Bespoke’s Morning Lineup – 6/2/26 – Software: Grabbing the Baton or Flash in the Pan?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Though a good deal is too strange to be believed, nothing is too strange to have happened.” – Thomas Hardy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

While Dow futures point to a 0.45% decline at the open, futures on the S&P 500 and Nasdaq are down much less, indicating a decline of less than 0.2%…for now. Crude oil is down 1.5% but still above $90 per barrel, while the 10-year yield declines 5 bps to 4.43%. Gold prices are up over 1% while Bitcoin is down over 3% and back below $70 as traders increasingly lose patience with the crypto space in search of greener pastures.

It’s a quiet day for economic data today, with the 10 AM JOLTS being the only report on the calendar. We’ll also get May vehicle sales data from the major OEMs throughout the day.

Overnight in Asia, it was a mixed session with the Nikkei down 0.3% while Hong Kong and China both rallied. South Korea’s KOSPI experienced a marginal gain of 0.2%, which, relative to recent moves, seems like a decline!

In Europe, the tone is more positive as the STOXX 600 rallies 0.7%, led higher by Italy and Germany. May CPI for the Eurozone increased 3.2% y/y, which was right in line with expectations, while Core CPI was slightly ahead of consensus forecasts (2.5% vs 2.4%).

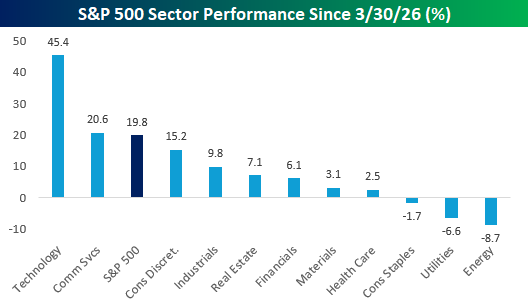

Since the market low at the end of March, the S&P 500 is up just under 20%, but as we are all aware, breadth has been narrow. The lion’s share of the gains has been in the Technology sector, which has rallied over 45%, and the only other sector outperforming the S&P 500 over that time is Communications Services, which is ahead of the index only just barely. The nine other sectors in the S&P 500 are all underperforming the index by a wide margin, including three – Energy, Utilities, and Consumer Staples – which are lower.

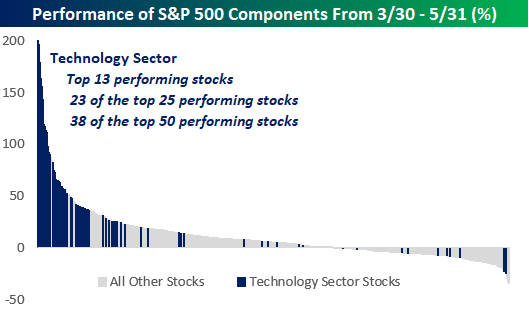

One way to illustrate the dominance of tech since the March low is in the performance of each S&P 500 component. Since the March 30 low, 38 of the top 50 performing stocks are from the Technology sector, including 23 of the top 25 and all of the top 13. It’s been Technology and everyone else.

Of the top performing stocks since 3/30, the tech stocks dominating the list have primarily been – you guessed it – semiconductor stocks, and more specifically memory stocks. Many of these names doubled or tripled in the span of just two months!

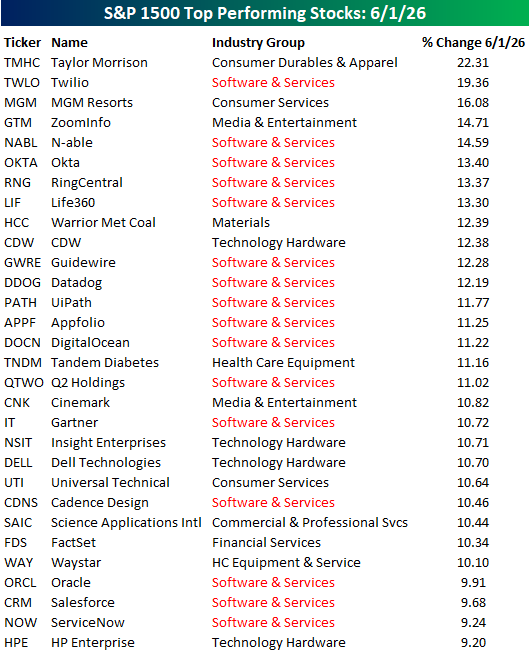

In yesterday’s trading, Technology was once again the top performing sector in the S&P 500 and one of just two sectors to trade higher. In looking at the top performing stocks yesterday, Technology stocks once again dominated the list, but it wasn’t semis. In fact, of the top 30 performing stocks in the S&P 1500 yesterday, not a single semiconductor stock made the list even though Technology was one of only two sectors to trade higher.

As shown in the list below, yesterday’s dominant group within the Technology sector was software stocks. Of the 30 top performing stocks, more than half were from the Software and Services Industry Group.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Matrix of Economic Indicators – 6/1/26

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Bespoke’s Morning Lineup – 6/1/26 – The Year of Semis

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“People talk about AI reducing jobs – complete nonsense. It’s causing more software engineers to be hired.” – Jensen Huang

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a new month, but the market rally continues to roll on. S&P 500 futures are priced to open 0.2% higher, while the Nasdaq is fractionally higher. Treasury yields are unchanged right around 4.45% while crude oil trades back above $90, as there don’t seem to be any signs of an imminent peace deal or ceasefire. Gold prices are down 1.4% but still above $4,500 per ounce, while weakness in Bitcoin persists as prices fall to their lowest level since April.

