May 29, 2026

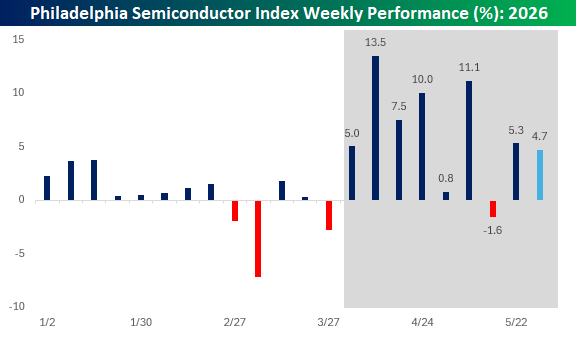

The Philadelphia Semiconductor Index (SOX) is on pace for a gain of just under 5% this week, which by any measure should be considered a great week. Be honest, though, if you hold any of these stocks in your account, have you looked at some of their performances this week and thought to yourself, “Is that it?”

Stocks like Marvell (MRVL), Applied Materials (AMAT), and Taiwan Semi (TSM) are up between 3% and 4% this week, but after gaining anywhere from 40% to 140% YTD, the gains this week seem ho-hum.

A look at weekly SOX performance since the March low illustrates the trend. Yes, the SOX is up 4.7% this week, but relative to recent history, it ranks as the third-worst weekly performance in the last nine. Sure, this week may not look like much compared to the last two months, but the last nine weeks have been a historic run of strength for the sector. As a case in point, if it were any other week before March 30th, it would have been the best week of the year!

After such an incredible run like the last nine weeks for the SOX, it’s easy to get jaded and expect the recent trend to become the norm. It won’t. Just like the Knicks will lose again at some point (hopefully not until next season), the SOX won’t keep going up. Eventually, you’ll look back on this stretch with nostalgia, so soak it in while it lasts, even if it is “only a 4.7%” gain.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

May 29, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In a crisis, be aware of the danger–but recognize the opportunity.” – John F. Kennedy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher this morning following a mostly positive session in Asia, where South Korea rallied 3.6% to take its weekly gain to 8%. The Nikkei also rallied 2.5% for a weekly gain of nearly 5%. Asia’s positive moves have flowed through to Europe this morning, and the STOXX 600 is up 0.6%, led higher by Spain, Italy, and France.

Outside of equities, treasury yields and crude oil are modestly lower on reports that the Iran-US ceasefire will be extended, and gold is bouncing after briefly trading below its 200-DMA yesterday.

An AI compute deal between Anthropic, Alphabet (GOOGL), Broadcom (AVGO), Apollo (APO), and Blackstone (BX) was reported on by Bloomberg last night. The deal has a lot of moving parts to it, and raises concerns over complex transactions and whether it’s just a lot of smoke and mirrors. We broke it all down in the commentary section of today’s Morning Lineup and explained why it’s nothing like the transactions that took place leading up to the Financial Crisis, so make sure to check that out.

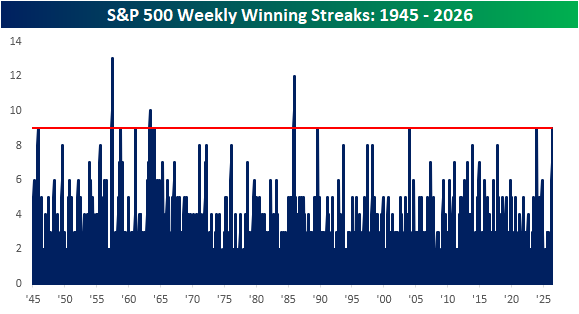

In our experience, we’ve seen enough to know never count anything out, but with the S&P 500 up over 1% already this week, it’s looking likely that the S&P 500 will finish higher this week, extending its weekly streak of gains to nine. The last time the S&P 500 traded higher for nine straight weeks was in December 2023, and the last time there was a longer streak of weekly gains was way back in 1985!

The chart below shows S&P 500 winning streaks in the post-WWII period, and while there have been eleven other nine-week streaks, only four made it to a tenth week or longer. In 1985, the S&P 500 went 12 straight weeks without a decline, and in 1957, the index went 13 weeks, or 3 months, without a weekly decline.

