Bespoke Brunch Reads: 1/19/20

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2020 Annual Outlook special offer.

Wall Street Week

The End of the Bonus Culture Is Coming to Wall Street by Katie Linsell and Lananh Nguyen (Bloomberg)

As Wall Street transitions towards a more recurring revenue-based system that is more automated and reliant on technology, bonuses are becoming a less important part of compensation schemes. [Link; soft paywall, auto-playing video]

U.S. Curbing Early Access to Sensitive Data Threatens Arms Race by Katia Dmitrieva and Vince Golle (Bloomberg)

Procedures related to the media lockup ahead of major data releases is changing and the results could force traders to go data-hunting on their own as they seek a leg up in the digestion of huge data releases that won’t have an out-of-the-box media narrative. [Link; soft paywall]

Less Research? No Problem, Hedge Funds Say. by Julie Steinberg and Paul J. Davies (WSJ)

Reduced analyst coverage of European stocks related to the advent of regulation coverage research has created opportunities for hedge funds that thrive in the darkness of less information. [Link; paywall]

Climate & Society

US power generators set for another big year in coal plant closures in 2020 by Anna Duquiatan, Taylor Kuykendall, Darren Sweeney, and Liz Thomas (S&P Global Intelligence)

2019 will mark the largest retirement of coal power capacity since 2015, further reducing coal demand and driven by the still-improving economics of natural gas and renewables. [Link]

Food & Drink

The Capitalist Way to Make Americans Stop Eating Meat by Derek Thompson (The Atlantic)

With carnivores challenged by the combination of animal welfare and the carbon impact of their eating habits, innovations across the spectrum of technology and culinary arts are fueling “peak meat”. [Link; soft paywall]

Panera Bread to cut meat on its menu by a third by Alistair Gray (FT)

In-line with the trends described in the prior story, Panera has moved to reduce the number of menu options which include meat over the next couple of years. [Link; paywall]

America Drank Less Wine for First Time in 25 Years by Saabira Chaudhuri (WSJ)

Less wine (on a volume basis) was purchased in 2019 than in 2018, the first sequential drop since 1994; industry groups blame less consumption of alcohol overall along with much less demand for low-price wine. [Link]

Zeitgeist

The Twitter Electorate Isn’t the Real Electorate by Helen Lewis (The Atlantic)

An argument that the flattening of newsrooms that social media has brought does not actually succeed at exposing them to opinions traditionally excluded from the media. [Link; soft paywall]

The 10 Most Checked-Out Books in N.Y. Public Library History by Concepción de León (NYT)

Dystopian science fiction, children’s books, and Harper Lee’s classic “To Kill a Mockingbird” are the most-read books in the long history of the New York Public Library. [Link; soft paywall]

Panic, Or Don’t

Few Bank Failures Could Be a Warning Sign for U.S. Financial System by Andrew Ackerman (WSJ)

We can remember a time when the high number of bank failures was a sign things were very bad, but apparently the opposite is the case. If there was ever an effort to spin good news poorly, this is it. [Link; paywall]

Money-Losing Companies Mushroom Even as Stocks Hit New Highs by James Mackintosh (WSJ)

With the rise of hyper-growth companies and firms dependent on network effects, more and more public companies don’t actually make any money. [Link; paywall]

Time For Tech

Silicon Valley reinvents Victorianism by Jamie Powell (FTAV)

The latest tech start-up to get attention is San Francisco company that re-creates servants with an app, and without using much in the way of technology to do so. [Link; registration required]

EU considers temporary ban on facial recognition in public spaces by Janosch Delcker and Bjarke Smith-Meyer (Politico)

With privacy concerns around facial recognition picking up, the EU is considering a ban on the use of the technology in public spaces. [Link]

Iran

How the US Knew Iranian Missiles Were Coming Before They Hit by Daniel Oberhaus (Wired)

Ground-based radar and satellite detection systems are key to giving US installations and troops an early warning when hostile missiles start flying. [Link]

Shocking Revelations

‘Rich kid of Instagram’ accused of swindling investors out of millions by Amanda Woods (NY Post)

A British teen claimed to make turn 200 pounds into six figures, then used the notoriety to take advantage of investors. [Link]

Health

The medications that change who we are by Zaria Gorvett (BBC)

Side effects from unremarkable, widely-prescribed drugs are turning up some strange behaviors from patients. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

B.I.G. Tips – S&P 500 Decile Analysis to Start the Year

The Bespoke Report – 1/17/20 – The Dominant Dozen

This week’s Bespoke Report newsletter is now available for members.

We’re just twelve days into the new year, but already it’s a year that is topping some strategists year-end targets. Granted, they were extremely conservative heading into the year, but if you’re a Wall Street strategist and already you’re going back to the drawing board just twelve days into the year, it’s going to be a long year.

For analysts, it’s a similar predicament. As of this week, the average analyst target price for stocks in the S&P 500 is just 4.64% above the average actual share price. Going back to at least 2004, there has never been another time where stock prices have been so close to their average analyst price targets. As an analyst, it’s hard to justify a buy rating on a stock if it’s trading at your price target!