Asian and European markets have been mixed to kick off the month, as manufacturing PMI indices have started to hit the tape. Here in the US, we’ll get the S&P 500 and ISM reads on the manufacturing sector at 9:45 and 10:00 AM, respectively.

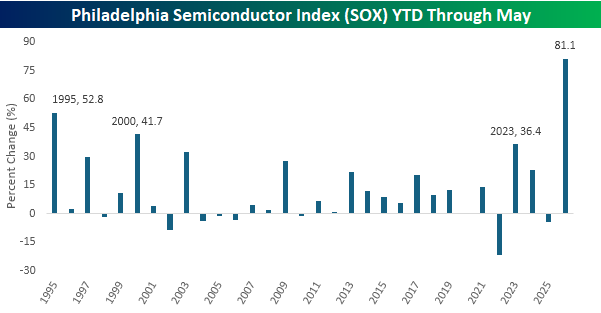

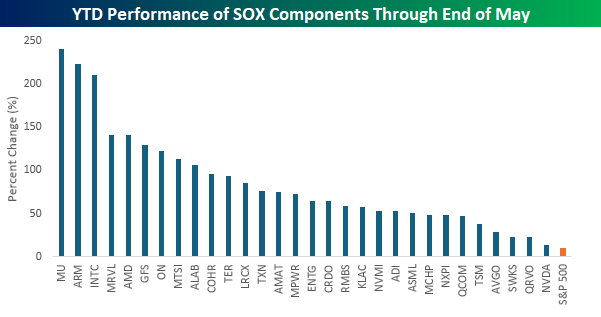

In a speech from Taiwan overnight, Nvidia (NVDA) CEO Jensen Huang called 2026 “the year of agents”. In the evolution of AI, that’s definitely been the case, and the side-effect of that trend in AI is that in the stock market, 2026 has been the year of semiconductors. With a year-to-date gain of 81.1% through the end of May, the Philadelphia Semiconductor Index (SOX) has easily had its best start to a year in its history.

Before 2026, the best start to a year for the SOX was its first full year in 1995, when it rallied 52.8%, or nearly 30 percentage points less than this year’s gain. An 81% gain to start the year is impressive under any circumstances, but when you consider the size of the sector, 81% is almost unbelievable.

Besides having a monster gain at the index level, the rally in semis has been broad. Of the index’s 30 components, eight have more than doubled, including three that are up over 200%. The average gain of all 30 components has been modestly better than the index itself (+87%), indicating that, unlike the S&P 500, it hasn’t been just the biggest stocks in the index driving the gains. Participation has been so broad, in fact, that every stock in the SOX has outperformed the S&P 500 so far this year.

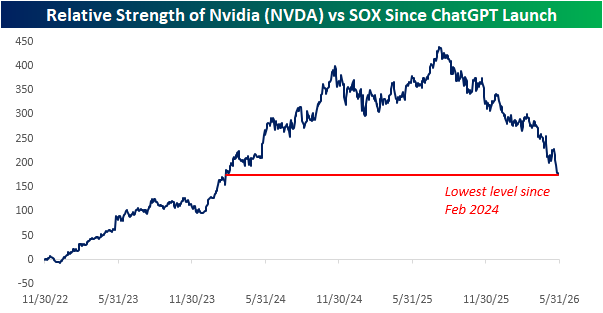

What really stands out about the chart below, though, is NVDA’s performance relative to all the other members of the SOX. With a gain of 13.2% YTD, it’s easily the worst performer in the index and outperforming the S&P 500 by less than three percentage points. So, while all of the major financial outlets are focusing endlessly on last night’s announcements from NVDA out of Taiwan, investors have been looking elsewhere.

Relative to the rest of the semis space, NVDA has been giving up ground for nearly a year now. The chart below shows the stock’s relative strength versus the SOX since the launch of ChatGPT in late 2022. While the stock saw blistering outperformance in the first two years after ChatGPT’s launch, it moved sideways relative to the SOX for nearly a year, and since last August, it has been steadily giving up ground to the index’s other 29 components.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

The Encore Performance

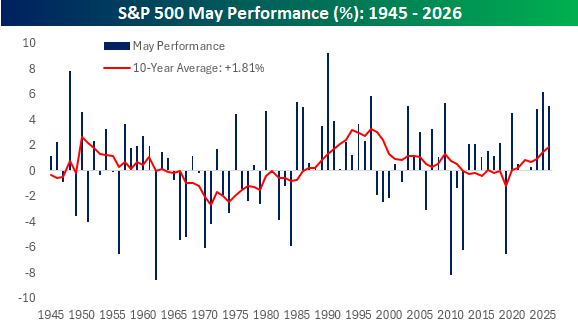

May marks the onset of the “go away” six-month period for US stocks, when they have historically had weaker-than-average returns. In more recent history, though, it has been the encore performance for the October—April period where market returns have historically shined.

With a 5% gain this month, the S&P 500 is on pace for its first-ever “three-peat” of 4%+ gains in May. Not only that, but over the last 14 years, May has only finished in the red once (2019’s -6.58%), driving the 10-year rolling average May return to 1.81%, which is the strongest rolling performance for the month since 1999. Your parents may have once told you that it’s never smart to hang around the bars after last call, but in recent years, staying late has paid off. Now about that hangover the next morning…

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.