Mar 17, 2026

Log-in here if you’re a member with access to the Closer.

- Since the last FOMC meeting on January 28th, the Fed Funds future curve has shifted justifiably and dramatically.

- Stocks with the highest international revenue exposure have seen large moves since the start of the war in Iran.

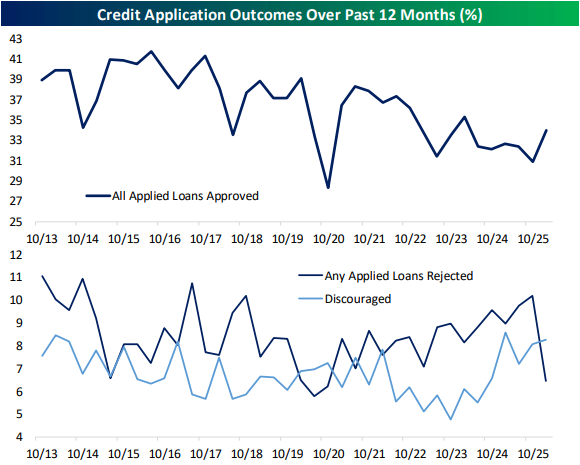

- February saw a steep decline in the number of consumers receiving rejections after applying for credit.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 17, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Competitive golf is played mainly on a five-and-a-half-inch course… the space between your ears.” – Bobby Jones

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As hard as the bears have been working to push futures lower overnight and this morning, the luck of the Irish won’t quit and has pushed futures on the S&P 500 and the Dow into the green. The Nasdaq isn’t quite there, but it is well off its overnight lows. Treasuries are modestly higher, pushing yields slightly lower, while crude oil rebounds more than 2% to $95 per barrel. Gold prices are fractionally higher, and Bitcoin is basically flat.

It’s a quiet day for economic data today, with Pending Home Sales and Leading Indicators the only two reports on the calendar, and both will be released at 10 AM.

In international markets, Asian stocks were mixed overnight, while Europe is mostly higher, with the STOXX 600 up 0.5%. Those gains come despite ZEW Economic Sentiment Indices coming in significantly weaker than expected, as concerns over the war in Iran weigh on sentiment.

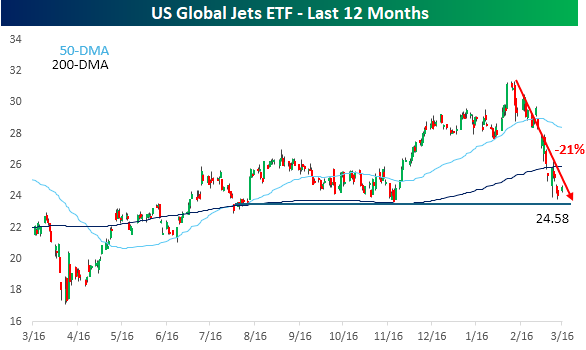

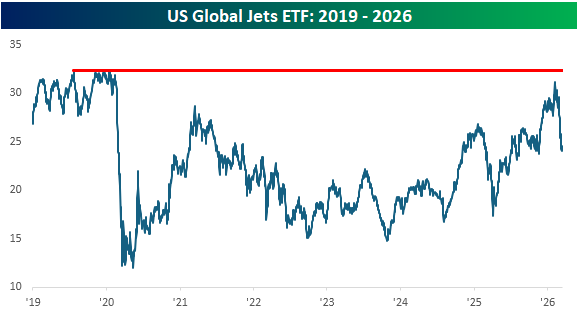

Can it get any worse for airline stocks? After already dealing with the government shutdown where TSA agents aren’t getting paid, the war with Iran has caused jet fuel prices to double and raised the threats of terrorism, which, at the margin, causes travel plans to decline. Since its peak in early February, the US Global Jets ETF (JETS) has plunged more than 20%, effectively erasing the gains from late last year after it broke out of a multi-month trading range. At $24.58, the ETF closed yesterday right near support at the low end of that prior range.

With all the headwinds facing the sector, it’s not looking like the Q1 earnings season is a period that airlines are looking forward to. Despite that backdrop, it was surprising to see comments from Delta CEO Ed Bastian this morning where he said that despite the negative impact of rising energy prices on company margins, the weakness has been completely offset by exceptionally strong demand. In his interview on CNBC, Bastian noted that “We’ve seen eight of the top 10 sales days in our history this quarter, and five of those just within the last two weeks, within just the last week of March”. With demand like that, we can only imagine what the company’s quarterly results would have looked like had there not been a war!

