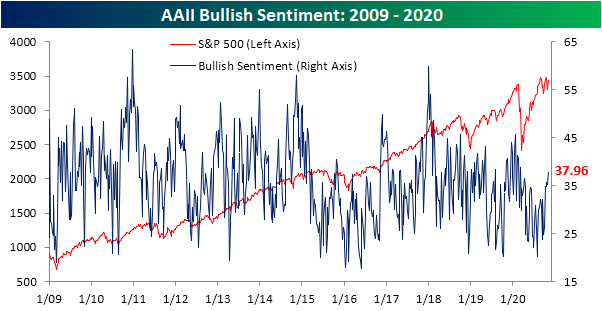

Bullish Sentiment Back Above Average

After remaining depressed for most of the past few months, the past several weeks have marked a rapid turn higher in bullish sentiment as per the American Association of Individual Investors’ weekly survey. As shown in the first chart below, bullish sentiment rose another 2.67 percentage points this week to 37.96%. That is the most optimistic reading on sentiment since the first week of March.

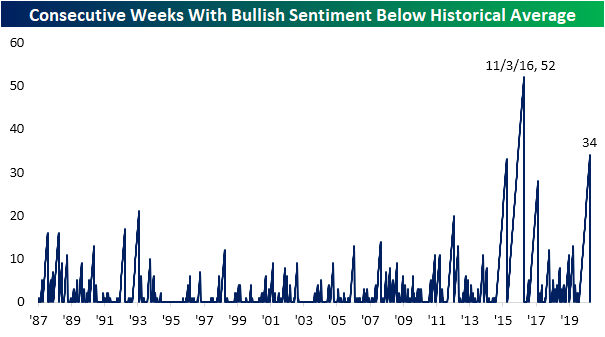

As the percentage of bullish respondents has risen to the high-30% range, it has finally moved just barely above its historical average of 37.91%. That is the first time this has happened in 34 weeks. As shown below, that makes for the second-longest streak of below-average readings on bullish sentiment in the survey’s history. The only one that went on for longer was back in 2016 when the streak lasted for exactly a year.

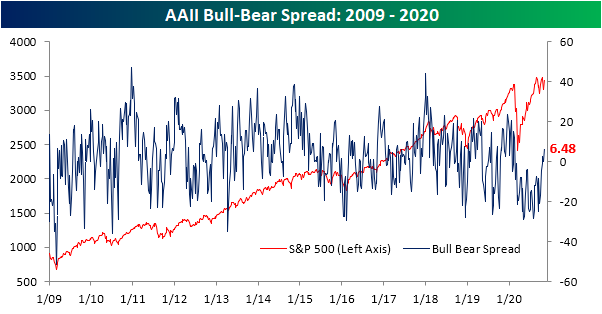

As bullish sentiment rose, bearish sentiment fell. Only 31.48% of investors reported as bearish which is the lowest level of market pessimism since February 20th; one day after the last bull market peak. Following the stretch of historically elevated readings over the past few months, this week’s decline brings the reading into the middle of its historical range (58th percentile), though unlike bullish sentiment, that is still slightly above the historical average of 30.63% as has been the case for the past 37 weeks. That is also the second-longest streak of above-average readings in bearish sentiment on record behind one that went on for 83 weeks ending in 2009.

Given the respective moves in bullish and bearish sentiment levels, the bull-bear spread has moved higher into positive territory after a reading of zero last week. With a move higher of 6.48 points this week, the bull-bear spread is at the highest level since February 20th.

Not every investor has a strong opinion on the market though. The percentage of respondents reporting as neutral was also higher this week, rising 1.15 percentage points to 30.56%. That is still off the pandemic high of 31.96% from July. Click here to view Bespoke’s premium membership options for our best research available.

