May 12, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“And so castles made of sand fall into the sea, eventually.” – Jimi Hendrix

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As prospects for a peace deal in Iran dwindle, traders are reducing risk as crude oil prices push higher and equity futures decline. The S&P 500 is on pace to open down 0.34%, while the Nasdaq is down more than twice that 0.71% as the hottest area of the markets experiences the most profit-taking. Crude oil prices are up over 4% as WTI trades back above $100 and Brent pushes towards $108. Gold prices are down about 0.5%, and Bitcoin is down 1.7% but still above $80K.

Lower odds of a peace deal have a more negative impact on Europe, and the STOXX 600 is down 0.70%, with Germany down over 1%. In Asia, the picture was mixed. The Nikkei rallied 0.5%, but Hong Kong, China, and South Korea all traded lower, with the latter falling the most (-2.3%). The decline in South Korea followed a proposal from a policymaker suggesting the country should pay citizens a ‘dividend’ using taxes on profits from AI-related industries.

Small business sentiment was released earlier this morning, and while the headline index was weaker than expected, it showed a modest increase relative to last month. The big report of the day, though, will be April’s CPI at 8:30. Economists expect the headline index to increase 0.6% with the core reading expected to jump 0.3%. While the market expects sizable increases to both indices, we would note that there hasn’t been a report yet this year where headline or core CPI was higher than expected.

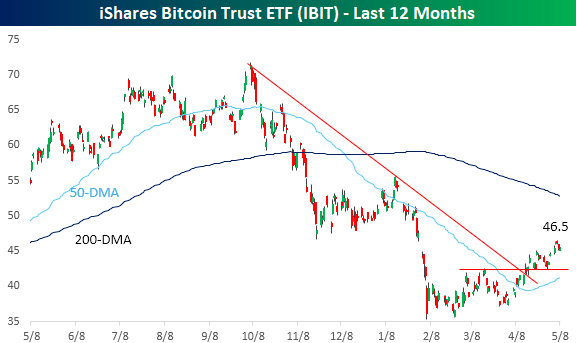

With everyone seemingly focused on Iran and semiconductors, Bitcoin has quietly carved out what increasingly looks like a bottom and the early stages of what could be an emerging uptrend. Since its intraday low in early February, the OG cryptocurrency has made a series of higher highs and higher lows. In early April, the price broke its downtrend from last year’s high, which also coincided with short-term resistance. Just to get back to even for the year, though, the Bitcoin ETF (IBIT) would need to rally more than 7% from yesterday’s close (8%+ from pre-market levels), and it’s still more than 35% below its 52-week high which would require a rally of 55% to get back to.

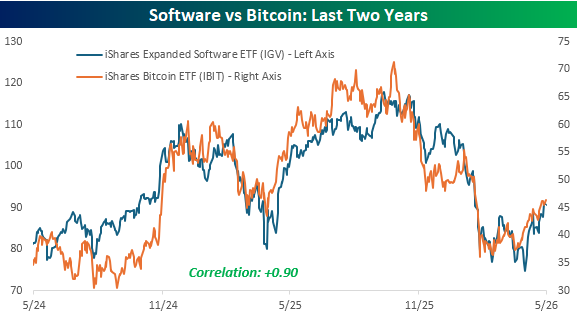

The direction of Bitcoin could be an important tell for one of the most beaten-down groups in the market, as the iShares Software ETF (IGV) has traded practically in lockstep with Bitcoin over the last two years. They’ve had their ups and downs, but IBIT and IGV have one of the closest relationships of any two major non-index ETFs, with a correlation of +0.90.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 11, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The toughest thing about success is that you’ve got to keep on being a success.” – Irving Berlin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures point to a lackluster start to the new week as the S&P 500 and Nasdaq are both indicated to open the week 0.10% lower. Given the move higher in crude oil, though, it could be worse. WTI is trading up over 3% to more than $98 per barrel after the US rejected Iran’s latest peace proposal as a non-starter. The 10-year yield is nearly 3 bps higher but still under 4.4%, while gold is down over 1%, and Bitcoin is fractionally higher.

Overnight in Asia and Europe this morning, it’s been a negative start to the week on the Iran news, but in the US, attention will likely shift from the Middle East to inflation – at least in the short term – with Tuesday’s release of CPI and Wednesday’s PPI.

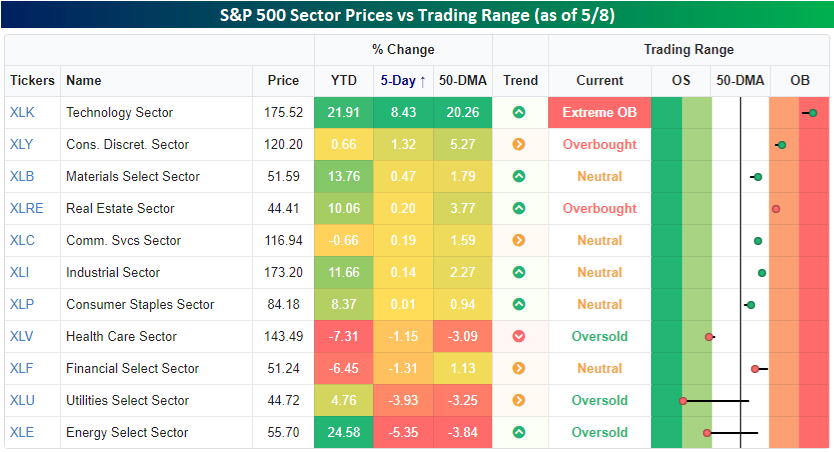

Every week is interesting, but last week’s breadth was a standout. The S&P 500 finished 2.33% higher, but mega caps did most of the heavy lifting as the average stock in the index finished the week higher by just 0.64%. Check out the snapshot below from our Trend Analyzer showing each sector’s performance and where they traded relative to their trading ranges. Again, while the S&P 500 was up over 2%, the only sector that outperformed the index was Technology, and with a gain of 8.43%, it outperformed by a lot! The only other sector that rallied more than 1%, though, was Consumer Discretionary (+1.32%), and no other sector even finished the week higher with a gain of 0.5%.

