Aug 27, 2021

This week’s Bespoke Report newsletter is now available for members.

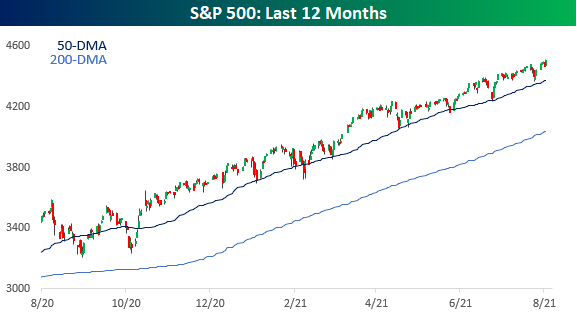

For several days, all the market could do was focus on the upcoming Jackson Hole speech from Fed Chair Jerome Powell. Will he signal in September or won’t he? Well the day finally came, and because the conference was changed from in-person to virtual, we all got to see the speech live on Friday morning. Powell didn’t say anything new, and since that followed a number of hawkish comments from other members of the committee, that was all bulls needed to conquer the day and push the S&P 500 to more record highs.

With the exception of last September and October, the S&P 500 has been in one of the steadiest uptrends ever. Tests of the 50-day moving average (DMA) are few, far between, and extremely short. Meanwhile, the S&P 500 is still maintaining ample social distance with the 200-DMA as that trend line shouts, “Remember me?”

In this week’s Bespoke Report, we cover a lot of different topics. Among them:

- A record number of records and Nasdaq 1,000 point milestones.

- A loot at some high-frequency COVID statistics,

- This week’s surge in crude oil and what it means for energy stocks going forward.

- A review of prior market responses to the GOMC Jackson Hole conferences.

- Bitcoin sentiment.

- Low volume rallies. Do they matter?

- The “Montana Curve”.

- Seasonality. And much more.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Aug 20, 2021

This week’s Bespoke Report newsletter is now available for members.

Before we get started with a preview of our weekly market recap, below we highlight recent performance across a wide range of ETFs representing various asset classes, national equity markets, and US sectors or indices.

- Global equities had a rough week although US stocks saw a decent rally into the close on Friday.

- Small-caps and mid-caps were down the most this week, while Energy, Financials, and Materials fell sharply as well. On the flip side, we saw nice gains in Health Care, Utilities, and Consumer Staples.

- We’ve seen steep declines in countries like Australia, Brazil, Canada, and China this week and this quarter, and international equities are underperforming the US in 2021 by a significant amount.

- The Bitcoin and Ethereum Trusts have surged in Q3, with GBTC up 32.7% and ETHE up 38%. ETHE is back up nearly 100% on the year after the bounce it has had.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Aug 13, 2021

This week’s Bespoke Report newsletter is now available for members.

Before we get started with a preview of our weekly market recap, below we highlight recent performance across a wide range of ETFs representing various asset classes, national equity markets, and US sectors or indices.

Summer trading means a grind higher around the world. Europe hasn’t had a red day in two weeks, while the US earnings season has been as strong versus expectations as any in the past 20 years so far. We discuss the massive beat rates being recorded across the US earnings landscape, record guidance raises, the impact of the Delta variant versus vaccines both in the US and around the world, an inflection point in numerous sentiment indices, potential bottoming out in US housing inventory, sentiment analysis powered by search trends, the fiscal impact of the infrastructure bill, soaring cryptocurrency prices, the partisan divides visible in economic data, and more. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels.

Aug 6, 2021

This week’s Bespoke Report newsletter is now available for members.

Summer Fridays in August are typically quiet as a lot of traders and investors have better things on their minds than the stock market. Better things to do than watch the stock market? That’s hard to believe! What was looking like an extremely quiet week turned out to simply be a quiet one with the release of Friday’s stronger-than-expected July Non-Farm Payrolls. But heading into the closing bell, the S&P 500 was basically flat while the Nasdaq was lower. As we headed into the closing bell for the week, though, the old cliché to never short a dull market proved true again as the US equity market saw modest but broad-based gains on the week.

We cover market breadth, technicals, earnings, the economy, and much more in our full Bespoke Report newsletter. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Jul 30, 2021

This week’s Bespoke Report newsletter is now available for members.

July 2021 lived up to its seasonal script of being the only summer month that typically sees gains. The S&P 500 (SPY) is ending the month with a solid gain of 2.5%, although it dipped red in the final week of the month as earnings and renewed COVID concerns stalled the rally a bit. While large-caps fell in the last week of July, it was good to see small-caps and mid-caps bounce back with gains after trading poorly for the better part of the month. For most of the past month or so, there’s been a concern among bulls that the rally was thinning, so this bounce back in small-caps and general breadth is a positive sign.

We cover market breadth, technicals, earnings, and sentiment in much more detail in our full Bespoke Report newsletter. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Jul 23, 2021

This week’s Bespoke Report newsletter is now available for members.

Stocks roared back to an all-time high close this week, shrugging off a surge in Delta variant cases in the US and around the world. We dive deep into earnings results that continue to run far ahead of analyst estimates, which have no doubt helped stocks recover from their slip last week. In addition to detailed analysis of how US earnings are rolling in, we review major reports from Europe this week as well as previewing major reports from both sides of the Atlantic next week. Fund flows continue to run at a shocking pace, driven by massive buying of bond funds and big inflows to equities too, while the longest commodity bear market in history continues despite 52 week highs for commodities this week. We discuss what high commodity prices mean for equities, as well as reviewing the recent slide in the crypto space. Finally, we review some big housing market data reports this week and take a look at which sectors of the economy are saving too much or too little. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels.