Bitcoin Morning Strength

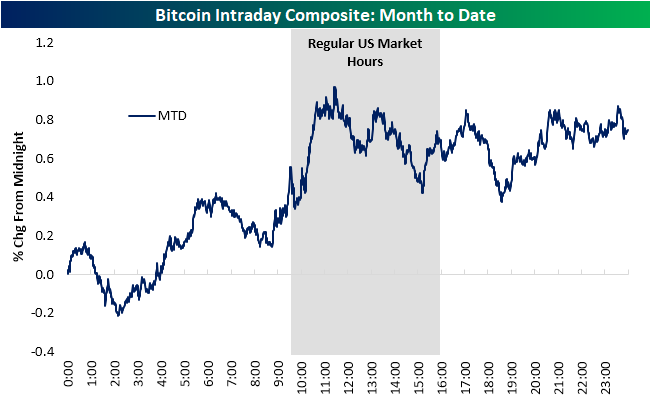

Alongside other risk assets rebounding to start the week, Bitcoin prices are approaching $74K, which is the highest price point since early February. Bitcoin and other cryptocurrencies differ from traditional assets in that they trade around the clock. In the charts below, we show an intraday composite for Bitcoin over the full course of a day over various time frames. These charts show Bitcoin’s average price movement throughout the 24-hour trading day over the time frames shown.

As shown below, Bitcoin has averaged around a 0.75% daily gain so far in March, with the bulk of that strength occurring in morning trading. In fact, Bitcoin has averaged around a 0.5% gain on the day heading into the US equity market open (9:30 AM ET) thanks to an early morning rally, and it has continued to rally towards a 1% gain by late morning. After peaking just before noon, Bitcoin has traded sideways all afternoon and night.

Bitcoin’s recent strength throughout the day is the opposite of what has been observed since the high in Bitcoin last fall. Generally speaking, throughout Bitcoin’s current drawdown, it has traded flat in the early morning hours and then lower throughout the US equity market trading day.

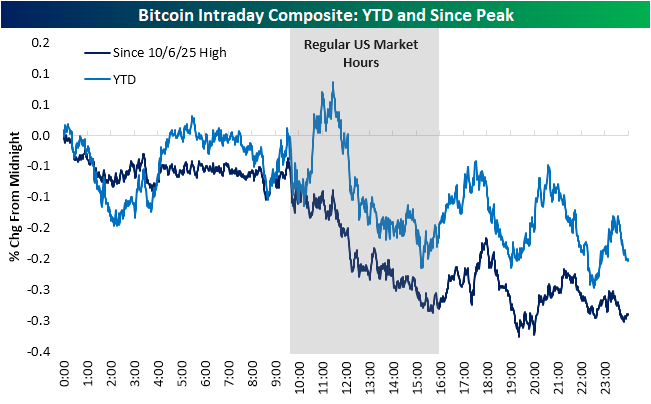

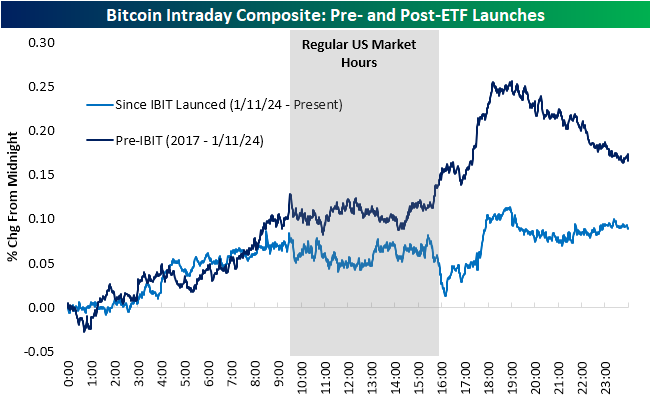

As shown below, Bitcoin has become less volatile as it has matured and especially since the latest waypoint of institutional adoption when spot ETFs garnered approval in early 2024. From 2017 up until early 2024 when the first spot Bitcoin ETFs were approved, Bitcoin generally traded higher throughout the trading day save for during regular US trading hours when price action was more flat in addition to declines late at night. Since spot ETFs like the iShares Bitcoin ETF (IBIT) were approved, though, price action has changed. Again, morning trading has been solid and even neck in neck with the intraday composite from before ETF approval. Likewise, during regular trading hours, Bitcoin price action has been largely uneventful, that is until the end of the day. Whereas previously the close of regular market hours saw Bitcoin ramping higher, since ETFs were approved, the end of the equity trading session has seen steep declines.

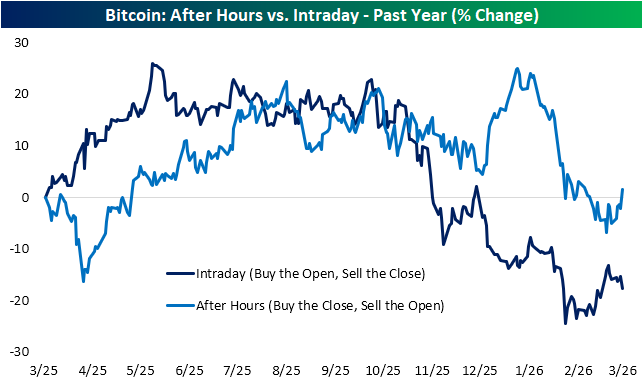

As we have done with the S&P 500 (SPY) in the past, below we show the performance of two hypothetical strategies of ownership. The first would be to buy bitcoin and only hold during regular US equity market hours (buy the open, sell the close) while the other would be the reverse of only owning outside of regular trading hours (buy the close, sell the open). As we discussed above, throughout various periods, Bitcoin performance was stable at best when stocks, bonds, and commodities are trading hands. Given this, only owning Bitcoin during regular market hours over the past year would have been the losing strategy, resulting in a 17% loss. The opposite strategy hasn’t exactly been a huge winner, but it at the moment it would still have resulted in modest gains. We would note that in the past two weeks, the two lines have begun to move in opposite directions. That dynamic was also prevalent from mid-December through the first week of the new year too.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up: