“Take my crude, please”

Crude oil is just about as popular or maybe even less popular than tobacco these days. Sure, there was a brief spike in prices following the US drone strike on Iranian general Soleimani last Thursday night, but ever since then, crude oil has done nothing but trade lower. Just the fact that crude only managed to rally 3% in the lead up to what many thought to be a full-blown war with Iran shows just how out of favor crude is. This isn’t the first time crude hasn’t been able to hold onto gains either. As noted earlier this week, besides the last week, there have been two other periods of heightened tensions between the US and Iran over the last year where one would have expected prices to rally, but instead they sold-off.

When a stock consistently opens at one price and then closes lower than it opened, it’s considered a negative as it signals that investors are selling into strength. Applying that logic to crude oil confirms just how out of favor it has become. This week alone, the daily closing price has been lower than its open on all five days. The chart below shows daily streaks where crude oil closed below its opening price going back to the start of 2009. While the current five-day streak isn’t anything to write home about, we would note that even before this past week’s tensions in the Middle East, in late September/early October there was a streak of 13 trading days where the commodity closed lower than it opened, and that was the longest losing streak since at least the early 1980s! Before that, there was another streak of 7 trading days in July. In other words, two of the five longest streaks since 2009 where crude oil closed below its open both occurred in the last six months. Looking for more from Bespoke? Start a two-week free trial to Bespoke Premium and receive instant access to our best research today.

Uncovering Trends With Sector Relative Strength Charts

Our Daily Sector Snapshot does a great job of consolidating key fundamental, technical, and breadth info for the eleven major S&P 500 sectors. Our trading range charts show the path of each sector over the last year with overbought and oversold levels overlaid with the sector’s price and 50-day moving average. We also include relative strength charts which show how the sector has been performing versus the S&P 500. When the relative strength line is rising, the sector is outperforming the S&P and vice versa for a falling line.

Below we have pulled both the trading range charts and the relative strength charts from our Daily Sector Snapshot for each sector. Most sectors have been performing well on an absolute basis lately and are trending nicely higher, but in many cases the sector relative strength charts tell a different story.

Both the Communication Services and Consumer Discretionary sectors are in uptrends and have broken out to new highs recently, but their relative strength versus the S&P 500 leaves a lot to be desired. Communication Services has merely been performing inline with the S&P over the last year, while Consumer Discretionary fell off a cliff versus the S&P in the early part of Q4 2019 and has just started to recover.

Consumer Staples performed well versus the S&P over the first two-thirds of 2019, but performance versus the market plummeted from late summer through year-end as the yield curve un-inverted and investors shifted into Tech, Health Care, and Financials. Energy is the only sector that has not been in an uptrend for the better part of the last year, and thus its relative strength chart has basically been a straight path lower. More recently, the slope of Energy’s relative strength decline has started to flatten, and we’ve seen some outperformance lately as geopolitical tensions heat up. Even with the improvement, though, the sector still has a lot of work to do to turn around versus the rest of the market.

The Financial sector has performed exactly in-line with the S&P 500 over the last year, but things looked a lot worse in mid-2019 when the yield curve was inverted. Once rates started to tick higher again and the slope of the yield curve turned positive in Q4 2019, the Financials really took off. That shifted the sector’s relative strength from negative to positive, but over the last few weeks we’ve seen a slight downtick as the Financials have traded more sideways.

The Health Care sector has been on a tear for the last three months, but it hasn’t been enough to shift its relative strength back into positive territory versus the S&P over the last year. The rise of Elizabeth Warren’s poll numbers held back Health Care in 2019, and once Warren’s numbers started to dip, the sector took off. That’s the reason you see Health Care’s relative strength really picking up since making a low last October.

The Industrials sector broke out to new highs recently after trading sideways for most of 2019, but its relative strength has been mostly trending lower since peaking in the first quarter last year. Materials has seen its relative strength completely collapse to start 2020. While the S&P is up 1.4% year-to-date, the Materials sector has fallen 3%. That type of underperformance does major damage on a relative strength basis.

Real Estate (REITs) had very positive relative strength for most of 2019, but this rate-sensitive sector has struggled mightily over the last few months as the yield curve has un-inverted. The price chart for Real Estate has broken its uptrend and is struggling to hang onto its 50-day moving average. With the S&P in a steep uptrend, a near-term downtrend for a sector causes its relative strength chart to collapse.

Remarkably, the Technology sector is the only one with an upward sloping relative strength chart that’s solidly in positive territory. This tells you that Tech has been the main (and only) area of true outperformance in the US equity space over the last year. At some point this is sure to reverse, and when it does, the S&P is going to struggle given Tech’s weighting in the index.

Relative strength for Utilities looks very similar to that of other defensives like Consumer Staples and Real Estate. You saw strong outperformance for Utilities at the start of Q4 2019, but it has given it all back and then some since then. To see our Daily Sector Snapshot and track these charts on a regular basis, start a two-week free trial to Bespoke Premium. You’ll unlock additional investment research like our Morning Lineup, Model Portfolios, and Chart of the Day as well.

Sector Valuations Stretched

The S&P 500 is currently up 1.4% year-to-date, but as shown below, only three sectors are outperforming the index — Technology, Communication Services, and Industrials. Given Tech’s massive weighting of more than 23% in the S&P, its 3.2% YTD gain has a big impact on the overall market’s gain. Tech’s huge weighting is also the reason why eight of eleven sectors are underperforming the S&P.