In this week’s Bespoke Report, we provide our take on everything going on in the market this week, a preview of the upcoming earnings season, and how to view the market after what has already been a great start to the year. To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 1/17/20

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

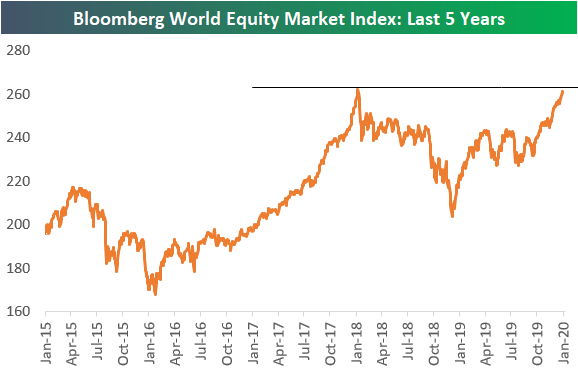

Global Equities Closing In On A Breakout

Below is a chart of the Bloomberg World Equity Market index, which is a cap-weighted index made up of nearly 5,000 publicly listed companies around the world (including the US). While the S&P 500 is up more than 15% from its January 2018 high, it’s notable that we still haven’t seen equities break out on a global scale. As shown, the Bloomberg World Index is now just a hair below its prior all-time highs (22 basis points to be exact). Start a two-week free trial to Bespoke Institutional to access our full library of research and interactive tools.

Bespoke’s Morning Lineup – 1/17/20 – Taking it to the House!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

With today’s strong report on Housing Starts, homebuilders will be a focus today. The group was a leader throughout most of 2010 but has been in a period of consolidation since Q4 of last year. This week, though, the group was finally able to break out to new highs, and data like today’s should only help the group going forward.

The Closer – Small Cap Surge, Manufacturing Mumbo Jumbo, Trade Prices – 1/16/20

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the recent outperformance of the small cap Russell 2000 and overbought conditions of the large cap S&P 500. Next, we show the differing performances of gold and silver over the past few months before turning to macroeconomic data including today’s releases of continuing jobless claims, manufacturing sentiment, and trade prices.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Market As Close To Targets As It Gets

Bulls Come Back

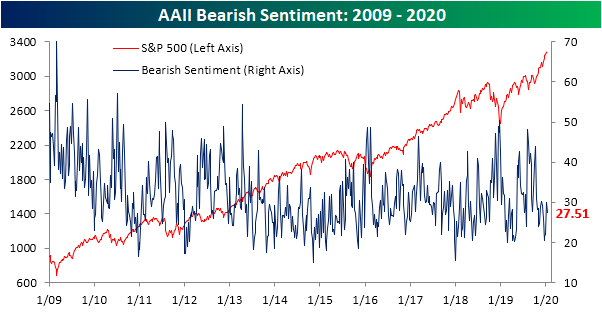

Even though equity markets shrugged off geopolitical tensions last week, sentiment actually declined based on AAII’s weekly survey. However, as equities have continued to move higher over the past week on solid earnings and the situation in the Middle East has further simmered down, sentiment has picked back up. This week, 41.83% of investors reported bullish sentiment, up from 33.07% last week. Although this only brings bullish sentiment to similar levels as the final week of 2019, that 8.76 percentage point increase this week was the largest weekly increase since mid-October. This also lifts it back above its historical average of 38.08%.

Even though bullish sentiment has surged, bearish sentiment was little changed at 27.5%; just 2.39 percentage points lower than last week. Thanks to the pick up in bullish sentiment, the bull spread has once again widened to 14.32 in the bull’s favor. Other sentiment readings like the Investors Intelligence survey similarly have seen stable bearish sentiment recently as bearish sentiment was unchanged at 17.8%.

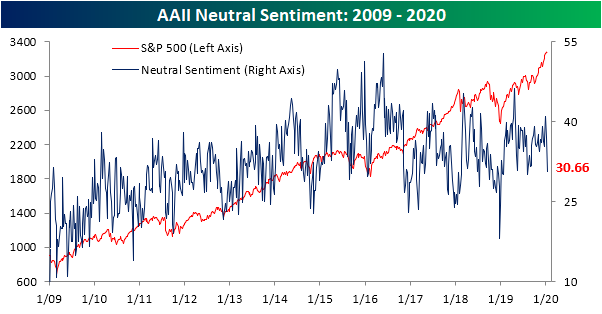

Considering most of the gains in bullish sentiment did not come from bears, neutral sentiment tanked to 30.66%. That is the largest weekly decline since August 8th when it fell 7.35 percentage points compared to the 6.38 percentage point drop this week. While it’s now at the lower end of the past year’s range, just two weeks ago neutral sentiment topped 40%. Declining 10.25% in that time, this was the first time that neutral sentiment experienced a double-digit drop in the span of two weeks since May. This drop has also snapped a 22-week streak that neutral sentiment has remained above its historical average. Going back through the history of the survey, there have only been five longer streaks, the next longest of which ended at 25 weeks in 2017. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.