Mar 8, 2022

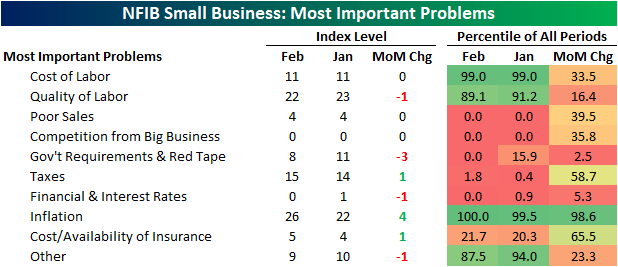

Looking across the range of issues surveyed by the NFIB, labor and inflation remain front and center of what most concerns small businesses. As shown below, the combined percentage of respondents reporting either cost or quality of labor as their most important problem continues to be the most prevalent topic with 33% of firms reporting as such. That is down slightly from 34% in January thanks to the decline in quality of labor. Most other categories fell to or remained at record lows. Such was the case for Poor Sales, Competition from Big Business, Government Requirements and Red Tape, and Financial & Interest Rates.

Last month the percentage of respondents reporting inflation as their biggest problem went unchanged from the December reading of 22%. This month that reading gained another 4 percentage points to cross above a quarter of all respondents for the first time on record going back to 1986. Behind labor concerns (the combined reading of cost and quality of labor), this is the most commonly reported problem, and based on the action in commodities prices over the last couple of weeks, this reading will almost certainly increase again next month.

That means what has usually been the second most important problem on a combined basis recently, government requirement and taxes, dropped in the ranking. In fact, the 3 percentage point decline in government requirements offset the one percentage point increase in taxes to tie the November 2005 reading for the lowest on record. As we have noted in the past, the past few presidential cycles have structurally seen lower readings in these indices when Republicans were in office and vice versa when Democrats have held the presidency. With Biden currently in office, the record low reading is somewhat unusual from this political perspective.

That is not the only category that has fallen to record lows. Poor sales and competition from big business have both fallen dramatically in the past couple of years. Click here to view Bespoke’s premium membership options.

Mar 8, 2022

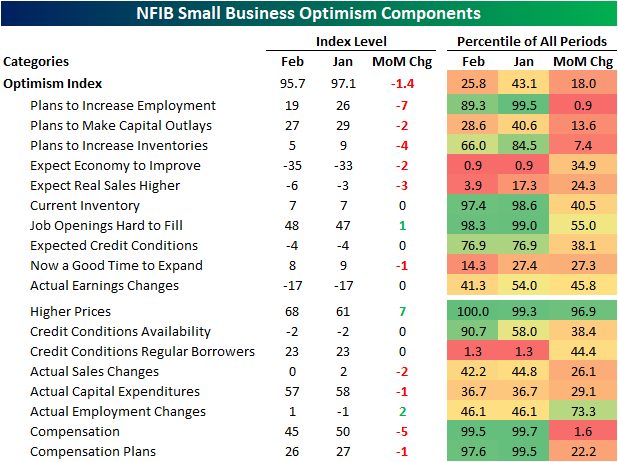

Sentiment on behalf of small businesses fell for the second month in a row in February. At 95.7, the NFIB’s Optimism Index has now dropped to the lowest level since January 2021 and continues to closer to its COVID low and further from its high.

The Optimism Index is now right around the bottom quartile of historical readings after the 1.4 point decline. Given the decline in the headline number, breadth across categories this month was weak with Job Openings Hard to Fill the only index to rise month over month. Despite the increase in Job Openings Hard to Fill, the index for Plans to Increase Employment saw the largest decline of any component.

Employment indices in this month’s report are some of those that remain the most elevated relative to their historical ranges. That being said, they have cooled off recently as we noted earlier in today’s Morning Lineup. Indices like Job Openings Hard to Fill and Compensation and Compensation Plans are all in the top few percentiles of their historical ranges even after coming off their peaks and some even falling significantly month over month in February. Hiring Plans, however, experienced a 7 point decline—ranking in the bottom 1% of all monthly moves—bringing that index out of the top decile of historical readings.

As for other areas of the report, General Business Conditions remain extremely weak falling another 2 points to remain in the bottom one percent of historical readings. Additionally this month, fewer respondents reported that it is a good time to expand, and more expect lower than higher sales on the horizon. While it is not an input to the optimism index, there was a new record high in the percentage of respondents reporting that they are raising prices. Click here to view Bespoke’s premium membership options.