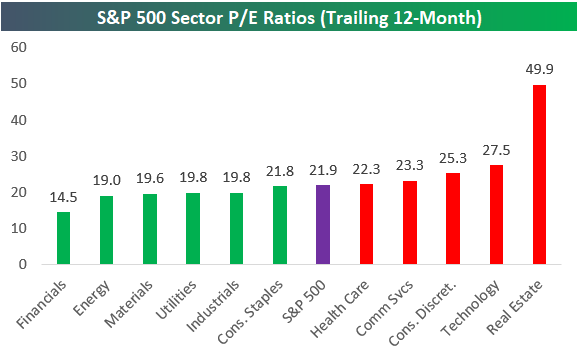

We continue to see elevated P/E ratios. The S&P’s trailing 12-month P/E is currently 21.9, while Real Estate is at 49.9, Technology is up to 27.5, and Consumer Discretionary is at 25.3. The only sector with a P/E ratio below 19 is Financials at 14.5.

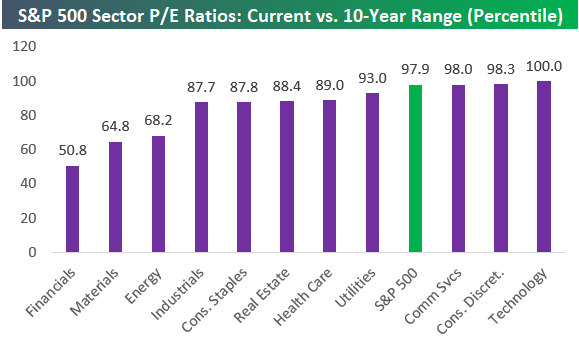

Absolute levels of valuations like the chart above don’t tell you much. The chart below shows where valuations stand for sectors relative to levels seen over the last ten years. As shown, the S&P 500’s current P/E ratio is higher than 97.9% of all other P/E readings seen for the index over the last ten years. That’s high! And three sectors have valuations in the 98th percentile or higher, with Technology at the top at 100%. Over the last ten years, Tech’s P/E ratio has never been higher.

The only sector where valuations are currently “average” compared to the last ten years is Financials. Sign up for Bespoke Premium and get half off your first three months. Click here for this special offer.

B.I.G. Tips – Consistently Overbought Readings

Dow 29,000?

By posting this, we’re probably jinxing it, but the DJIA is on the verge of topping another 1,000 point threshold less than two months after first topping 28,000. While the media makes a big deal of each of these thresholds, we would note that the road to 29,000 from 28,000 is only 3.4%. That’s hardly a momentous move. Since Trump became President in January 2017, though, 29,000 would be the 10th 1,000-point threshold that the DJIA would cross under his watch.

The table below lists the date that the DJIA first crossed each 1,000-point threshold throughout history. For each level, we also include the number of calendar days that elapsed between the first cross of that threshold and the prior one, how large a percentage gain that the 1000-point threshold represents versus the prior one, and then how many times the DJIA has crossed each threshold (on a closing basis) both to the upside and downside. One of the most notable aspects of the table in our view is that even though each threshold is a smaller percentage than the prior one, there have been so few crosses (above and below) of most of the thresholds since the Dow first crossed 19,000 after the 2016 election. 19,000 was only crossed once, and six of the other nine thresholds since then haven’t been crossed more than ten times. That’s indicative of a market that has been rallying and not looking back. Start a two-week free trial to Bespoke Institutional for full access to our research platform.

Bespoke’s Morning Lineup – 1/10/20 – Jobs Friday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

At its October meeting on 10/30, Fed chair Powell noted that “a significant inflation rise would be needed before any rate hike,” and ever since then markets have been in rally mode as even strong economic data hasn’t been taken as a signal that the FOMC would start to tighten policy. A perfect example is the monthly jobs report. As shown in the table below, on the day of the three Non-Farm Payrolls reports since the FOMC essentially took itself out of the picture, the S&P 500 has been up at least 0.90%. That’s quite a streak. The last time we saw three straight gains of 0.90%+ on the day of employment reports was back in July 2013 and going back to 1998, there have only been four other three-month streaks of 0.9%+.

The Closer – Credit Trades Tight, Repo Uptake, Inventory Outlook, Auction Update – 1/9/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we provide an update on what credit spreads are showing on the health of the economy as well as the Fed’s activity in the repo market. Next we take a look at the Department of Transportation’s freight volumes data then we show the results of today’s 30 year UST bond auction. We finish with an update on consumer comfort.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Sector Snapshot — 1/9/19

Bespoke’s Consumer Pulse Report – January 2020

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

December Employment Report Preview

After several weeks where employment-related data was mixed relative to expectations, we’ve begun to see some signs of improvement as jobless claims have edged back down. Even with that improvement, though, there have still been some mixed signals. Those mixed signals haven’t resulted in a lot of angst on the part of the market heading into the report, though. That’s because recession fears mostly seem to be in the rearview mirror, and the Fed has basically taken itself out of the picture regarding any potential hikes.

Heading into tomorrow’s Non-Farm Payrolls report, economists are expecting an increase in payrolls of 160K, which would be a 106K decline from November’s blockbuster reading of 266K. In the private sector, economists are expecting a similar decline from 254K down to 153K. Job growth in the manufacturing sector is expected to decline from 54K down to 5K. Even with the expected big decline in Non-Farm Payrolls, the Unemployment Rate is expected to stay unchanged at 3.5% while average hourly earnings are forecast to increase 0.3% compared to November’s reading of 34.4.

Ahead of the report, we just published our eleven-page preview of the December jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in December. We also include a breakdown of how the initial reading for December typically comes in relative to expectations and how that ranks versus other months.

For anyone with more than a passing interest in how equities are impacted by economic data, this December employment report preview is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!