The Bespoke 50 Top Growth Stocks — 11/5/20

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 177.1 percentage points. Through today, the “Bespoke 50” is at new all-time highs and up 332.0% since inception versus the S&P 500’s gain of 154.9%. Always remember, though, that past performance is no guarantee of future returns. To view our “Bespoke 50” list of top growth stocks, please start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: Breadth Doesn’t Have The Votes

Extended Benefits Expand

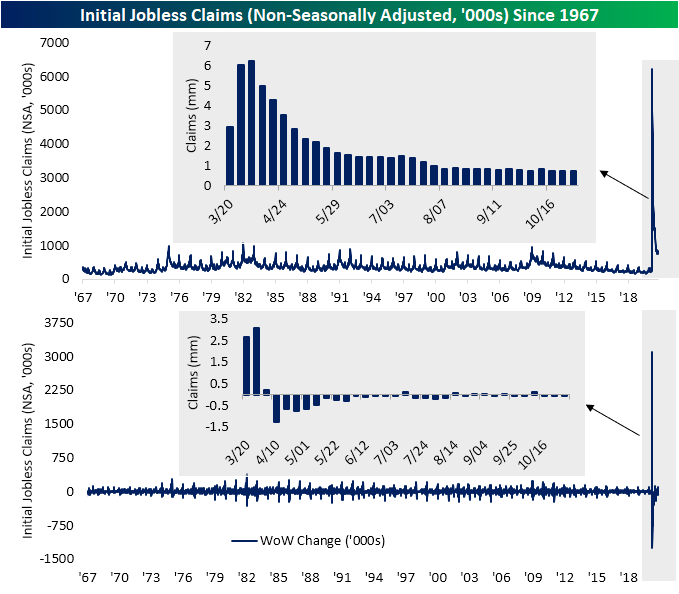

Initial jobless claims for the final week of October came in at another pandemic low at 751K. That would have been unchanged from the previous week’s number, but that was revised up 7K to 758K. Regardless of that revision higher, initial claims have declined for three straight weeks although the pace of decline has been slowing. Given this week’s decline was comparably small to recent weeks, this morning’s release did miss estimates calling for a level of 735K.

On a non-seasonally adjusted basis, initial claims were pretty flat only falling 0.5K to 738.2K. That established a slightly lower post-pandemic low and marked the 14th consecutive week that initial claims have come in below 1 million.

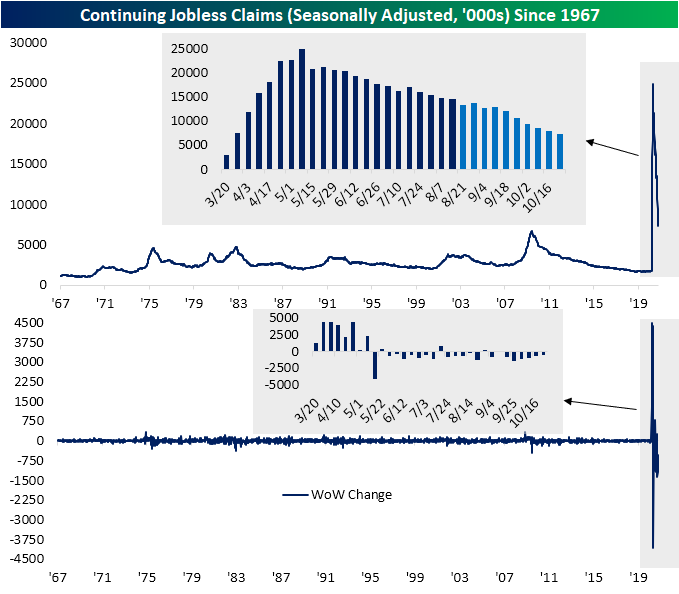

Continuing claims data is released at a one week lag to initial claims, and last week’s sizable decline led continuing claims to also reach a new low for the pandemic. At 7.285 million, it was still above estimates of 7.2 million. Continuing claims have now fallen for 7 of the past 8 weeks, and the one week where they didn’t drop, they were unchanged.

Including Pandemic Unemployment Assistance (PUA) to get a more complete picture, the declines in regular state initial claims have been slightly offset by rising PUA claims. Total initial claims (PUA plus regular state claims) were up this week from 1.098 million to 1.101 million meaning claims continue to hover around 1.1 million as has been the case over the past month. Whereas regular state claims have fallen for three straight weeks with a total decline of 91.5K, PUA claims have risen for three straight weeks totaling 25.66K.

