Dipping Dallas

The fifth and final regional manufacturing release came out of the Dallas Fed this morning, capping off the month on a disappointing note. The index fell by more than expected, dropping 5.3 points to 8.7. While lower, that is still several points above December and January levels. The Expectations reading was also lower, setting a 21-month low.

The month over month decline in general business activity came up just shy of the bottom quartile of all readings since the data begins in 2004. In spite of that decline at the headline level, overall breadth was actually largely positive with the number of categories rising month over month doubling the number of categories that fell. With that said, company outlook, shipments, and new orders each saw significant declines. Expectations, on the other hand, had a larger share of categories decline as most of these indices sit lower within their respective historic ranges.

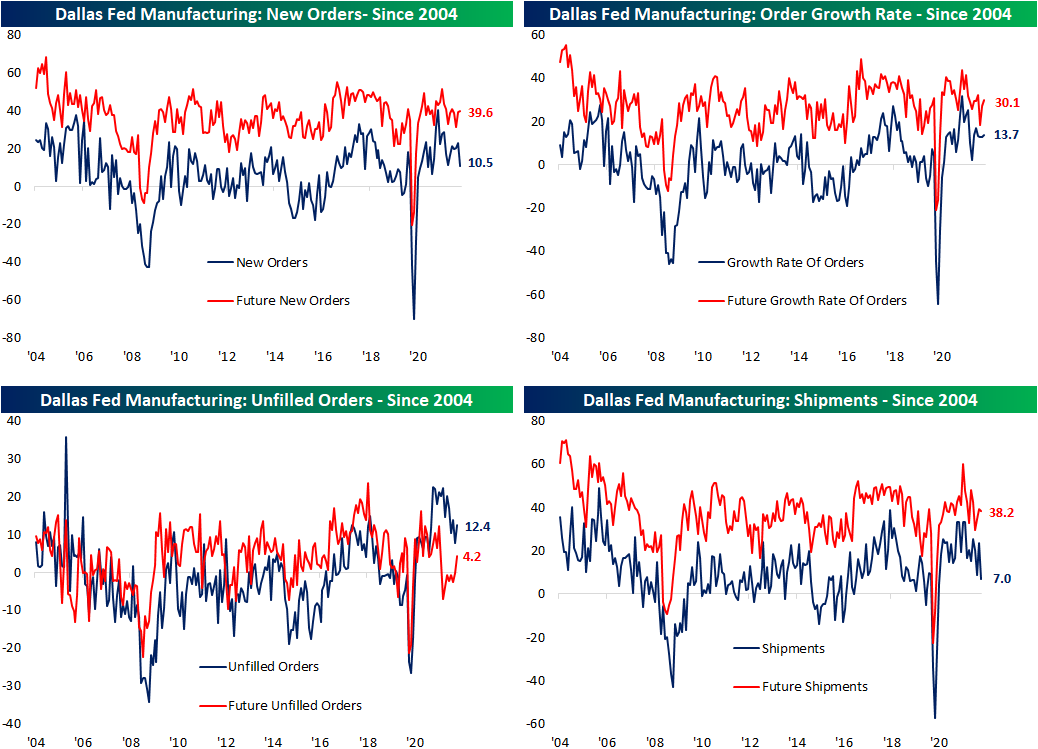

As mentioned above, new orders and shipments experienced two of the most notable declines this month, falling 12.6 and 16.5 points, respectively. New orders is now down to the weakest level since January 2021 while shipments has erased any gain since June 2020. While those were big declines, the positive readings still indicate that the region continues to see growing demand albeit at a slower rate.

Employment metrics were a healthier area of the report showing the region’s firms increased hiring in March at an accelerated rate. Additionally, wages and benefits also rose at a historic rate. The current conditions index for that category set a new record high this month while expectations reversed off of a record. Not only are the region’s firms paying workers more, but they are also increasing capital expenditure. That took out the December high for the strongest reading since last May. That increased spend is also expected to continue as the expectations index hit the highest level in three years. Click here to view Bespoke’s premium membership options.