Not only did most sectors underperform last week, but more sectors were down 1% than up 1%. In fact, there were just as many sectors that finished down by over 3% – Energy and Utilities – as there were that finished up at least 1%!

Where each sector settled out the week relative to its trading range also varied widely. While Technology heads into the new week at ‘extreme’ overbought levels, Utilities is right on the cusp of ‘extreme’ oversold levels, and Energy and Health Care also finished the week at oversold levels.

However weak overall breadth was, a gain is a gain, and the S&P 500, Nasdaq, and Russell 2000 now all have winning streaks of at least six weeks. Six-week winning streaks aren’t that out of the ordinary for any of the three indices on their own, but for all three to have one simultaneously is much less common. Since the Russell 2000 started in 1979, there have only been ten other periods.

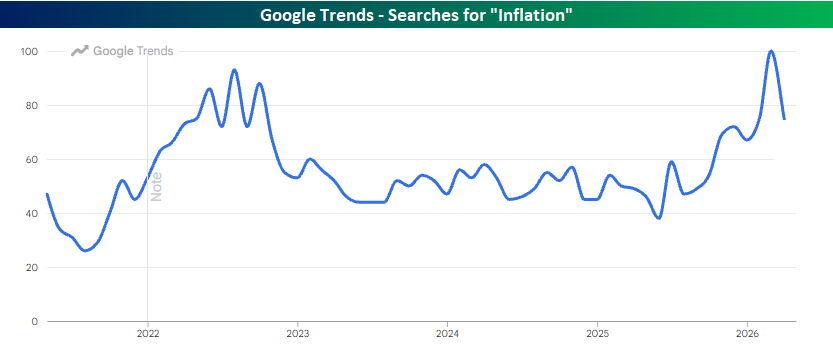

Finally, inflation will be a big topic this week with the release of CPI on Tuesday and PPI on Wednesday. Obviously, the market is expecting big upticks in inflation. What surprised us, though, is the uptick in search activity related to inflation. According to Google Trends, searches for “inflation” during March surpassed the peak levels seen during 2022 when CPI surged as high as 9.1% y/y. For tomorrow’s CPI, economists are only forecasting an increase to 3.7% from 3.4% in April.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 8, 2026

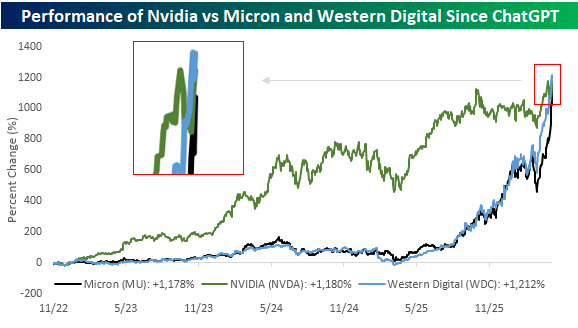

We’ve had a hard time keeping up with the price movements today, but suffice it to say that memory stocks are surging again. The rally in these stocks has gotten so large lately that they’re starting to crowd Nvidia (NVDA) out of the AI winner spotlight. Any mention of AI related to the stock market almost instinctively causes investors to think of NVDA, but when it comes to performance since the launch of ChatGPT, memory stocks, including Micron (MU) and Western Digital (WDC), have caught up.

As of Friday morning, MU’s gain of 1,127% since the launch of ChatGPT isn’t far behind NVDA’s 1,180% gain, while WDC’s gain of 1,212% now surpasses NVDA!

Ever since the AI boom started, NVDA had built a moat comprised of the best GPUs and its CUDA software ecosystem. Memory, meanwhile, was the most commoditized aspect of the entire tech ecosystem. Try telling that to the memory companies now!

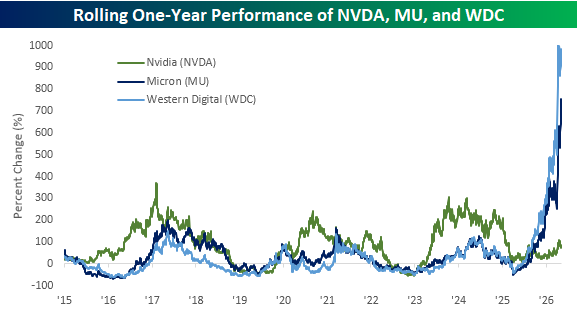

The magnitude of the moves in the memory stocks has been even more surprising. Back in early 2024, when NVDA was sitting on year/year gains of more than 300%, investors couldn’t believe it. Today, stocks like MU and WDC have experienced y/y gains of triple that or more! A key difference between these rallies in the memory stocks and NVDA is that NVDA surged more than 200% on a y/y basis and continued to build on gains of that magnitude for more than a year. At this point, the rally in memory stocks has been more of a concentrated flash (pun intended) in the pan move than an enduring rally. Can it continue? Most investors would probably say no. Once supply catches up to demand, prices will come down quickly, but when was the last time the market didn’t surprise you?

To receive Bespoke’s best and most actionable insights, join our Think BIG mailing list or start a trial to Bespoke Premium or Bespoke All Access today!

May 5, 2026

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!