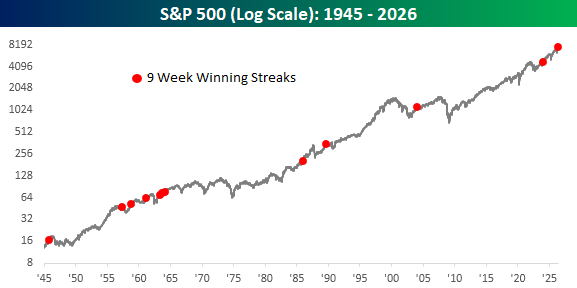

The chart below shows each prior streak on a long-term chart of the S&P 500. Besides the fact that none of these prior periods occurred right near a major top in the market, it’s also interesting to note that they didn’t really occur early on in bull markets coming out of extended bears.

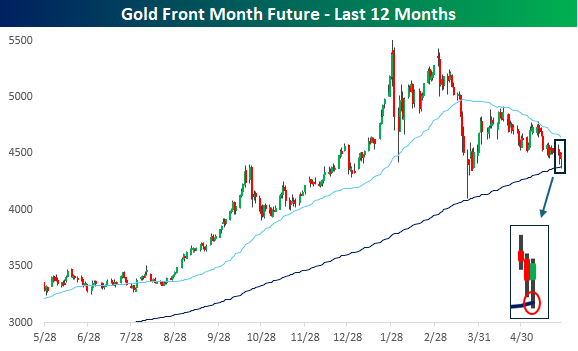

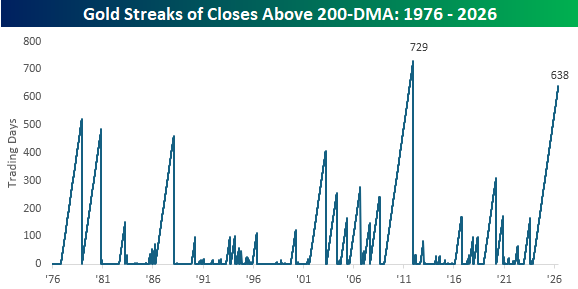

While the S&P 500 keeps chugging along, gold prices have been under pressure for months now, which is a stark contrast to earlier this year when the metal could do no wrong. From the peak in late January, gold prices briefly dropped into bear market territory (on an intraday basis) before rallying intraday. In the process of that decline, gold prices also briefly dipped below the 200-day moving average (DMA) for the first time in 2.5 years.

While the streak of trading without a breach of the 200-DMA on an intraday basis ended yesterday, the streak of closes above that level remains intact, and at 638 trading days, it ranks as the second-longest streak on record, trailing only a 729 trading day streak that ended in December 2011. In order for the current streak to break the record, gold would have to stay above its 200-DMA through the summer months and into late October, but it has been an impressive streak.

The decline in gold since its January high, however, should serve as an important reminder that the tide on a trade that can seemingly do no wrong can quickly go out.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 28, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The distance between insanity and genius is measured only by success” – Ian Fleming

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Markets are taking a breather this morning as the US and Iran trade missile and drone strikes. The S&P 500 looks poised to open 0.2% lower, while the Nasdaq is down 0.33%. After a brief excursion below $90, WTI crude oil is back above $90, gold is down over 1%, and the 10-year yield is up 3 bps to 4.51%.

Asian stocks were mostly lower overnight, with the Nikkei down 0.5% and Hong Kong falling 1.3%. The Shanghai Composite bucked the trend, finishing with a marginal gain, but even South Korea finished the session lower, falling 0.5%. South Korea down? Outside of the rising tensions between the US and Iran, there was no obvious catalyst for the declines in the region.

In Europe, events in the Middle East have also weighed on equities. The STOXX 600 is down close to 1%. Led lower by the UK, while Italy bucks the trend with a gain. Hawkish comments from the ECB’s Chief Economist also haven’t helped.

In the US today, there’s a monster slate of data on the calendar with Personal Income, Personal Spending, PCE, Jobless Claims, Durable Goods, and GDP all at 8:30, followed by New Homes Sales at 10 AM, as well as Energy inventories at 10:30 and 12:00.

