Bespoke’s Morning Lineup – 3/10/26 – The Whole is Worse than the Parts

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think we’re at a bottom. I really do.” – Mark Haines, CNBC, 3/10/09

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a dramatic reversal late in yesterday’s session on hopes that the war in Iran would be ‘complete’ soon, futures were higher for the overnight session and into this morning. As the opening bell approaches, though, futures have been drifting lower, and all of the major averages are on pace to open fractionally lower. Treasury yields are little changed, and crude oil has been volatile, sitting under $90 per barrel. While that seems low relative to Sunday night, it’s still much higher than anything seen in the months leading up to the war in Iran. Gold prices are up over 1.5%, and silver is surging 5% as it’s currently trading at the same price as WTI! Bitcoin has been quietly grinding higher over the last few days, and this morning, it’s above $70K.

Earnings season is largely in the rearview mirror, but after the close, we’ll hear from Oracle (ORCL), which could be a major catalyst tomorrow for different parts of the AI ecosystem. The only economic reports on the calendar today are small business optimism from the NFIB, which came in weaker than expected (98.8 vs 99.5), and then at 10 AM, we’ll get Existing Home Sales for February.

Asian markets followed the lead of the late-day reversal in US equities and traded sharply higher overnight. It wasn’t enough to entirely erase Monday’s losses, but the Nikkei rallied just under 3% while South Korea surged over 5%. Chinese stocks rallied a more modest 0.7%, and while February exports surged 39.6% y/y, exports to the US declined 17%. Those lost exports to the US were scattered across Europe and Southeast Asia, and many of those likely ended up finding their way into the US in a roundabout way. In Japan, GDP rose 0.3% q/q, which was higher than expected, and in South Korea, growth contracted less than expected.

European stocks are also sharply higher this morning as the US reversal occurred after those markets closed for trading yesterday. The STOXX 600 is up 2.3%, and Germany, Italy, and Spain are all up over 2% as well.

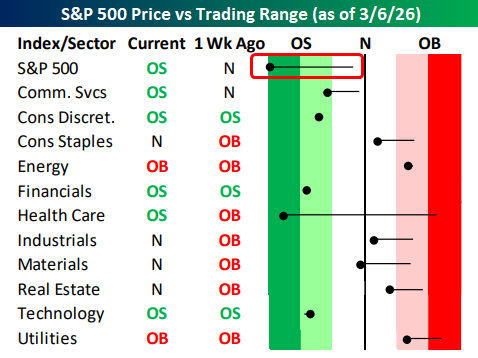

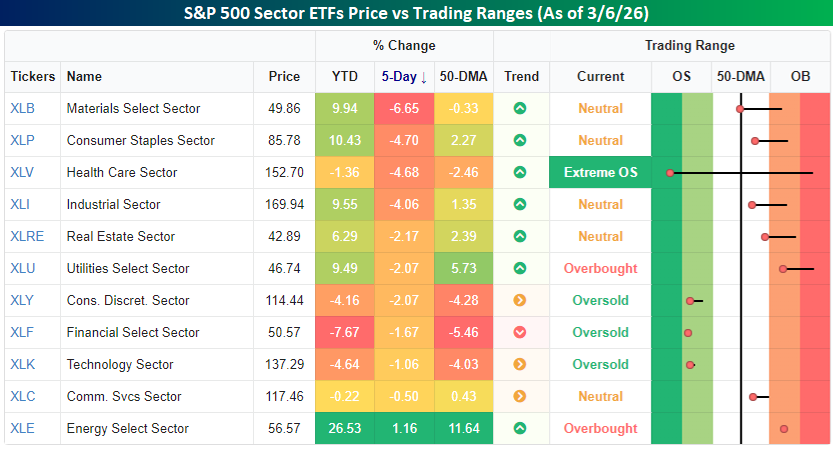

When you looked at page two of the Morning Lineup to see where sectors closed out last week relative to their trading ranges (image below), you may have done a double-take at seeing that the S&P 500 was in ‘extreme’ (2+ standard deviations) oversold territory and more oversold than any sector. In fact, the only other sector in extreme oversold territory was Health Care (after being in extreme overbought territory a week earlier), and just four other sectors were oversold while five were still above their 50-DMAs.

