See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The future starts today, not tomorrow.” – Pope John Paul II

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last week’s Trump-Xi summit, which failed to produce any meaningful results, coupled with data suggesting inflationary pressures in the economy, has left stocks facing an uphill battle. That pressure has continued into the new week. S&P 500 futures were firmly lower but have rebounded on reports from Iran that the US will offer a temporary waiver on Iranian oil sanctions. Both the S&P 500 and Nasdaq were indicated to gap down by about 0.5% at the open, but are now just modestly negative, while the 10-year yield is fractionally lower. Crude oil prices are modestly higher, and gold and Bitcoin are lower, with the latter trading back down below 77K.

In Asia, it was a mixed session with Japan and Hong Kong both down 1% while South Korea had a fractional gain of 0.3%. Economic data in China disappointed with April Retail Sales rising just 0.2% while Industrial Production missed forecasts by close to two full percentage points (4.1% vs 6.0%).

In Europe, the STOXX 600 is down 0.4% with Italy down close to 2% after reporting a smaller-than-expected March trade surplus. The UK is trading 0.3% higher as reports suggest PM Starmer is planning to step down.

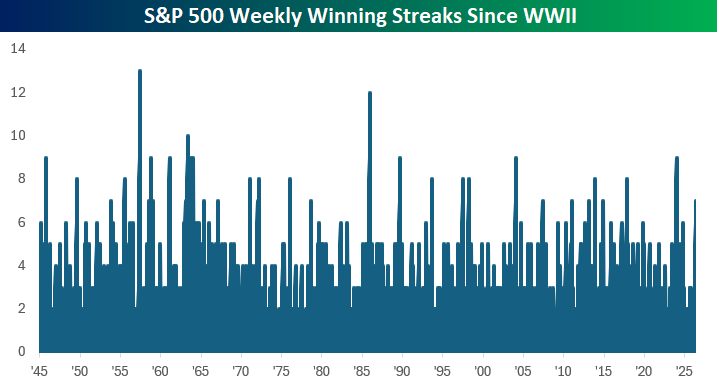

Last week ended on a down note with the S&P 500 declining through the last two hours of the trading session to finish down near the lows of the day. It was a close call at the end of the day on Friday, but the S&P 500 managed to clock its seventh straight week of gains. That’s the longest winning streak since a 9-week streak of gains in December 2023 and the 34th streak of at least seven weeks since WWII.

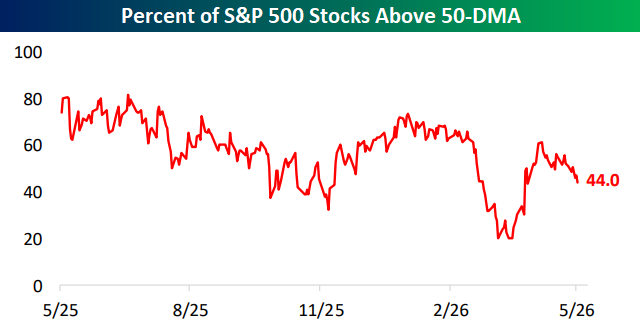

While the S&P 500 may have finished last week higher, breadth remains weak. As of Friday’s close, just 44% of stocks in the S&P 500 were trading above their 50-day moving average, which is hardly the type of reading you would expect to see with a market right near record highs. After a sharp rebound off the April lows, the percentage of stocks above their 50-DMA has been steadily declining for a few weeks now, even as the index has continued higher.

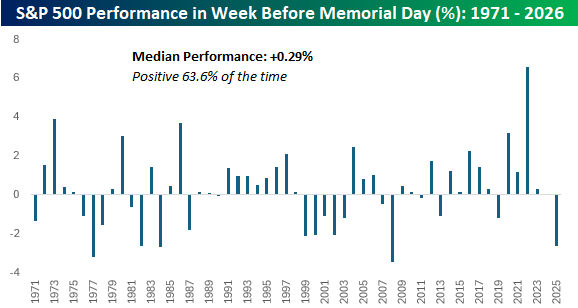

It doesn’t officially start for another month, but the unofficial start to summer kicks off this weekend, just after the unofficial end to earnings season on Thursday, when Walmart (WMT) reports. In the week leading up to the summer season, stocks have tended to have a modestly positive return. Since 1971, when the last Monday of May became the official observance of Memorial Day, the S&P 500’s median performance during the week was a gain of 0.29% with positive returns just under two-thirds of the time. That said, last year’s decline of 2.6% leading up to Memorial Day weekend was the worst pre-holiday performance for the S&P 500 since 2007, and the fifth worst since 1971. Who wants a hot dog with their burger!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.