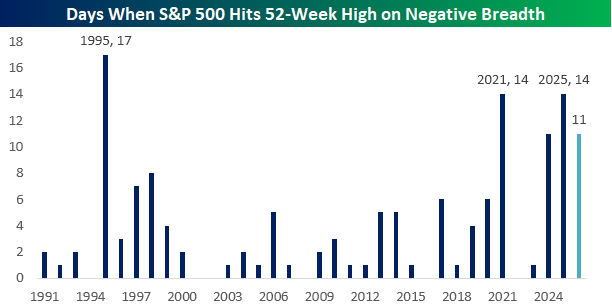

Yesterday was another one of those days when the S&P 500 hit a 52-week high, but breadth was negative. So far this year, these types of daily divergences have occurred 11 times, and if that brings back memories of the late 1990s, it shouldn’t.

As shown in the chart below, we’re not even fully five months into the year, but this year already ranks tied for fourth in the number of days when the S&P 500 closed at a 52-week high but breadth was negative. The only years with more occurrences were 1995 (17), 2021, and 2025, with 14. If you look at the late 1990s, though, in 1998 it happened only eight times all year, in 1999 there were only four occurrences, and in 2000, it only happened twice.

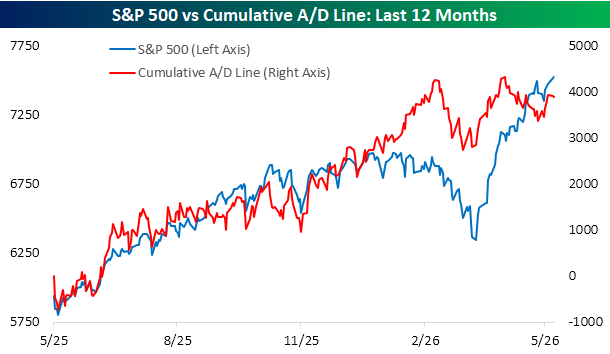

Regarding breadth, the S&P 500’s cumulative advance/decline line continues to diverge from price. On 4/20, the cumulative A/D line made a marginal new high, but ever since then, it’s been biased to the downside, even as the S&P 500 has rallied close to 6%.

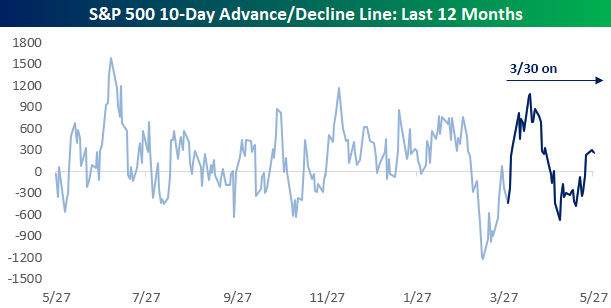

At least there have been some signs that breadth is modestly improving. The chart below shows the S&P 500’s 10-day A/D line over the last year, with the period from 3/30 shown in dark blue. While breadth was positive in the early days of the rally, from late April through just before Memorial Day weekend, it was negative before moving modestly back into positive territory this week. Breadth could still use a lot of improvement, but you have to start somewhere!

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

May 27, 2026

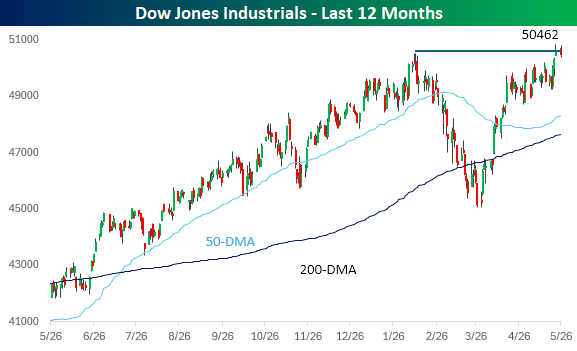

Last week, the Dow finally caught up to the rest of the major US indices in surpassing its pre-Iran war highs. Since that move to new highs, the oldest US index has been moving sideways for the last couple of days.

