Chart of the Day – June Intra Month Performance

Bespoke’s Morning Lineup – 6/1/21 – June Comes in Like a Bull

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Time is your friend; impulse is your enemy.” – John Bogle

June is coming in like a bull this morning as equity futures are all trading firmly in positive territory. Generally positive economic data out of Asia and Europe has been the catalyst, and investors will be looking for that trend to continue in the US with the Markit Manufacturing and ISM Manufacturing surveys of the US economy as well as Construction Spending at 10:00 and the Dallas Fed Manufacturing report at 10:30.

Read today’s Morning Lineup for a recap of all the major market news and events including a recap of some notable earnings reports, major economic data out of Asia and Europe, and the latest US and international COVID trends including our vaccination trackers, and much more.

The month of May closed out on a positive note for most sectors. Last week, eight of eleven sectors finished the week in positive territory. Leading the way higher, Consumer Discretionary, Communication Services, Real Estate, and Industrials all traded up over 2% while Utilities, Health Care, and Consumer Staples were the only three sectors to finish the week lower. With last week’s gains, the majority of sectors head into June at overbought levels, although Consumer Discretionary, which was the top-performing sector on the week, is one of just two sectors below its 50-DMA.

Bespoke Brunch Reads: 5/30/21

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

Inflation

Reopening Is Inflation’s Cure, Not Cause by Jason M. Thomas (WSJ)

As patterns of supply and demand normalize after the pandemic, the price dislocations which have sent small categories of inflation soaring are likely to normalize into more familiar patterns that moderate the recent spike. [Link; paywall]

83% Of Americans Are Belt Tightening Due To Inflation Pressures by Walter Loeb (Forbes)

While consumer spending has boomed, Americans report they aren’t actually spending as much as they are, scared off by the high price of food and other goods. [Link; paywall]

Memorial Day

The First Decoration Day by David W. Blight (Newark Star Ledger/David W. Blight)

Recalling the origin of Memorial Day, which started as a march honoring Union war dead on the grounds of what used to be the slaveholders’ race track in Charleston, South Carolina. [Link]

Auto Industry

Cars Are About to Get a Lot More Expensive by Anjani Trivedi (Bloomberg)

With the used car market jammed with demand as well as semiconductors and other basic input commodities coming up in short supply, auto manufacturers are getting a golden opportunity to raise prices. [Link; soft paywall]

Tesla Model S Reaches Parity With Gas-Powered Cars In Test Drive (Value Walk)

A recent road test saw the Tesla Model S travel over 300 miles at 75 miles per hour, a first for the electric vehicle company and a key range achievement relative to the performance of internal combustion engines. [Link]

Investing

Dow Jones Industrial Average Celebrates 125 Years as Wall Street’s Bellwether by Karen Langley and Peter Santilli (WSJ)

This week saw the venerable Dow Jones Industrial Average introduced, starting a history that has weathered every bull and bear market since. [Link; paywall]

Bank of America’s Merrill Lynch to Ban Trainee Brokers From Making Cold Calls by Rachel Louise Ensign (WSJ)

While cold LinkedIn messages are still okay, advisor trainees in the Thundering Herd will no longer be encouraged to give prospective clients an uninvited phone call. [Link; paywall]

A New ETF Taps Investors’ Fear of Missing the Latest Hot Stock Trend by Evie Liu (Barron’s)

FOMO will try and hold stocks that are currently on the market’s radar but doesn’t hold stocks like COIN or any of the SPAC stocks which have made such a big splash in both directions over the past year. [Link; paywall]

Tech

A Cynic’s Guide To Fintech by Dan Davies (Medium)

While this rundown is over half a decade old, it helps to point out the relatively limited scope that fintech companies can operate in with a durable competitive advantage. [Link]

How 5G May Improve Early Warnings of Severe Weather by Marco Quiroz-Gutierrez (WSJ)

Changes in the signals of cellphone towers can be used to measure humidity shifts, a key data point that may help meteorologists develop more accurate and timely weather models which can speed up warnings. [Link; paywall]

Facebook Reverses Ban on ‘Man-Made’ COVID References After Biden Orders Review by Alex Noble (Yahoo! News)

As the discourse shifts, Facebook has lifted a blanket ban on asserting that COVID was created in a lab, a claim that has been latched on to by the conspiratorial fringe since the first days of the pandemic. [Link]

Pot

Positive Marijuana Tests Are Up Among U.S. Workers by Matt Grossman (WSJ)

2.7% of the 7 million drug tests conducted by Quest Diagnostics for employers came back positive for marijuana as a rising share of the national labor force lives in states where recreational marijuana use is legal. [Link; paywall]

Real Estate

In Tight Housing Market, Thousands of Homes Are Reserved for Certain Buyers by Nicole Friedman (WSJ)

With so much demand, sellers are able to sidestep the public sales process to show homes to a select group of buyers, though such “pocket listings” account for only 3% of sales this year. [Link; paywall]

Cardio

The Cardiovascular Secrets of Giraffes by Bob Holmes (Smithsonian Mag)

To make sure blood circulates their extremely tall bodies, giraffes have to have very high blood pressure, but they don’t suffer most of the maladies that come with high blood pressure in humans. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 5/28/21 – MoMo Makes A Comeback

This week’s Bespoke Report newsletter is now available for members.

