Jun 12, 2026

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report we start with a review of the successful trading debut for SpaceX (SPCX). While that event sucked up all the headlines this week, one relatively obscure US economic release was far more important and we go into detail why. We also dive into the performance of a range of stocks in our Bespoke AI Basket, review the strong year for emerging markets and which countries are driving returns, discuss Chinese economic data this week, and review the week that was in US data including inflation, housing, and labor markets. Give it a read!

Jun 12, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers RH’s (RH) Q1 2026 earnings call.

RH (RH) is a luxury home furnishings and design company that sells high-end furniture, lighting, textiles, décor, and interior design services through large-format galleries, sourcebooks, and a growing international footprint. The company provides a useful read on affluent consumer spending, luxury housing trends, interior design demand, and the health of the high-end home furnishings market. RH reported better-than-expected first-quarter results despite ongoing tariff-related sourcing disruptions that left backorders and special orders roughly $75 million above normal levels. Management argued that growth will accelerate sharply in the second half as those delayed orders ship, new galleries contribute, and RH Estates launches. Estates was the dominant topic on the call, with CEO Gary Friedman describing it as RH’s biggest initiative ever as a push into the highest end of the luxury home market featuring designer brands, bespoke customization, and new incentives for architects and interior designers. Management also emphasized that the company does not need a housing recovery to meet guidance, noting that the housing downturn has already stretched toward four years. International expansion remained another key focus, with Madrid and Milan now open and London viewed as the critical launch point for building RH into a global luxury brand. RH shares were down roughly 5% for the better part of the trading day on 6/12…

Continue reading our Conference Call Recap for RH by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jun 12, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Adobe’s (ADBE) Q2 2026 earnings call.

Adobe (ADBE) is the leading provider of creative software, document productivity tools, and digital marketing platforms. Its products, including Photoshop, Illustrator, Premiere Pro, Acrobat, Firefly, and Adobe Experience Cloud, serve everyone from individual creators and students to Fortune 500 marketing teams. Adobe sits at the intersection of several major technology trends, making it a useful barometer for AI-driven content creation, digital advertising, enterprise marketing software, and the broader creator economy. Its scale is notable, with more than 850 million Acrobat and Express monthly active users and over 90 million users across its Creative freemium products. Adobe delivered a triple play this quarter, growing revenue 11% to $6.62 billion and raising full-year guidance, but the biggest story was a push toward aggressive AI-driven user acquisition. Management believes AI is fundamentally changing how people discover and use software, prompting Adobe to prioritize frictionless freemium experiences in Firefly, Acrobat AI Assistant, and Express over near-term ARR growth. Traffic to adobe.com grew more than 40%, Firefly ARR increased roughly 50% sequentially, and AI-first ARR surpassed $500 million. On the enterprise side, Adobe highlighted growing demand for agentic AI marketing tools, customer experience orchestration, and brand visibility solutions, bolstered by the recent SEMrush acquisition. Despite the triple play, ADBE shares fell 7.1% at the open on 6/12 due to news that the company’s CFO will be leaving…

Continue reading our Conference Call Recap for ADBE by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Jun 12, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think we have a duty to maintain the light of consciousness, to make sure it continues into the future.” – Elon Musk

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Jun 11, 2026

Log-in here if you’re a member with access to the Closer.

- In reaction to more peace talk headlines, Brent crude oil fell to the lowest level since mid-March and the 30-year Treasury yield fell below the 50-DMA on an impressive outside day reversal.

- AI stocks have been pulling back leaving some Implementation basket stocks at interesting technical levels.

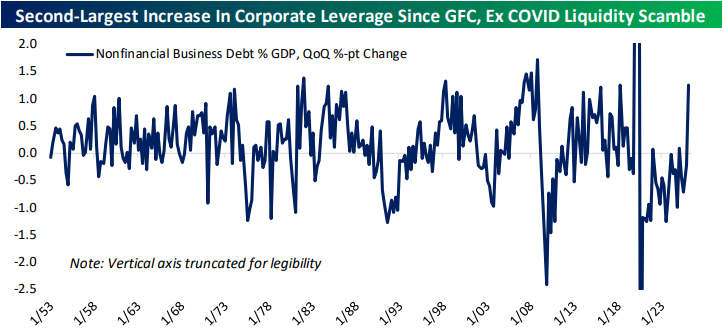

- Nonfinancial business debt as a percentage of GDP rose by one of the largest amounts on record since the end of the GFC.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Jun 11, 2026

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Oracle’s (ORCL) Q4 2026 earnings call.

Oracle (ORCL) is one of the world’s largest enterprise software and cloud computing companies, selling the software, databases, and cloud infrastructure that large organizations use to run their operations. While Oracle is best known for its database business, the company has become an important player in cloud computing and AI because so much enterprise data already sits on Oracle systems. That gives Oracle a view into where companies are actually spending on AI and how quickly those projects are moving from testing to real-world deployment. Oracle’s quarter was dominated by one theme: demand for AI computing power is growing faster than the industry can build it. Cloud infrastructure revenue jumped 93%, while the company’s backlog of signed but unrecognized business reached $638 billion, up 363% year-over-year. Oracle signed $67 billion of new AI infrastructure contracts during the quarter and said customers continue to commit billions of dollars years in advance, often prepaying or supplying their own hardware to secure capacity. To keep up, Oracle plans to spend roughly $70 billion on data center expansion in fiscal 2027 and expects to bring significant new capacity online throughout the year. Outside of infrastructure, management said customers have largely moved beyond AI experimentation and are now deploying AI agents inside business software to automate tasks like recruiting, customer service, and healthcare workflows. Despite better-than-expected revenue and EPS, ORCL shares opened 11.2% lower on 6/11…

Continue reading our Conference Call Recap for ORCL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan