The Closer – Twice The Multiple, Less Than Half The Fun – 3/17/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight comparing the macro backdrop now versus the Volcker era. We then show what analysts are projecting for the rest of the year and 2023. We follow with a recap of today’s residential construction numbers and an update of our Five Fed Manufacturing Composite.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 3/17/22

This content is for members onlyBears Come Out of Hibernation in Spite of Rebound

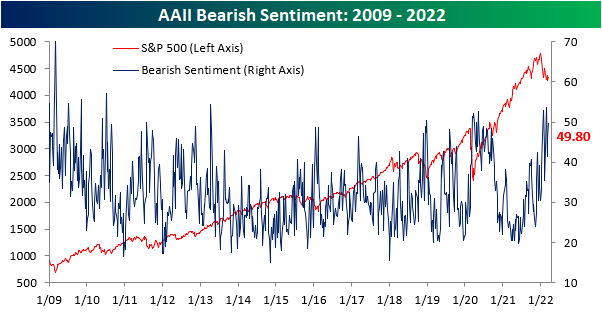

In spite of the S&P 500 gaining back some ground in the past week, sentiment has continued to shift in an increasingly pessimistic direction. For a second week in a row, less than a quarter of respondents to the AAII sentiment survey reported a bullish. At 22.5%, however, current levels are still slightly above the low of 19.2% from one month ago.

Bearish sentiment meanwhile climbed another 4 percentage points with just under half of respondents reporting as such. Albeit elevated, bearish sentiment is not as high as the 50%+ readings reached in January and February. As for another reading on bearish sentiment from the Investors Intelligence survey, bearish sentiment is at the highest level since the March 2020 COVID low.

The bull-bear spread is extremely low at -27.3 but that is not quite as low as those past couple of weeks when over half of respondents reported as being bearish.

Not all of the increase to bears came from bulls. As shown below, neutral sentiment fell from 30.2% down to 27.8%. That is only the lowest level since the end of February. While bullish and bearish sentiment are both over a full standard deviation away from their historical averages, neutral sentiment is much more inline with its own historical average. Whereas all weeks since the start of the survey has seen neutral sentiment average a reading of 31.4%, this week’s reading was only a few percentage points away. Click here to view Bespoke’s premium membership options.

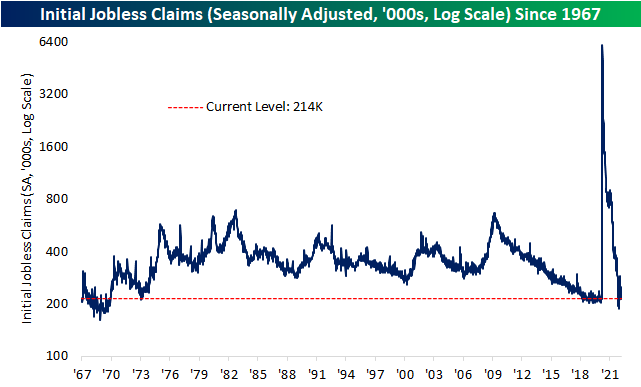

Continuing Claims At the Lowest Level Since 1970

Seasonally adjusted jobless claims continue to ping back and forth within their recent range between 200K and 300K. Still off the sub-200K readings from the end of last year, jobless claims fell from 229K to 214K this week. That is the lowest level since the last week of 2021 when they were 7K lower. Even though there has been no new notable low, the current level is still healthy and consistent with pre-pandemic levels that had not been observed at any other period after the early 1970s.

Jobless claims continue to have seasonal tailwinds at this point of the year and typically do not seasonally bottom until several weeks later. The current week of the year has historically been one of the strongest in terms of consistency of declines in the non-seasonally adjusted number. Since 1967, 92.7% of the time claims have fallen week over week during the current week of the year, and this year was no exception. At 202.9K, it was only slightly above the low of 196K from two weeks ago. That level is also still slightly above the readings for the same week of the year prior to the pandemic (2018 and 2019).

Delayed an additional week making the most recent reading through the first week of March, seasonally adjusted continuing claims fell to a fresh low of 1.419 million. That is the strongest reading on continuing claims since February 1970. Click here to view Bespoke’s premium membership options.