Recession fears continue to rise, and as potential cracks in the economy’s armor start to add up, weakness in Friday’s Non-Farm Payrolls report would definitely hurt sentiment. That’s especially the case after Thursday’s weaker than expected ISM Services report showed Employment at its weakest level in over five years. In terms of the market reaction, prior to this morning, one would have expected a weaker than expected report to be met with selling, but after today’s weaker than expected ISM Services report and the market’s subsequent positive reaction, who knows at this point!

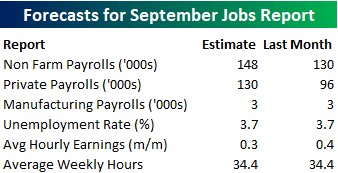

Heading into tomorrow’s Non-Farm Payrolls report, economists are expecting an increase in payrolls of 148K, which would be a slight increase from August’s disappointing reading of 130K. In the private sector, economists are expecting an increase to 130K from August’s reading of 96K. Job growth in the Manufacturing sector is expected to remain at an anemic pace of just 3K. The unemployment rate is expected to remain unchanged at 3.7%, average hourly earnings growth is expected to slow to 0.3% from 0.4%, and average weekly hours are expected to remain unchanged at 34.4.

Ahead of the report, we just published our eleven-page preview of the September jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in September. We also include a breakdown of how the initial reading for September typically comes in relative to expectations and how that ranks versus other months.

For anyone with more than a passing interest in how equities are impacted by economic data, this September employment report preview is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!