B.I.G. Tips – Do Nothing Markets

This content is for members onlyB.I.G. Tips – Next Stop – Earnings Season!

Investors are preoccupied with trade issues and impeachment headlines this week, but earnings season is coming up right around the corner. Whether the earnings headlines provide a welcome break from all the back and forth between the US and China or Republicans and Democrats remains to be seen, but at least it will be a change of pace.

Once again this month, the key trend to watch this earnings season will be how often the term ‘China’ or ‘tariffs’ comes up in quarterly conference calls. Just this morning, the NFIB reported in its Small Business Sentiment report that “Tariffs are adversely affecting many small firms, with 30% reporting negative effects in NFIB’s September survey.”

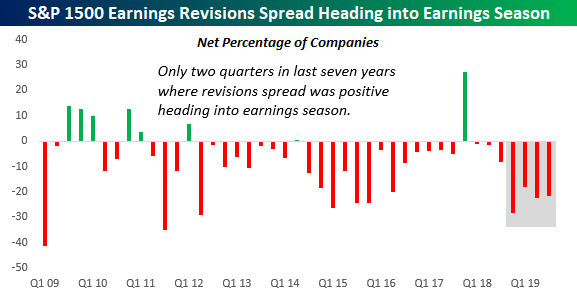

Based on the commentary, current trade policies are obviously making their presence felt. The only question is how much is priced in? Based on recent trends in analyst revisions, analysts have adjusted their forecasts by a decent amount. Over the last four weeks, analyst revisions have come in at a pace of two to one in favor of downside revisions. Analysts have raised EPS forecasts for just 312 companies in the S&P 1500 and lowered EPS forecasts for 634, which works out to a net of negative 322 or 21.5% of the stocks in the index. As shown in the chart below, this continues a trend that we have seen for four quarters now, where analysts have been consistently lowering forecasts in response to the impact of tariffs and other uncertainty related to trade.

We have just published our quarterly preview of the upcoming earnings season and what to expect in terms of the overall market and sector performance based on trends in analyst revisions. To gain access to the full report, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

B.I.G. Tips -September Employment Report Preview

Recession fears continue to rise, and as potential cracks in the economy’s armor start to add up, weakness in Friday’s Non-Farm Payrolls report would definitely hurt sentiment. That’s especially the case after Thursday’s weaker than expected ISM Services report showed Employment at its weakest level in over five years. In terms of the market reaction, prior to this morning, one would have expected a weaker than expected report to be met with selling, but after today’s weaker than expected ISM Services report and the market’s subsequent positive reaction, who knows at this point!

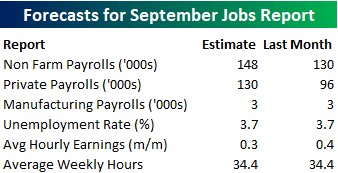

Heading into tomorrow’s Non-Farm Payrolls report, economists are expecting an increase in payrolls of 148K, which would be a slight increase from August’s disappointing reading of 130K. In the private sector, economists are expecting an increase to 130K from August’s reading of 96K. Job growth in the Manufacturing sector is expected to remain at an anemic pace of just 3K. The unemployment rate is expected to remain unchanged at 3.7%, average hourly earnings growth is expected to slow to 0.3% from 0.4%, and average weekly hours are expected to remain unchanged at 34.4.

Ahead of the report, we just published our eleven-page preview of the September jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in September. We also include a breakdown of how the initial reading for September typically comes in relative to expectations and how that ranks versus other months.

For anyone with more than a passing interest in how equities are impacted by economic data, this September employment report preview is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!