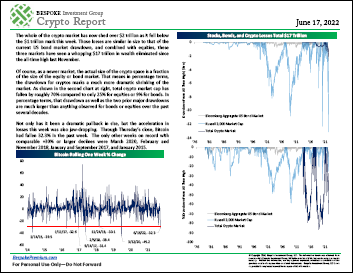

Bespoke’s Crypto Report — 6/17/22

Bespoke’s Crypto Report contains numerous technical, momentum, and sentiment charts for bitcoin, ethereum, and other key cryptos. Page 1 of the report includes our weekly commentary on the space and attempts to identify any new trends that are emerging. The remaining pages include important overbought/oversold levels to watch, charts on historical drawdowns and rallies, seasonality trends, futures positioning data, Google search trend shifts, and more. Our weekly Crypto Report is produced so that followers of the space can more easily stay on top of price action, technicals, seasonality, and sentiment.

Sign up for a monthly or annual subscription to Bespoke Crypto to receive our weekly Crypto Report and anything else we publish related to cryptos. Note: If you’re currently a Bespoke Premium, Bespoke Newsletter, or Bespoke Institutional subscriber, you’ll need to subscribe to Bespoke Crypto as an add-on to receive access. The weekly Crypto Report and any additional crypto analysis is not included with our Premium, Newsletter, or Institutional memberships. You can sign up for Bespoke Crypto and receive our Crypto Report in your inbox weekly using the monthly or annual checkout links below. If you sign up for the annual plan, the first year of access is 50% off!

Bespoke Crypto Access — Monthly Payment Plan ($49/mth)

Bespoke Crypto Access — Annual Payment Plan ($247.50 for the first 12 months, then $495/year in year 2 and beyond)

Bespoke Investment Group, LLC believes all information contained in this service to be accurate, but we do not guarantee its accuracy. None of the information in this service or any opinions expressed constitutes a solicitation of the purchase or sale of any securities, commodities, or cryptocurrencies. This service contains no buy or sell recommendations. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

The Closer – Bear Markets And Recessions: Not Always Together – 6/16/22

Log-in here if you’re a member with access to the Closer.

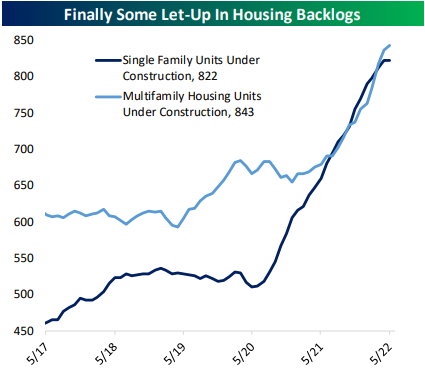

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin by showing the relationships between recessions and bear markets in bonds and equities (page 1). We then take a glance at past times that the S&P 500 has reversed lower by at least 1% after rallying 1% on a Fed day (page 2). Turning over to macro data, we provide an update of our Five Fed Manufacturing Composite (page 3) followed by some notes on today’s housing data (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 6/16/22

This content is for members onlyMore Promise For Supply Chains

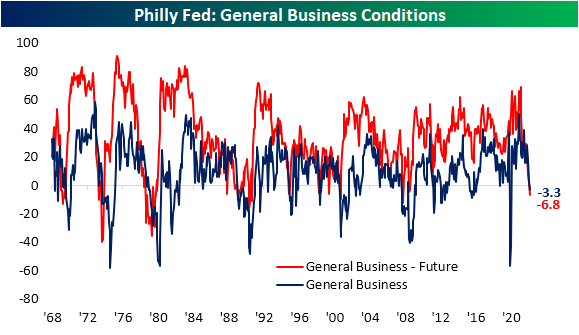

Piggybacking off of another contractionary reading in the Empire Fed survey yesterday, the neighboring Philly Fed’s Manufacturing survey also saw its headline reading print a negative number for June. The index for General Business Conditions has fallen sharply over the past three months, now having shed 30.7 points in that time. This month was the smallest month-over-month drop of those months, though, with the index falling from a barely expansionary reading of 2.6 in May to -3.3. Despite the small drop, that is still the first negative reading since May 2020. As for expectations, this month also saw the index fall into contractionary territory, a first since December 2008.

Whereas the Empire Fed report had some silver linings with pretty mixed breadth, this report saw large and broad declines across nearly all categories. Multiple month-over-month moves ranked in the bottom few percentiles of all monthly changes on record in data going all the way back to 1968. There were also three indices (excluding the headline number) that fell from expansion into contraction.

Following up on a retail sales report yesterday that showed the US consumer has cooled off, regional Fed reports are also showing decelerating demand; perhaps even more dramatically so. The Philly Fed’s New Orders index not only fell into contraction and the weakest levels since the spring of 2020, but the 34.5 point decline month over month ranks in the bottom 1% of all monthly moves on record. In fact, that move was large enough to bring the index from the top quartile of its historical range all the way down to the bottom decile. Shipments and Unfilled Orders did not see drops down to quite as extreme levels, but each one went from the 96th percentile to 35th percentile in just one month. Again, their month-over-month declines were some of the largest on record.

Expectations are in even worse shape with similarly large declines. New Orders expectations not only saw the first negative reading since 2008, but at -7.4 it is at the lowest level since 1995. Unfilled Orders expectations have been negative for some time now meaning firms have been expecting to unwind massive backlogs built up during the pandemic due in part to supply chain disruptions. But considering the inflow of New Orders is and is expected to continue declining, Unfilled Orders expectations are at the lowest level since the start of 1974.

As we noted yesterday with the Empire Fed Manufacturing report, the decline in unfilled orders is both bad and good. With regard to the former, it is bad because it appears to in part be due to cooling off of demand. But on the bright side, it also appears to be thanks to massive improvements in supply chains. Not only did the current conditions index for Delivery Times fall sharply in June, but expectations have completely collapsed bringing it to a record low.

Another welcome sign of the report was cooling inflation as fewer respondents reported higher Prices Paid and Prices Received. Both of these readings have plateaued in recent months alongside expectations.

Employment metrics were mixed this month with the Number of Employees rebounding slightly after a big drop the prior month. Expectations, on the other hand, saw a massive 18.7 point decline. Not only was that one of the biggest declines on record but it follows two other sizeable declines in April and May. That indicates the region’s firms are expecting that hiring will moderate significantly in the coming months. Meanwhile, the Average Workweek has been pulling back with current conditions still at a historically healthy level. Click here to learn more about Bespoke’s premium stock market research service.