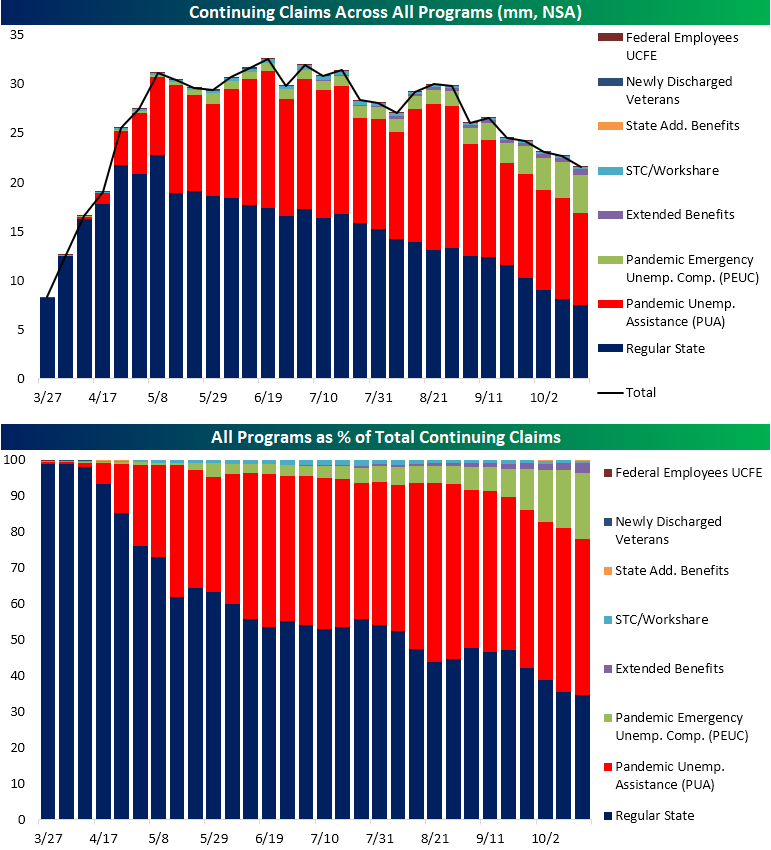

Although inflows to the unemployment insurance system have been stable at around 1.1. million, on net, the number of people receiving benefits has continued to fall. In the charts below, we show the total count (in millions) of continuing claims across all programs. The data is lagged yet another additional week to regular state claims. As of the week of October 16, total continuing claims reached 21.6 million which is the lowest level in seven months. Claims have now fallen in seven of the last eight weeks with regular state claims and PUA claims (the two largest contributors) driving those declines. On the other hand, extended benefit programs for those who have seen their insurance expire like Pandemic Emergency Unemployment Compensation and regular state extended benefits have been on the rise. These two measures are at new highs in terms of both the number of claims and their share of total claims. That means that despite an overall improvement in the number of people on unemployment, there is a growing share that have been unemployed for an extended period of time. Click here to view Bespoke’s premium membership options for our best research available.

Emerging Markets Cheering a Potential Biden Win

The US equity market has seen a massive rally in reaction to what is looking like a Biden victory over President Trump coupled with the Republican party maintianing its majority in the US Senate. None of these results are official at this point, so they are subject to change, but these are the most likely scenarios as of now. Outside of the US, emerging markets have also rallied. In just the last two days, the MSCI Emerging Market ETF (EEM) has rallied 5% and broken above resistance to new 52-week highs. If for no other reason then Biden’s campaign slogan isn’t America First, the rationale behind the rally makes some sense.

The reaction of EEM in the aftermath of this election is very much different from what happened in 2016. Heading into the 2016 election, EEM had been trending higher, but pulled back in the days leading up to the election and broke its uptrend that had been in place since earlier in the year. Again, Trump’s America First approach was understandably viewed as a headwind to emerging market equities.

While the initial reaction of EEM to Trump’s election was negative, that weakness didn’t last long. The chart below shows the performance of EEM in the two months before and one year after the 2016 election. The gray box represents the same period shown in the chart above. Within days after breaking its uptrend after the 2016 election, EEM bounced back, rallied to its 50-DMA, tested its November low, and then in the early days of 2017 it was off to the races as EEM. In fact, even accounting for the post-Election Day declines, one year after the 2016 election, EEM was up 25% which was actually more than the 21% return for the S&P 500! The moral of the story here is that first reactions aren’t always the right reactions, and as an investor it’s not just imperative to know the environment you are operating in, but also when the tides are turning. Click here to view Bespoke’s premium membership options and unlock instant access to our research and interactive tools.

Bespoke’s Morning Lineup – 11/5/20 – Groundhog Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Information is not knowledge.” – Albert Einstein

When you turned on your TV to one of the financial networks or cable news channels this morning that wasn’t your DVR showing yesterday’s news. The election still hasn’t been decided and equities are once trading sharply higher. Over the course of the last 24 hours, not much has really changed. The path for the President is looking increasingly narrow, and markets seem to be content with the prospect of gridlock.

In economic news, both initial and continuing jobless claims came in modestly higher than expected. Non-farm productivity was a bit weaker than expected, and Unit Labor Costs were less bad than forecast. While it was easy to overlook given all the other news, don’t forget that there is also an FOMC decision this afternoon!

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, election analysis, trends related to the COVID-19 outbreak, and much more.

After the worst pre-election week for the S&P 500 in its history last week, it only makes sense that the S&P 500 would be on pace for one of its best-ever election week performances on record. It is 2020 after all! With futures indicating a 1.5% gain at the open, the S&P 500 is on pace for its second-best election week performance since 1928. To find the best election week performance for the S&P 500 on record, you have to go all the way back to 1932 when FDR won in a landslide.

An interesting trend to note about recent election cycles is that they have become increasingly volatile. Going back to 1996, the S&P 500’s average percentage move the week before Election Day has been a move of +/-3.6%. That’s more than twice the average pre-election move of the prior 17 election cycles going back to 1928. Similarly, the S&P 500’s average election week performance has been a gain or loss of over 4%. Likewise, that’s also just about twice the prior average of election cycles spanning 1928 to 1992!

With all the information investors have had at their fingertips in the last 25 years, you would expect that it would dampen volatility in reaction to big events like elections, but the data of the last 25 years since Netscape – the first mainstream internet browser – was launched shows a much different outcome. Information is often confused with knowledge, but as Einstein succinctly put it, the two aren’t the same.

Daily Sector Snapshot — 11/4/20

Services Dip

Whereas Monday’s manufacturing release of the ISM report for the month of October exceeded estimates and continued to rise to new highs for the pandemic, this morning’s service sector report was weaker. The release was anticipated to show a slight decline, falling to 57.5 from 57.8 last month. Instead, that decline was even larger with the headline number dropping to 56.6. That is the lowest level of the index since May, and while it is still indicative of expansionary activity, it was at the slowest rate of the recovery. That has led the composite of the manufacturing and non-manufacturing readings to similarly be a bit on the weak side, falling from 57.5 to 56.9. Again this is consistent with overall growth versus last month, but at a slower rate.

Given the headline number’s decline, breadth in this month’s report was a bit weak. Just six of the ten sub-indices were higher this month. Despite this, every index remains in expansion with those for Inventories and Import Orders actually exiting contraction.