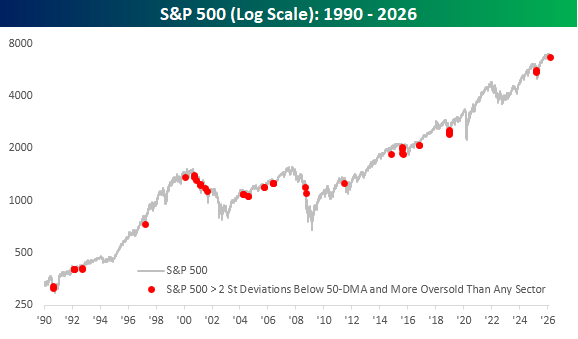

We were curious to see how often it is that the S&P 500 trades in ‘extreme’ oversold territory and is also more oversold than any other sector. Since sector data begins in 1990, there have only been 49 other days when this was the case, and a lot of them occurred during the dot-com bust from early 2000 to late 2001, but as the chart below illustrates, it’s hardly just a bear market phenomenon.

Happy Birthday!

Just how low can stocks go? That was the question posed by the Wall Street Journal on Monday morning, March 9, 2009. Just like this year, March 9th fell on a Monday, following a Friday where the S&P 500 closed sharply lower on economic fears.

That’s where the similarities end. In 2009, the S&P 500 closed below 700 for the first time since 1996; this year, it’s trading not far below 7,000, or roughly ten times higher. Back then, strategists were debating if the index would crater another 27% to reach 500. Having already dropped 56% from its 2007 highs, another leg down felt entirely plausible, but in hindsight, it was the low. Compare that to today: when was the last time you saw mainstream analysts calling for a 27% drop, even with equities right near record highs?

The analysis from that article serves as a reminder of the investor tendency to extrapolate current trends into the future. If stocks are up, they’ll stay up; if they’re sliding, the bottom is always miles away. Analysts often add a ‘countertrend’ hedge in their forecasts just to cover their bases, but take today’s ‘temporary sell-off’ forecasts with a grain of salt. They’re only echoing what the market has been doing. The only way to know for sure is to watch, listen, and let the tape tell the story.

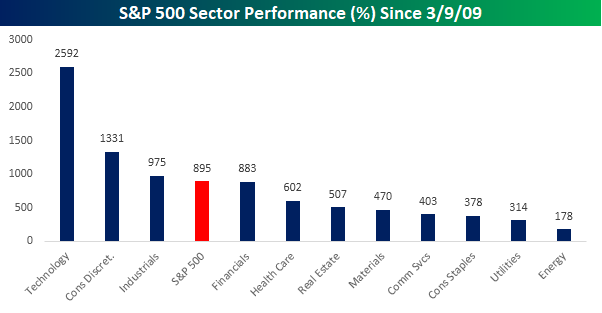

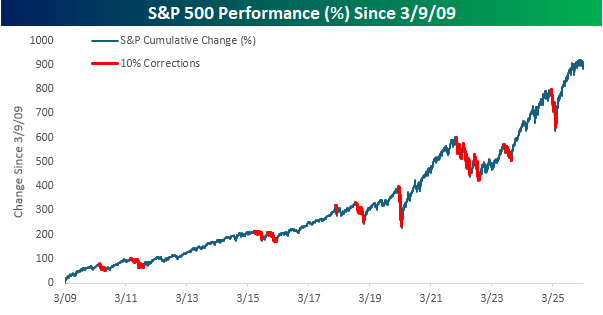

The ride since March 2009 has been incredibly rewarding for those who stayed the course. Since that Monday close, the S&P 500 has rallied 895% (excluding dividends), and more than half of all sectors have risen more than fivefold. Technology has been the top-performing sector with a gain of over 2,500%, followed by Consumer Discretionary, which is up by just over half of that amount. Rounding out the top three, Industrials is the only other sector that has outperformed the S&P 500 since the March 2009 low. While all eleven sectors are higher since March 2009, Energy (178%) and Utilities (314%) have been the worst performers, along with Consumer Staples (378%) and Communication Services (403%), which are the only other sectors that are up less than half as much as the S&P 500.

Have you ever heard anyone say that big gains are right around the corner? Of course not. Looking back at the last 17 years, it seems like the market has done nothing but go up. How many times have you heard someone say that the easy money has been made?

Investing always looks easy in retrospect, but in the moment, it never is. And the last 17 years? The S&P 500 has experienced two bear markets, three other near bear markets (-18%+ from a peak), and a total of 12 different declines of at least 10%. It’s nothing like the period from 2007 to 2009, but there were plenty of moments when putting new money into the market felt like anything but easy. That’s the trick. It’s only easy in retrospect.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Chart of the Day – 1%+ Downside Gaps

This content is for members onlyBespoke’s Morning Lineup – 3/9/26 – It Doesn’t Get More Monday Than This

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There is no instance of a nation benefitting from prolonged warfare.” – Sun Tzu, The Art of War

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If there’s ever a day that feels like a Monday, today is it. As much as we may like daylight savings time for the later sunsets, we could do without the later sunrises after already missing an hour of sleep. Couple that with triple-digit oil prices and much lower equity prices, and we almost wish our alarms didn’t go off this morning.

Equity futures are down over 1% across the board this morning, treasury yields are higher with the 10-year yield now up to 4.17% (it was below 4% less than two weeks ago), and WTI crude oil is up over 10% to $102 per barrel. Incredibly, that’s down around 15% from just under $120 overnight. There’s been no flight to safety in gold either, as prices are down over 1% there too.

Equities in Asia plunged overnight, with the Nikkei down over 5%, while South Korea fell 6.0% after circuit breakers were triggered during the session. In China, CPI for February rose much more than expected, rising 1% after an increase of 0.2% in January. And that was before the spike in oil prices. European equities are also down more than the US. The STOXX 600 is down 1.6% with France down over 2% and Spain down just under 2%. We can try to read into different catalysts for the weakness, but it’s pretty much all oil. Until those prices stop rising, equity prices will continue falling.

The economic calendar is quiet today, and there will be no Fedspeak as the blackout period ahead of next week’s meeting started this weekend. The economic calendar will be very busy, though, with CPI on Wednesday, Jobless Claims, Housing Starts, and Building Permits on Thursday, and Personal Income and Spending, as well as GDP, among others, on Friday.

The war in Iran hasn’t had much of a benefit on any sector, except, of course, Energy. Since the fighting broke out just over a week ago, Energy has rallied over 1% while every other sector is in the red, with nine down more than 1%. Four sectors declined by over 4%, with Materials leading the losses at 6.65%, followed by Consumer Staples, Health Care, and Industrials. Health Care’s losses have taken that sector into ‘extreme’ oversold territory after trading in ‘extreme’ overbought territory just over a week ago. War has a way of changing market conditions very quickly!

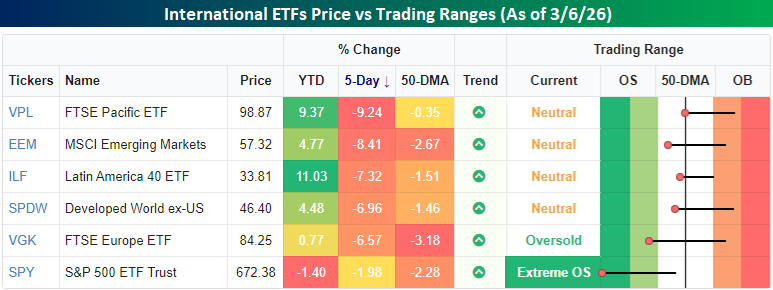

As bad as the US markets have been since the war broke out, it’s peanuts compared to the losses in the rest of the world. Below, we show the performance of various regional ETFs last week. While the S&P 500 was down nearly 2% last week, every other region of the world was down at least 6% and, in most cases, even more. Europe was down 6.6%, emerging markets were down over 8%, and stocks in the Asia Pacific region were down over 9%. As much as higher oil prices are a pain for US consumers and businesses outside of the Energy sector, other areas of the world are much more dependent on external sources for energy than the US.

In terms of the US vs. the rest of the world trade, the Developed World Ex US ETF was down nearly 7%, or five percentage points more than the S&P 500, in a week! As much as the US outperformed the rest of the world last week, it’s still significantly underperforming the rest of the world on a YTD basis (-1.4% vs +4.5%).

With the S&P 500 on pace to gap down 1% at the open for the fourth time in six days today, volatility has been on the rise, and the VIX is trading above 30 for the first time since last spring during the tariff-tantrum. Back then, though, the VIX briefly breached 60 before pulling back. So far during the current war, the highest the VIX has traded is 35.3. Last week may seem like a rough period for the markets, but relative to other points in just the last year, it could be a lot worse. The longer this conflict lasts and oil supplies remain disrupted, the more likely it is that conditions will worsen.