B.I.G. Tips – Here Comes Q2 Earnings Season!

Second quarter earnings season kicks off this week as Pepsi (PEP) reports before the open tomorrow, while Kraft Heinz (KHC) reports Wednesday, and Delta (DAL) reports on Thursday. The real action, though, will come next week as the major banks and more than 50 other S&P 500 companies will report results. As shown in the chart below, the busiest day of this earnings season will be on 7/25 when 61 S&P 500 companies are scheduled to report, while the busiest week for earnings will be the following week when a total of 160 companies will be reporting. After that things will quickly start to die down in August.

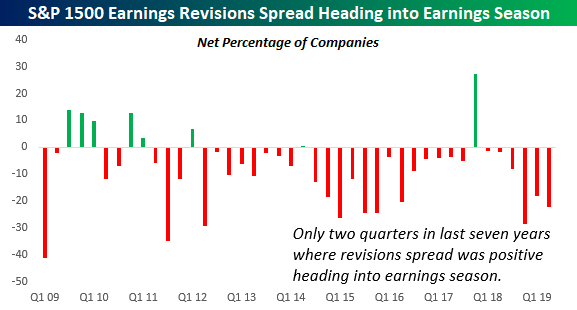

The key trend to watch this earnings season will be how often the term ‘China’ or ‘tariffs’ comes up in quarterly conference calls. With increased uncertainty created by the on-again, off-again escalation of trade disputes between the US and its largest trading partners, we have seen a significant uptick in negative analyst commentary. Over the last four weeks, analysts have raised EPS forecasts for just 278 companies in the S&P 1500 and lowered EPS forecasts for 611. This works out to a net of negative 333 or more than 22% of the stocks in the index. To put this in perspective, there has only been one other quarter in the last three years where the net EPS revisions spread heading into earnings season was more negative than it is now. This doesn’t mean that analysts are normally positive, though. As shown in the chart below, there have only been two quarters in the last seven years where the revisions spread was positive heading into earnings season.

We have just published our quarterly preview of the upcoming earnings season and what to expect in terms of overall market and sector performance based on trends in analyst revisions. To gain access to the full report, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

B.I.G. Tips – Chart Checkup

This content is for members onlyB.I.G. Tips – June Employment Report Preview

With just one day separating the July 4th holiday and the upcoming weekend, you probably figured that Friday would be a throwaway day. Not this time. With the market all but pricing in at least a 25 bps rate cut at the end of the month but many FOMC officials not on the same page (see Mester’s comments from Tuesday), Friday’s employment report will be even more important than normal. You can bet there will be a notable market reaction whether the report is good or bad!

Heading into Friday’s report, economists are expecting an increase in payrolls of 162K, which would be an improvement from May’s much weaker than expected reading of 75K. In the private sector, economists are expecting an increase of 153K, which represents a 63K increase from last month’s weaker reading of 90K. The unemployment rate is expected to remain unchanged at 3.6%. Average hourly earnings are expected to grow at a rate of 0.3% versus last month’s 0.2% reading. Finally, average weekly hours are expected to be unchanged at 34.4.

Ahead of the report, we just published our eleven-page preview of the June jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in June. We also include a breakdown of how the initial reading for June typically comes in relative to expectations and how that ranks versus other months.

For anyone with more than a passing interest in how equities are impacted by economic data, this June employment report preview is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!