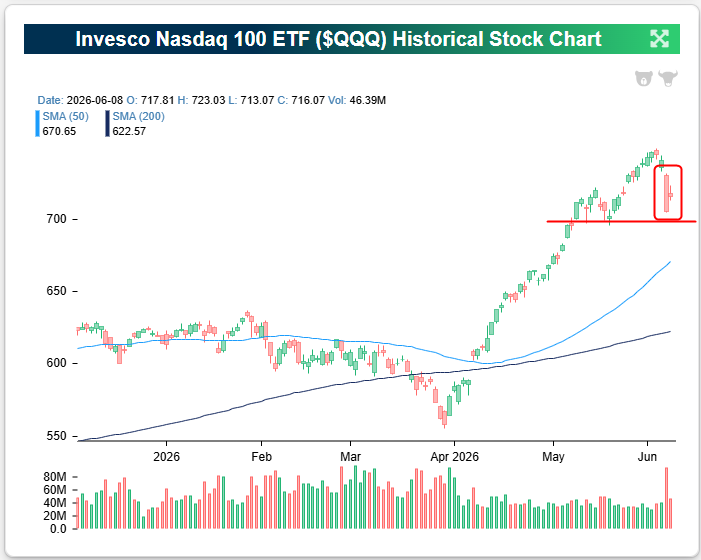

Crude oil is back below $90 this morning after President Trump suggested that a deal with Iran could be reached in the next 2-3 days. Equities are rallying as well with SPY up 40 bps pre-market and QQQ up double that at 80 bps.

Semis, AI, and quantum names are dominating the list of pre-market winners as investors rotate back into the areas that got hit hardest late last week.

After a 4%+ drop on Friday, the Nasdaq 100 (QQQ) rallied back 1.5% yesterday to start the new trading week. As shown below, the intraday range yesterday looks tiny compared to the huge red bar seen Friday. QQQ still needs to gain 3.3% just to get back to its closing level last Thursday.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 8, 2026

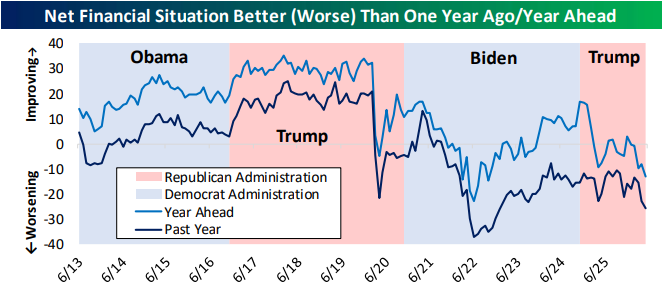

Log-in here if you’re a member with access to the Closer.

- Consumer facing stocks like durables, apparel, and lenders have made lower highs recently.

- The New York Fed’s Survey of Consumer Expectations saw a multiyear low in the range of one year inflation expectations.

- Consumer expectations for their financial situation in the year ahead had the worst showing since October 2022.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!