May 21, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“To have a comeback, you have to have a setback.” – Mr. T

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity futures this morning are lower, but it’s not because of Nvidia (NVDA) earnings. Those are basically shaping up to be a non-event. The culprit this morning is news out of Iran, as the country’s Supreme Leader said that the country will not let its enriched uranium leave the country. That lowers the odds of a peaceful solution, which has oil prices moving higher and equity prices lower. The S&P 500 looks to open down about 0.4% while the Nasdaq is down 0.6%.

As mentioned, crude oil is up about 3%, treasury yields are higher, gold is down about 0.6%, and Bitcoin is fractionally lower.

In Asia, Japan rallied 3.1% while South Korea surged more than 8% as the strike at Samsung was averted. China bucked the positive tone, though, and fell 2%. In Europe, equities are lower across the board with the STOXX 600 down 0.3% as flash PMI indices for the region largely missed expectations.

It’s been a busy morning for data already in the US, and the results have been mixed. Jobless claims were basically in line with forecasts, the Philly Fed for May missed expectations, while Building Permits and Housing Starts came in better than expected.

For all the focus the media puts on Nvidia (NVDA) earnings, the stock is poised to gap up 0.52% today as the market rates the report a snoozer. To put that in perspective, shares of Walmart (WMT) are priced to gap down 2.4% at the open. Today’s moves continue a trend where a relatively ‘boring’ stock like WMT has had a more volatile initial reaction to earnings than NVDA. Including today’s reaction, shares of WMT have had a larger gap (in terms of magnitude) than NVDA for six of the last eight quarters. While NVDA’s average gap on earnings reaction days in the last eight quarters has been 2.6%, WMT’s average gap has been +/-3.6%.

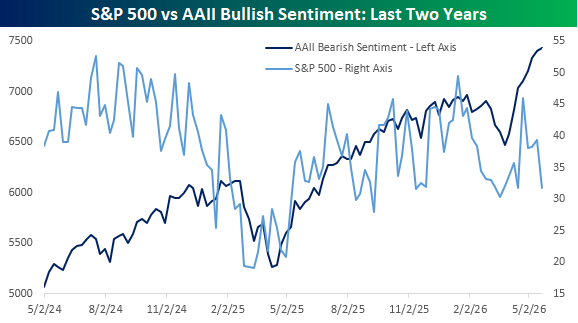

The S&P 500 closed within 0.2% of a 52-week high yesterday, so you would expect investors to feel more optimistic, but the latest sentiment survey from the American Association of Individual Investors (AAII) showed the opposite. In this week’s survey, bullish sentiment declined from 39.3% down to 31.7% while bearish sentiment spiked up to 43.6% for a bull-bear spread of -11.9. Historically, when the S&P 500 was within 1% of a 52-week high, the bull-bear spread was positive 14.6!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 20, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Software is eating the world, but AI is going to eat software.” – Jensen Huang, May 2017

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures have been moving higher all morning, and both the S&P 500 and Nasdaq are indicated to open firmly higher. Treasury yields are modestly lower, with the 10-year yield still at 4.65%, while crude oil falls over 2% to $101.80. Gold is basically flat, and Bitcoin is up 1% to $77,500.

Overnight, Asia was lower across the board with the Nikkei down 1.2%, while other countries in the region were down by smaller amounts. In Europe, the tone has been more positive with the STOXX 600 up 0.4%, led higher by a 0.7% gain in France. The gains have been fueled by reports that the EU has reached a trade agreement with the US to sidestep additional tariffs.

There’s no data on the calendar today, but we will hear from a few Fed speakers before the main event after the close when Nvidia (NVDA) reports results. While the company’s embrace of AI has been a major contributor to the stock’s rally, we were struck by the quote above regarding AI and software. AI’s impact on software may have only been realized by the market in the last six months or so, but Jensen Huang was warning of its impact all the way back in 2017!

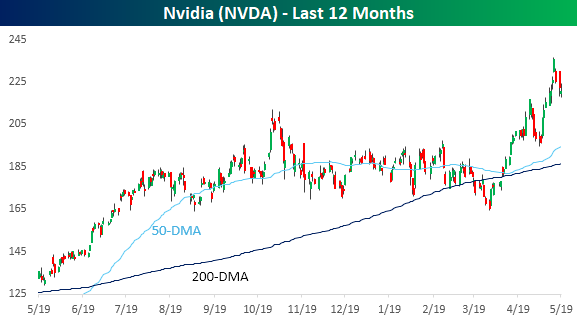

Just given its roughly 7.5% weight in the S&P 500, how NVDA reacts to earnings will have a material impact on the market’s performance tomorrow. NVDA has been on a roll heading into the report as the stock rallied more than 33% off its March low and closed yesterday more than 11% above its 50-day moving average (DMA).

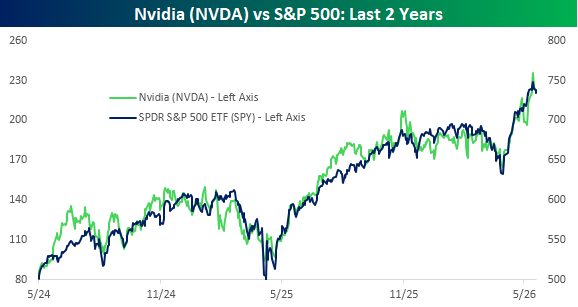

You’ve probably heard people saying, “as goes Nvidia, so goes the market,” and while the magnitude of the stock’s move has been larger than the S&P 500, the patterns of the two over the last two years have been remarkably similar.

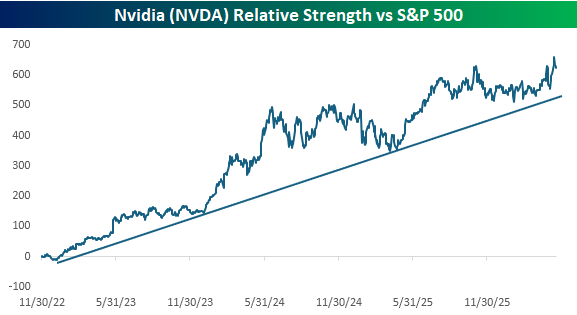

Since the launch of ChatGPT, NVDA’s relative strength versus the S&P 500 has followed a steady upward trend with periods of sharp outperformance followed by periods of consolidation. After trading sideways versus the market for nearly a year, since the March low, the stock appears to be attempting a new leg of outperformance. How the stock reacts to today’s earnings report could go a long way in determining if the latest attempt is successful.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 19, 2026

This content is for members only

May 19, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future starts today, not tomorrow.” – Pope John Paul II

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures have been losing steam as we approach the opening bell, with the biggest recent winners leading the losses. S&P 500 futures are indicated to open nearly 0.5% lower, while the Nasdaq is poised to gap down 0.75%. Treasuries aren’t doing much this morning as the 10-year yield is modestly lower but still above 4.6%. Crude oil is little changed but elevated as the Middle East is on edge over whether the US will launch a new round of attacks on Iran. Gold and Bitcoin are both fractionally lower.

In Asia, it was a mixed session with the Nikkei down 0.5% following a modestly stronger than expected GDP report, while China was up nearly 1%. With AI-related stocks coming under pressure yesterday, South Korea fell 3.3%.

With tech and AI-related stocks leading the selling pressure, European stocks are much more immune, and the STOXX 600 is bucking the trend of weakness with a gain of 0.8%. Germany is leading the way higher with a gain of 1.4%, while Italy lags with just a marginal gain.

In the US today, it’s a quiet day for data with Pending Home Sales at 10 AM. On a housing-related note, though, shares of Home Depot (HD) are trading marginally lower after reporting earnings this morning. Management noted that while the consumer continues to “defer their spending on larger projects…consistent with what they’ve told us the last few years,” they remain engaged.

Divergent market breadth usually gets the most attention when the S&P 500 trades higher, but the net number of stocks trading higher on the day is negative. Yesterday was the opposite, where the S&P 500 traded lower, but most stocks in the index finished the day higher. At the sector level, yesterday was also net positive as seven sectors traded higher while just four traded lower. With Technology being one of those sectors that traded lower, though, it dragged the entire market into the red with it.

For all the talk recently about how narrow breadth has been, the YTD picture of sector performance is also surprisingly positive. While the S&P 500 is 8.1% higher YTD, seven sectors have outperformed the index on a YTD basis, while just four have declined.

Where the big breadth divergence has occurred is since the low on 3/30. In the seven weeks since then, the S&P 500 is up 16.7%, but just two sectors – Technology and Communication Services – have outperformed. What really stands out is how many sectors have outperformed the S&P 500 by A LOT since 3/30. As shown in the chart, besides Technology and Communication Services, the only other sector that is even close to performing in line with the index is Consumer Discretionary.