Looking at the airline stocks from a longer-term perspective, the timing of the Iran war couldn’t have been worse. At its recent peak in February, the JETS ETF traded above $31 and was within a dollar of its pre-Covid highs. It’s been a long slog for the sector, but after more than six years, it’s almost back to even.

Mar 16, 2026

Log-in here if you’re a member with access to the Closer.

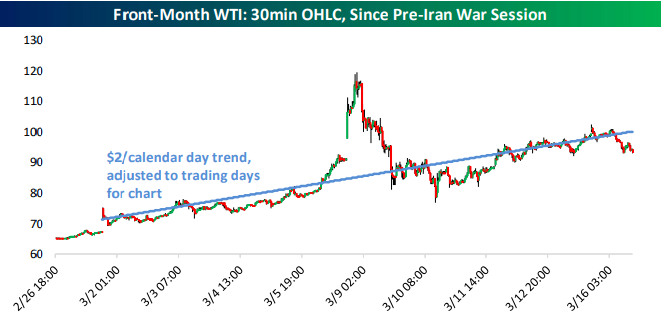

- Despite the dip today, front month WTI is rising at a $2/day pace.

- Positioning data is beginning to reflect adjustments in energy and agriculture commodity futures as a result of the closure of the Strait Hormuz.

- Consumer lending, private equity, and private credit stocks are down as IG credit spreads have soared.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Mar 16, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Philosophy is common sense with big words.” – James Madison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been a tough few weeks for equities. After months of trading in a sideways range, the war in Iran has put an added weight on the bearish side of the scale, pushing stocks lower. All of the major US indices are below their 50-DMAs, and the 200-DMAs are now starting to come into play as well. The short-term key has been and will continue to be oil prices. With no spike this morning, equities are taking the opportunity to rally, and we’ve been picking up steam as the morning drags on. The S&P 500 is on pace to gap up 0.75% as the open, while the Nasdaq is up closer to 1%. Now, let’s see if the gains can hold!

Outside of equities, treasury yields are falling with the 10-year yield down 5 bps to 4.24%, and crude oil falls almost 2% to just under $97 per barrel. Gold prices are down just over 1% and barely hanging on to $5,000, while bitcoin is up nearly 3% and above $73K.

Asian stocks were flat to higher to start the week on the optimism that oil prices didn’t spike more after the weekend. Japanese stocks traded down 0.1% while China was down 0.8%. Hong Kong, India, and South Korea, however, all rallied more than 1%. The declines in China came despite better-than-expected February data for Industrial Production, Retail Sales, and Fixed Investment.

European stocks have taken a more muted start to the week. The STOXX 600 is down 0.1% while Germany is up 0.3% and Italy drops 0.3%. It will be a busy week for central banks on the continent as the ECB, BoE, and SNB all have meetings.

It’s a relatively busy day for economic data this morning, with the Empire Manufacturing report for March hitting the tape at 8:30, followed by Industrial Production and Capacity Utilization at 9:15. Homebuilder sentiment will come out at 10 AM. Another area of focus today will be on Nvidia (NVDA) as CEO Jensen Huang will give the keynote speech at his company’s GTC conference at 2 PM Eastern. Looking ahead, the Fed will announce its latest policy decision on Wednesday.

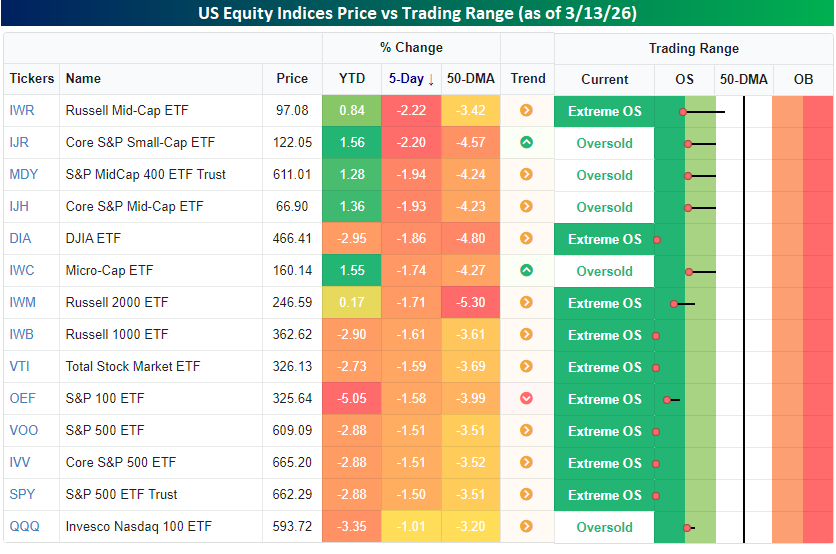

The S&P 500 has declined for four straight weeks now, but still hasn’t even declined 5% from its closing high in late January, so while it’s been a slump, it could be worse. Even with the relatively modest declines, as we discussed in Friday’s Bespoke Report, it still finds itself in what we consider ‘extreme’ oversold levels as it closed more than two standard deviations below its 50-DMA. Along with the S&P 500, the majority of other US index ETFs also finished off last week in extreme oversold territory, and the ones that aren’t are still in oversold territory.

Last week, there was a little bit of rotation in the market where the indices that had been performing the best YTD (small and mid-caps) experienced the largest declines, while large caps, which had been the weakest, were down less. It’s all relative, though, as even the best-performing US indices last week were still down over 1%.

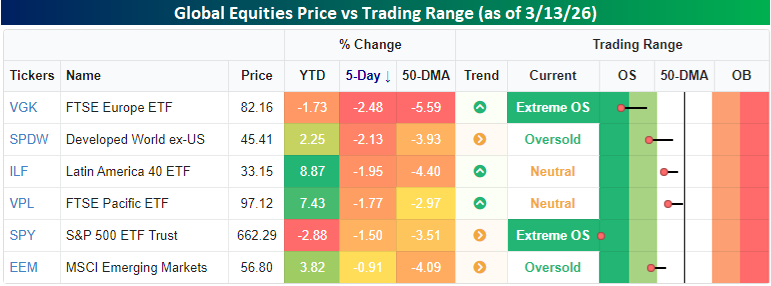

Similar to the relative outperformance of large caps versus small caps last week, US stocks outperformed their global peers once again last week, further digging out of their relative hole on a YTD basis. While the S&P 500 was down 1.5%, European stocks traded down by 2.5% last week, putting them into ‘extreme’ oversold territory with the US. The only areas of the world not oversold heading into the new week are Latin America (ILF) and Asia Pacific (VPL).

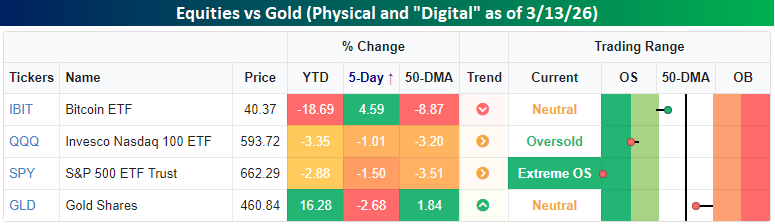

With equities under pressure, investors must be taking shelter in the safety of gold, right? Not really. Physical gold hit a speed bump last week, falling more than 2.5%. Despite the decline, though, it’s still up over 16% YTD and above its 50-DMA, so don’t shed too many tears for the gold bugs. One area of surprising strength last week was in Bitcoin (IBIT). While it’s still down close to 20% this year, it managed to rally more than 4.5% last week. As they say, even a broken clock is right twice a day.

Mar 13, 2026

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Mar 13, 2026

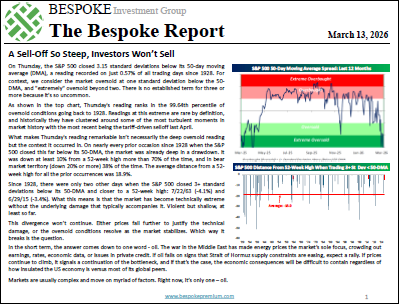

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. It was another eventful week in the market as we witnessed an extraordinary divergence between the S&P 500’s extreme oversold reading despite its relatively close proximity to all-time highs. This divergence won’t continue. Either prices fall further to justify the technical damage, or the oversold conditions resolve as the market stabilizes. Which way it breaks is the question. In this week’s Bespoke Report, we discuss the main factor(s) facing the market and put some of the recent moves into perspective.