May 28, 2026

Log-in here if you’re a member with access to the Closer.

- Even after working off of its lows, the S&P 500 Software and Services industry’s distance from its price targets is in the 10th percentile of all periods since 2003.

- GDP was revised down 0.4%-pt QoQ SAAR as non-residential investment remained the biggest driver of growth.

- Due to a combination of weak hiring, slowing wage growth, and higher inflation, purchasing power has been driven down as real household earnings registered a 4th percentile reading.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

May 27, 2026

Log-in here if you’re a member with access to the Closer.

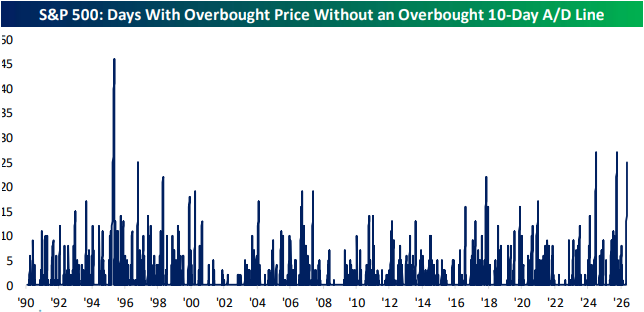

- The S&P 500 has been overbought for 31 days in a row, but the 10-day A/D line hasn’t experienced an overbought reading since April 21st.

- Regional manufacturing surveys had the strongest showing for price indices since the spring of 2022.

- Special questions from regional Federal Reserve bank surveys indicated rising prices and decelerating AI adoption among responding firms.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

May 26, 2026

Log-in here if you’re a member with access to the Closer.

- DRAM prices and GPU rental rates have continued to rise, powering the AI trade.

- AI related stocks have posted consistent gains recently with many of those names reaching new highs.

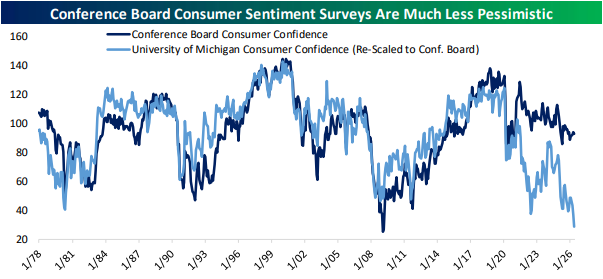

- Separate surveys tracking consumer confidence are showing drastically different results including a record low for UMich and more tempered readings for the Conference Board.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!