Comparing the performance of the market cap and equalweight S&P 500 so far this year, while the market cap-weighted S&P 500 has outperformed, it’s not as though the divergence has been all that wide. While there have been times throughout the year when one version has significantly outperformed the other, in the bigger picture, they have largely cancelled each other out.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 18, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future starts today, not tomorrow.” – Pope John Paul II

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last week’s Trump-Xi summit, which failed to produce any meaningful results, coupled with data suggesting inflationary pressures in the economy, has left stocks facing an uphill battle. That pressure has continued into the new week. S&P 500 futures were firmly lower but have rebounded on reports from Iran that the US will offer a temporary waiver on Iranian oil sanctions. Both the S&P 500 and Nasdaq were indicated to gap down by about 0.5% at the open, but are now just modestly negative, while the 10-year yield is fractionally lower. Crude oil prices are modestly higher, and gold and Bitcoin are lower, with the latter trading back down below 77K.

In Asia, it was a mixed session with Japan and Hong Kong both down 1% while South Korea had a fractional gain of 0.3%. Economic data in China disappointed with April Retail Sales rising just 0.2% while Industrial Production missed forecasts by close to two full percentage points (4.1% vs 6.0%).

In Europe, the STOXX 600 is down 0.4% with Italy down close to 2% after reporting a smaller-than-expected March trade surplus. The UK is trading 0.3% higher as reports suggest PM Starmer is planning to step down.

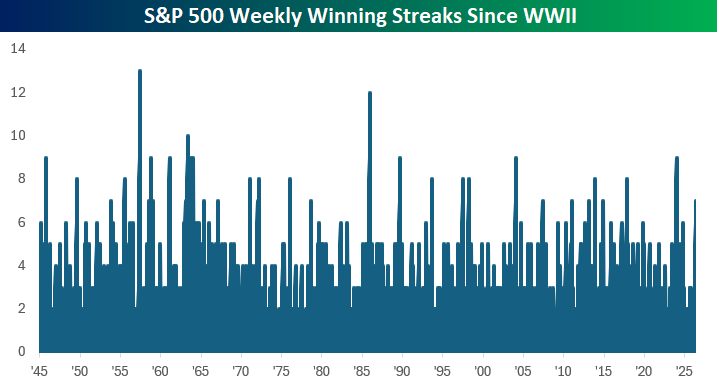

Last week ended on a down note with the S&P 500 declining through the last two hours of the trading session to finish down near the lows of the day. It was a close call at the end of the day on Friday, but the S&P 500 managed to clock its seventh straight week of gains. That’s the longest winning streak since a 9-week streak of gains in December 2023 and the 34th streak of at least seven weeks since WWII.

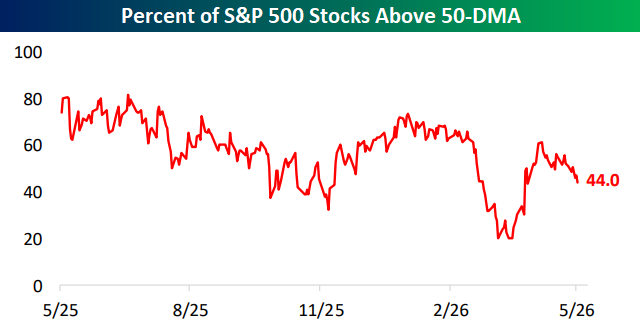

While the S&P 500 may have finished last week higher, breadth remains weak. As of Friday’s close, just 44% of stocks in the S&P 500 were trading above their 50-day moving average, which is hardly the type of reading you would expect to see with a market right near record highs. After a sharp rebound off the April lows, the percentage of stocks above their 50-DMA has been steadily declining for a few weeks now, even as the index has continued higher.

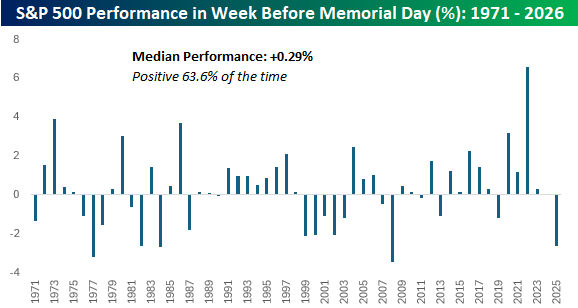

It doesn’t officially start for another month, but the unofficial start to summer kicks off this weekend, just after the unofficial end to earnings season on Thursday, when Walmart (WMT) reports. In the week leading up to the summer season, stocks have tended to have a modestly positive return. Since 1971, when the last Monday of May became the official observance of Memorial Day, the S&P 500’s median performance during the week was a gain of 0.29% with positive returns just under two-thirds of the time. That said, last year’s decline of 2.6% leading up to Memorial Day weekend was the worst pre-holiday performance for the S&P 500 since 2007, and the fifth worst since 1971. Who wants a hot dog with their burger!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.