Daily Sector Snapshot — 3/25/22

This content is for members onlyThe Closer – Peso Push, Distributional Discussion, Roaring Capex – 3/24/22

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin tonight with a look at EMFX performance followed by a rundown of the Federal Reserve’s quarterly update of Distributional Financial Accounts data. We also show the differing performance of investors by generation. We then take a look at quarterly equity market issuance and retirement data, preliminary durable goods figures, and the 10 year TIPS reopening.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Record Readings From The KC Fed

The fourth of five regional Fed manufacturing indices was released this morning from the Kansas City Fed. The 10th district’s Manufacturing Composite hit a new record high in March rising 8 points to 37. Expectations also set a new record climbing 3 points to 41. Those readings indicate the region’s manufacturers have seen a historic rate of growth and expect that to continue over the next six months.

Given the record reading in the headline index, most categories of this month’s report came in at historically elevated readings. Breadth was also impressive with only three categories declining month over month: Number of Employees, Average Workweek, and New Orders for Exports. In spite of those declines, the levels are consistent with healthy growth. Breadth for expectations was more mixed with an equal number of categories rising and falling versus the February report.

Growth in demand only accelerated modestly as the new orders index rose a single point to 33, and order backlogs rose by a more significant 7 points. The ability of the region’s manufacturers to fulfill those orders, meanwhile, was much stronger in March as both shipments and production set new record highs rising 22 and 15 points, respectively. Production expectations also set a new record high.

That higher production also came in spite of supply chain slowdowns. The delivery times index rose back up to the November record high of 55, erasing any of the past few months’ improvements. The expectations index saw the same results in which any recent reversal lower has now been erased as it set another record high.

Similar to delivery times, a huge month-over-month increase in prices paid this month led the index to reverse much of the past year’s decline, though, that was preceded by a large increase in expectations last month. The prices received index has been more rangebound recently but it too ticked higher in March. That is while expectations are rising at a much more rapid rate, setting more all-time highs.

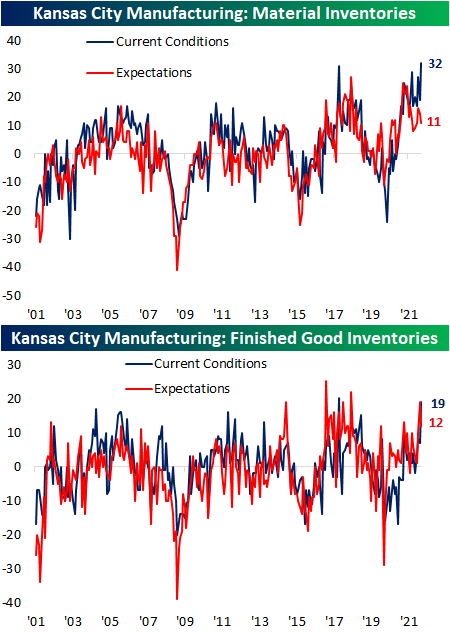

In spite of higher prices paid and supply chain delays, material inventories experienced record builds in March as that index took out the former record from October 2017. Finished good inventories, meanwhile, came up one point shy of its October 2017 record.

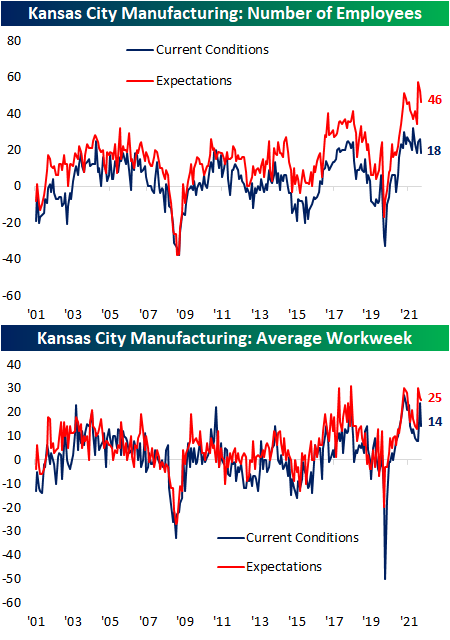

The only notably weak area of the report was employment metrics. Both number of employees and average workweek remain in expansionary territory but pulled back in March for both current conditions and expectations. Click here to view Bespoke’s premium membership options.