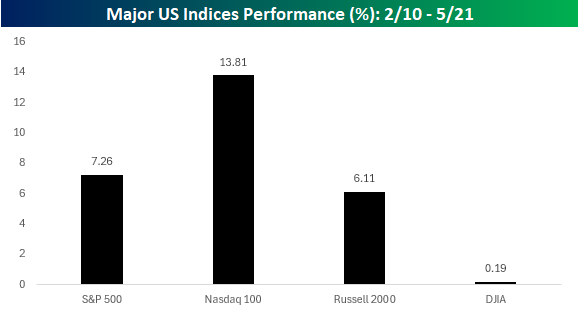

A look at the performance of major US indices from 2/10 through 5/21 – the period the Dow went between highs – illustrates how much the index has lagged its peer indices. While the DJIA rallied just 0.19% during that span, every other major US index was up at least 6%, with the Nasdaq 100 blowing them all out of the water, gaining nearly 14%.

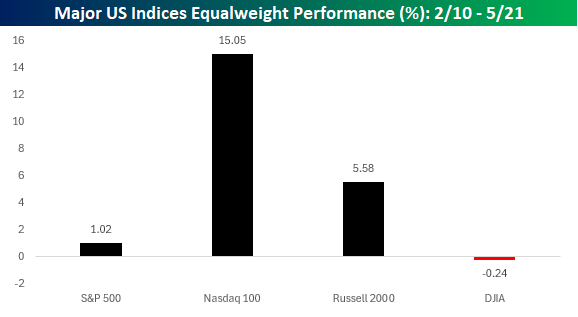

While the Dow has lagged its peer indices, on an equal-weighted basis where each component’s performance is treated equally, the Dow’s underperformance doesn’t look quite as bad, at least relative to the S&P 500. As shown in the chart below, while the 30 Dow components were down an average of 0.24% from 2/10 through 5/21, the average S&P 500 component was up just barely 1%. The average Russell 2000 component, however, was still up close to 6%, while the average performance of the stocks in the Nasdaq 100 is even higher than the index’s performance.

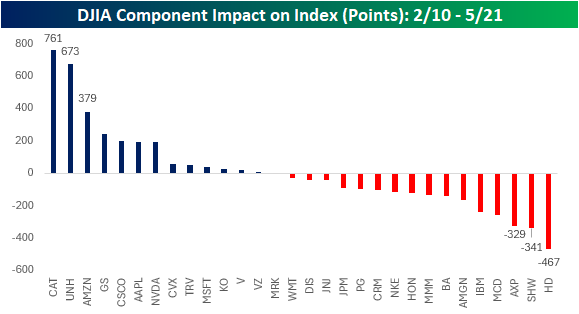

Turning back to the Dow, breadth in the index from 2/10 through 5/21 was skewed to the downside. The chart below shows each component’s impact on the index in terms of points during that period. Caterpillar (CAT) has had the biggest positive impact, responsible for 761 upside points, followed by UnitedHealth (UNH) at 673 points. Trailing way behind in third place, Amazon.com (AMZN) has added 379 points to the index’s performance.

On the downside, Home Depot (HD) and Sherwin-Williams (SHW) have had a combined downside impact of just over 800 points, illustrating housing market weakness. Pointswise, there wasn’t much in the way of train wrecks at the individual stock level, but just a lot more malaise than clear sailing ahead.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

May 27, 2026

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Every victory is only the price of admission to a more difficult problem” – Henry Kissinger

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

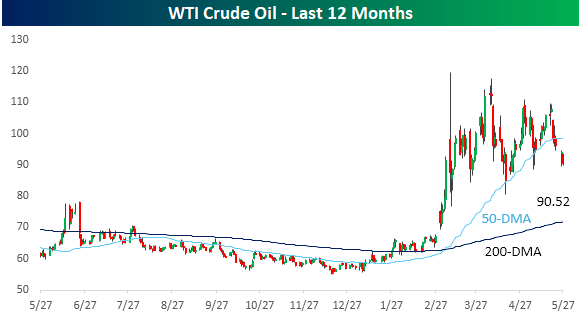

S&P 500 futures are modestly higher (+0.27%), while Nasdaq leads (+0.79%) as memory stocks surge again in pre-market trading. Crude oil is down over 4%, right around $90 per barrel, on hopes (again) of a resolution to the war in Iran and the closure of the Strait of Hormuz. The 10-year yield is down 3 bps to 4.46%, and gold is down another 1.2% to $4,450 per ounce.