Mar 8, 2022

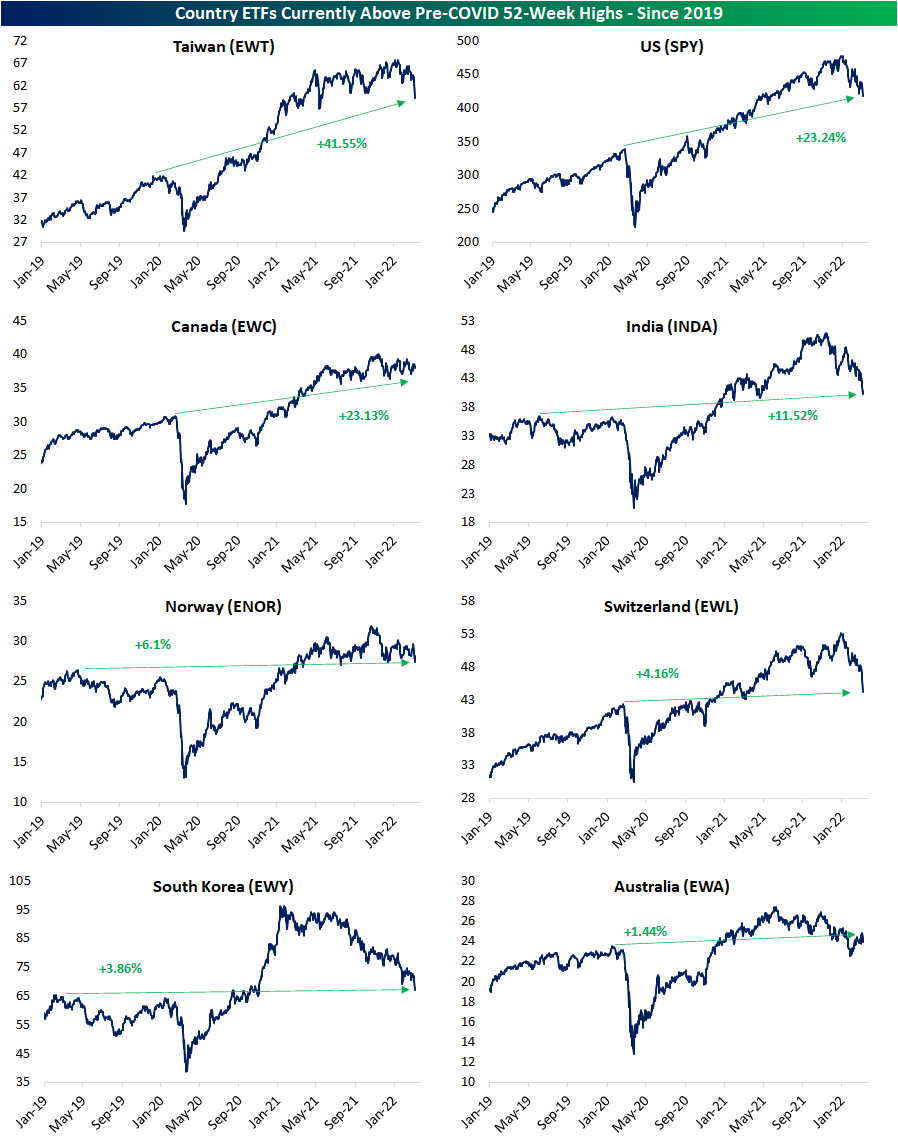

Headed up to the two-year anniversary of the COVID crash low (3/23/20), equities around the globe have been experiencing some of the worst pullbacks since that period. In the table below, we show the country ETFs of the countries tracked in our Global Macro Dashboard as well as their year and month to date performance, performance since each respective 52-week high as of 2/19/20 (the S&P 500 and a handful of other global indices last high before entering bear markets during the COVID crash) and current 52-week high. We also show where they are currently trading with respect to their 50-DMAs.

Given the degree of declines recently, nearly everything is oversold with six countries’ readings now ‘off the chart’ as they trade well over three standard deviations below their 50-DMAs. The average country ETF is also down double digits on both a YTD basis and relative to their respective 52-week highs. Of the countries shown below, only Brazil (EWZ) and South Africa (EZA) are higher YTD with gains of 17.56% and 9.27%, respectively. Russia (RSX), meanwhile, is obviously down the most having been cut by over 75%.

The average country ETF is now down over 20% from its 52-week high, and only four of those 52-week highs have come since the start of 2022 whereas most were set last spring. As for how the current drawdowns have eaten into the post-COVID rallies, below we also show the percent change of these ETFs relative to their 52-week highs as of 2/19/20. In other words, where each ETF is trading with respect to their pre-COVID highs. Currently, there are only 8 country ETFs that remain above their respective pre-COVID highs. Seven others, meanwhile, have now declined more than 20% below their pre-COVID highs. Of course, Russia is once again down the most dramatically from those levels falling more than 75%.

Below we show the charts of those eight countries that are currently still in the green relative to pre-COVID highs. The recent rough patch is not exactly identical for all countries though. Whereas the downtrends for some like Taiwan (EWT) or the US (SPY) are bringing these ETFs to multimonth lows, others like Canada (EWC) and Norway (ENOR) have more or less trended sideways. Since retaking pre-COVID highs, only Australia (EWA) has gone on to recently retest/fall back below those levels which it did in late January. While it would mean much further downside for the likes of EWT, SPY, and EWC, those prior highs could mark one area of tangible support for these other countries. Click here to view Bespoke’s premium membership options.

Mar 7, 2022

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight by showing which stocks led the way lower in today’s session and whether or not recent price action is consistent with bear markets. We then note some feedback effects of elevated oil prices. Next, we review the moves in fixed income markets while also previewing this week’s Treasury sales. We finish with a look at mortgage delinquency data and positioning data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!