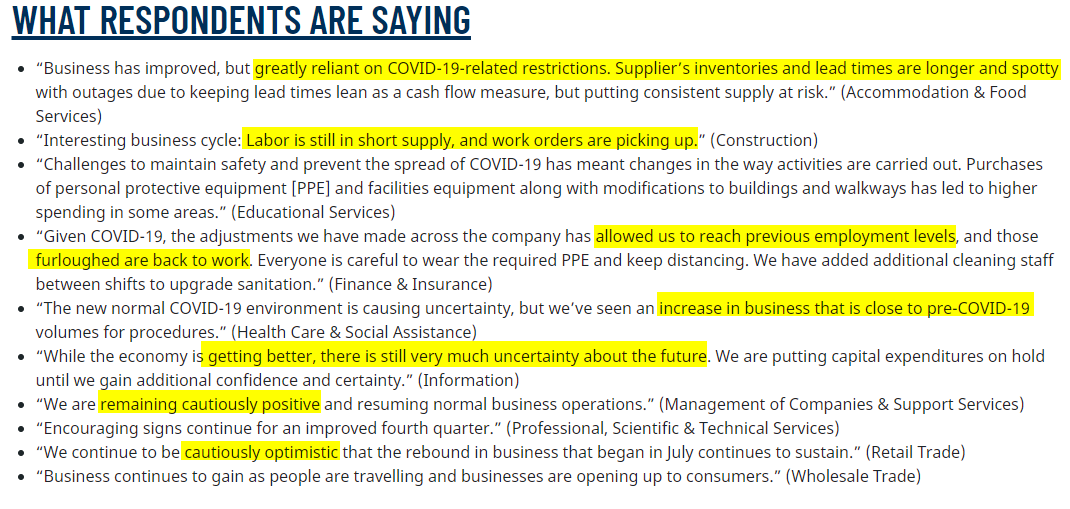

Broadly speaking, the survey showed that conditions have continued to improve but at a slowed pace in October. Given this, the key phrase of the commentary section seemed to be “cautiously optimistic”. Multiple comments made mention that business has gotten better with solid demand and workers coming back, but uncertainty has persisted.

New Orders have continued to grow, but at a slowed pace as the corresponding index fell 2.7 points to 58.8 in October. Unlike the same index for the manufacturing survey which is at multiyear highs, the services index for new orders is in the middle of its historical range. On the other hand, given orders have continued to rise, backlogs have also continued to rise. The index for Backlog Orders rose 4.3 points to 54.4 which is the highest level since the summer.

As demand sits at solid levels, Inventory Sentiment remains historically low. That index fell to 51.1 in October which is the third-lowest level since 1997 behind July and March. In other words, very few businesses are reporting that inventories are too high. Despite this, the index for Inventories actually indicated that inventory levels grew in October as the index rose to 53.1. That compares to a reading of 48.8 last month which is consistent with drawdowns in inventory levels.

Employment experienced its first expansionary reading of the pandemic in September, but in October hiring appeared to slow as the index fell to 50.1. Although that is still indicative of net hirings, it shows that businesses were slower to bring in/back workers. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day – Was it the Election or Something Else?

Bespoke’s Morning Lineup – 11/4/20 – Stay Tuned!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“The poll that matters is the one that happens on Election Day.” – Heather Wilson

Americans were expecting a wild election night, and that’s exactly what we got. Heading into the results, it was Biden’s election to lose. As early state results came in the odds skewed heavily towards Trump, but overnight and early this morning the odds started to turn in Biden’s favor where they remain now. With all the uncertainty, you would guess that futures would be trading lower, but they’re up across the board with the Nasdaq leading the way. Republicans holding onto the Senate makes the reflation trade less attractive, and that is pushing down interest rates and pushing growth stocks higher.

In economic news, the Employment picture turned a little darker as the ADP Private Payrolls report for October missed expectations by a wide margin as the economy created just 365K jobs compared to expectations for growth of 634K.

Be sure to check out today’s Morning Lineup for a rundown of the latest stock-specific news of note, market performance in the US and Europe, some election analysis, trends related to the COVID-19 outbreak, and much more.

With the outcome of the election uncertain and legal challenges looking increasingly likely, we are immediately reminded of the uncertainty that surrounded the aftermath of the 2000 election. Most of us remember how poorly the market traded during that period, but in the chart below we show the intraday chart of the S&P 500 in the three days that followed the election. In those three days, the S&P 500 traded down more than 4.5%. What’s interesting to note is that in the opening minutes of trading the day after Election Day, the S&P 500 actually opened the day higher before sellers stampeded in.

This will be a key indicator to watch in trading today. Futures are currently firmly in positive territory this morning, and much more positive than they were in 2000 the day after that election. If those early gains can hold, a nightmare scenario of November and December 2000 will look increasingly less likely.