It’s a quiet economic calendar this morning, with Richmond Fed the only report on the calendar, while several Fed officials are scheduled to speak. In Asia and Europe, markets were mixed, and the STOXX 600 is currently up 0.2%

As mentioned above, WTI crude briefly dipped below $90 per barrel this morning and now trades just above that level. Prices have been moving in an increasingly narrow range as the markets await a resolution to the war in Iran and the closure of the Strait of Hormuz. US markets have already rallied so much above their pre-war levels, so it’s hard to imagine seeing the US market get a major lift unless prices see a major decline from here. However, if prices continue to drift lower, we would expect to see a broadening of the rally, perhaps even at the expense of the mega caps.

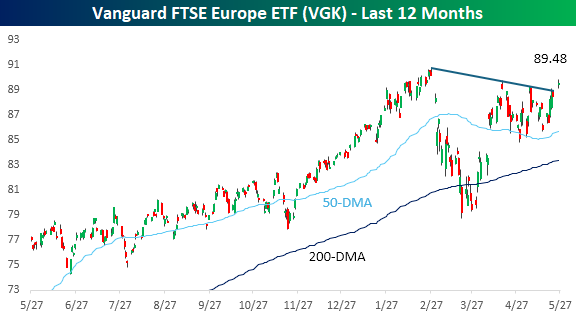

One area of the world more leveraged to oil prices is Europe. As shown below, the FTSE Europe ETF (VGK) has yet to take out its high from earlier in the year, but the drop in oil prices this morning has it getting closer. With this morning’s rally, the ETF is also breaking its downtrend from its earlier peak, leaving one less roadblock to clear on the road to new highs.

On a final note, here we go again. Whenever a new trend emerges in the market, you always find irrelevant companies looking to exploit the wave of euphoria by ‘rebranding’ their businesses to capitalize on the wave of investor interest. In the late 1990s, we saw it with dot-com companies. Then, about 10 years ago, penny stocks started adding crypto to their name in hopes of getting a pop in their share prices.

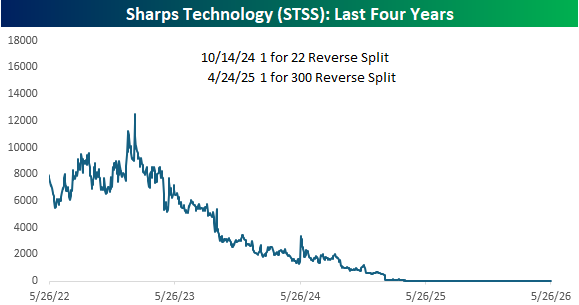

Recently, the “it” rebranding strategy is AI, and the latest example this morning is a company called Sharps Technology (SSTS). For years, Sharps Technology could generously be described as a medical device company in that they made medical syringes. In 2025, the company “pivoted” towards crypto, essentially becoming a Solana treasury company and holding as much as $250 million in the cryptocurrency on its balance sheet.

Judging by the company’s stock price, the pivot to crypto didn’t go as planned, as the price of STSS stock has been in a steady free-fall for several years now. On a reverse-split adjusted basis, the stock has gone from around $16,000 to $1.82 yesterday. It’s been like a memory stock, but only in reverse!

Often, a reverse stock split, even if it’s on a 1-2 basis, is a sign of trouble at a company. STSS has announced two reverse stock splits in the last four years. In October 2024, the company announced a 1 for 22 reverse split, and if that wasn’t bad enough, six months later, it announced a 1 for 300 split. If our math is correct, for every 6,600 shares you had in the summer of 2024, you have one now!

Since the crypto strategy hasn’t quite worked out for Sharps, today the company is going in a new direction and announced a new “vision to build the leading Agentic Finance Platform for the Global South.” The company will change its name to SkyAI and combine its “stablecoin rails with agentic AI to deliver financial access, education, and actionable intelligence to the billions of underbanked users across Africa, Latin America, and Southeast Asia.”

Whenever you see these types of stories, it immediately brings bubble talk into the conversation, and rightfully so. The one silver lining to all of this, at least at this point, is that the announcement has been largely ignored as shares of STSS are up merely six cents in pre-market trading.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.