Nov 13, 2020

US equity performance this week was dominated by vaccine news. Good data from Pfizer early in the week sparked all-time highs for small caps and robust equity rallies around the world. Technical backdrops have improved dramatically both in the US and Europe versus where they sat just before the US election. The relief rallies in stocks around the world are indicative of just what can happen when risk events are taken off the table. Unfortunately for investors, the risk events moving off the table have been replaced by others: government funding deadlines in mid and late December, as well as more Phase 3 trial data from vaccine companies. In the background, the US economy is starting to slow as COVID prevalence explodes across the country. We discuss all the latest US data, earnings results, and more in this week’s Bespoke Report.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Oct 30, 2020

Talk about a Halloween scare. In a week where the S&P 500 has historically risen 1%, it traded down more than 5% which was its worst one-week performance since the COVID crisis. Even more notable was the fact that it was the worst performance for the S&P 500 in the last full week before a Presidential election on record. At the close on Friday, the S&P 500’s week-to-date decline was nearly twice the decline of the second-worst week in 1932 when the S&P dropped 2.96% in the last full week leading up to the 1932 election of FDR!

It was a very busy week for the market with a traffic jam of worries to contend with. In this week’s Bespoke Report, we give a full recap of everything going on this week and what it means going forward.

This week’s Bespoke Report newsletter is now available for members.

To read this week’s report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Oct 23, 2020

With COVID surging in the US and across the northern hemisphere, we discuss economic impacts that are already starting to appear in survey data. We also review the week that was in global equity markets, the weakening US dollar, rising interest rates, the extremely strong housing market, and of course earnings. It was a very busy week in the US and Europe this week, featuring reports from a wide range of important companies. We give a full recap, including a breakdown of how COVID-sensitive names have reported before previewing the pre-Halloween economic and earnings slate in this week’s Bespoke Report.

This week’s Bespoke Report newsletter is now available for members.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Oct 9, 2020

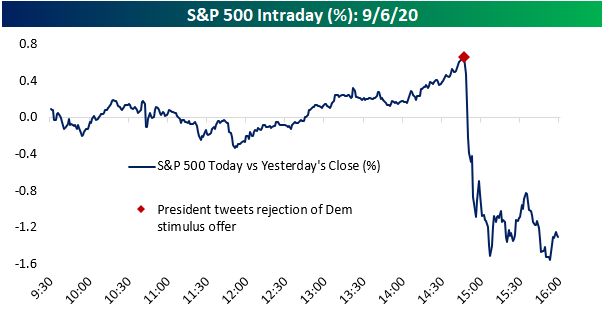

The market may abhor uncertainty, but even with an abundance of it, US equities had their best week in months. The health of the President, the progression of COVID, the ultimate outcome of the election, and the status of another round of stimulus are just a few of the issues facing investors right now, but this week the market was able to grin and bear it and push higher.

That wasn’t necessarily the case on Tuesday, though. What was looking like a good day for equities abruptly headed south after the President put the kibosh on hope for a stimulus deal when he tweeted that he had instructed “representatives to stop negotiating until after the election when, immediately after I win.” With that, the S&P 500 erased a 0.5% intraday gain and finished the day down over 1%. While the reversal was scary to watch, as we noted in our Morning Lineup on Wednesday, “while it’s often tempting to read into these types of late-day sell-offs as an early ‘tell’ for further market weakness, the summary results don’t bear that out.” By the close on Wednesday, the S&P 500 had erased all of Tuesday’s losses, only adding to those gains on Thursday and Friday.

Part of the reason for the recovery in equity prices was the fact that President Trump backtracked on his comments from Tuesday, and by Friday was tweeting and telling Rush Limbaugh that he wanted to “Go Big” with an even larger stimulus bill than the Democrats were proposing!

Where these stimulus talks end up is anyone’s guess, and we’re not sure anything even gets done, but there’s also a lot more to cover in the markets this week. We just published our weekly Bespoke Report newsletter, which covers all of the major events of the week, including the economy, sentiment, the Covid outbreak, key group performance, and the upcoming earnings season. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!