The Closer – AI Breakout, Services, Loan Growth – 4/16/26

Log-in here if you’re a member with access to the Closer.

- AI stocks are trading at some of the most overbought levels since the spring of 2023 following a surge in both Infrastructure and Implementation names in April.

- After a surprise pop last week, jobless claims data returned to healthy levels that are inline with typical seasonal patterns of the past few years.

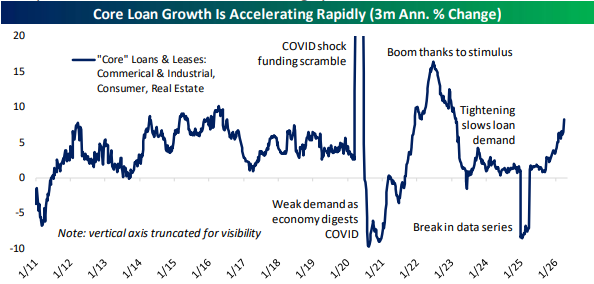

- The Federal Reserve’s H.8 report has indicated surging deposit growth this year thanks to core loan growth accelerating to 8% annualized in the past three months.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Weekly Sector Snapshot — 4/16/26

This content is for members onlyB.I.G. Tips – New Highs on Few Highs

This content is for members onlyThe Closer – Rapid Rebound, Beige Book, Record Surplus – 4/15/26

Log-in here if you’re a member with access to the Closer.

- Since 1928, this is the first time the S&P has made new all-time highs in 11 days or fewer after falling 5-10%.

- Beige Book mentions of optimistic terms rose to the highest levels since June of 2022.

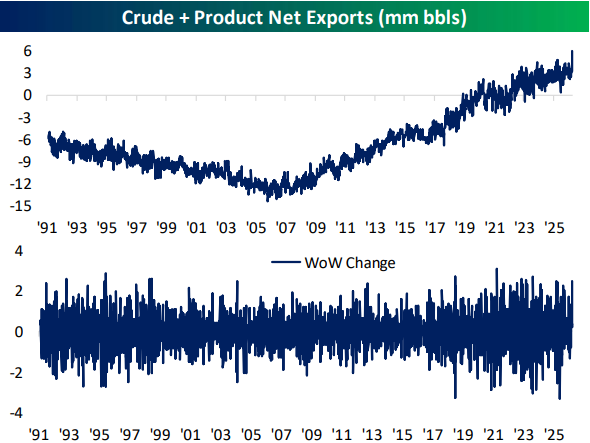

- The US saw record crude and crude product exports during the week of April 10th.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!