High volatility stocks with big retail participation (so-called “meme” names) made a big come back this week and Chinese equities broke out. We discuss these moves along with the receding COVID pandemic, an increase in investors looking for a correction, a fresh decline in crypto markets, renewables power uptake in the US and how renewables stocks have been performing, earnings Triple Plays, very strong economic data across the world economy, surging gas prices and the oil production picture in the US, booming house prices but slowing new home sales, surprisingly affordable prices for new homes, solid consumer confidence, booming manufacturing activity from regional Fed surveys, revised US GDP in Q1, core PCE inflation numbers in the US, the outlook for an infrastructure package from Congress, and more in this week’s Bespoke Report.

To read the report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Daily Sector Snapshot — 5/28/21

B.I.G. Tips – June 2021 Seasonality

Bespoke’s Morning Lineup – 5/28/21 – Salesforce.com Drives the Dow

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

“Focus on the 20 percent that makes 80 percent of the difference.” – Marc Benioff

It seems weird to say that a 5% rally in Salesforce.com (CRM) is driving the Dow higher today, but since it was added to the index late last August, Marc Benioff’s company is on pace for one of its largest one-day gains accounting for about half of the Dow’s pre-market gains this morning.

In economic data, it’s been a busy morning but so far there hasn’t been much in the way of surprises. The only other releases on the calendar are Chicago PMI at 9:45 and Michigan Confidence at 10 AM. With the holiday weekend on the horizon, look for this afternoon’s trading to be on the quiet side.

Read today’s Morning Lineup for a recap of all the major market news and events including a recap of some notable earnings reports, major economic data out of Asia and Europe, and the latest US and international COVID trends including our vaccination trackers, and much more.

Although equity futures are higher this morning, the crypto space is under pressure heading into the long weekend following some cautionary comments from BoJ Governor Kuroda (who says crypto isn’t uncorrelated?). It’s been an interesting week for bitcoin and ether. Throughout the week, they made multiple attempts to break above short-term resistance, but each one was met with selling. In bitcoin’s case, the resistance level was right around $40,000 while for ether it was $2,900. After several unsuccessful attempts at sealing the deal, it looks like traders in both crypto assets have given up heading into the weekend.

More and More Investors Are Looking For A Correction

The S&P 500 has been hovering around 0.5% below its record highs this week, but without a true test of those highs, sentiment has not moved very far. The American Association of Individual Investors‘ weekly reading on bullish sentiment fell from 37% last week down to 36.4%. While that is the second week in a row with an absolute move less than a full percentage point in size, the marginally lower reading does leave bullish sentiment at the lowest level since the end of October.

Bearish sentiment moved by even less, only rising 0.1 percentage points. At 26.4%, it still is below the reading of 27% from the first week of the month. Outside of that reading, that is the highest level since February.

This week’s moves left the bull-bear spread little changed at 10. That’s down 0.7 points from last week but still above the 9.5 reading from two weeks ago.

Once again, the highest percentage of investors are in the neutral camp at 37.1%. As was the case last week, that makes for the highest level in neutral sentiment since the first week of 2020 when it stood north of 40%.

Pivoting over to sentiment for equity newsletter writers measured in the Investors Intelligence survey, there were some more interesting moves. Bullish and bearish sentiments were not necessarily anything to gawk at similar to the AAII survey. Bullish sentiment has been on the decline with this week’s survey showing a 3 percentage point drop to 51.5%, the lowest level since March 10th. Meanwhile, bearish sentiment moderated from 17.2 to 16.8%. That was the same level as the start of the month.

The percentage of respondents “looking for a correction” was more notable. Rather than simply asking whether or not respondents foresee a correction in the technical sense on the horizon (a 10% decline from a high), Investors Intelligence defines a newsletter writer as “looking for a correction” when they are bullish on a list of stocks but at a lower price point. Coming in at 31.7%, the reading is a few percentage points above the historical average of 27.6% and is in the top quartile of the historical range. In other words, it is an elevated reading albeit far from without precedence. What is more significant is that it has been over a year since this part of the survey has seen these levels.

In the history of the survey dating back to 1963, there have only been eight other times that the percentage of newsletter writers looking for a correction has crossed above 30% for the first time in at least a year. The most recent of these was in April 2009. In the table below we show the S&P 500’s performance in the year following those occurrences. As shown, performance has been generally positive across those past instances with average gains over the following weeks and months and moves higher at least 75% of the time one month, three months, and one year out. Additionally, while there were two times, 1982 and 2009, in which the S&P 500 rallied over the following year without looking back, there were another two times, 2001 and 2007, that at the following years’ lows, the S&P 500 would end up lower by double-digit percentage points. Click here to view Bespoke’s premium membership options for our best research available.

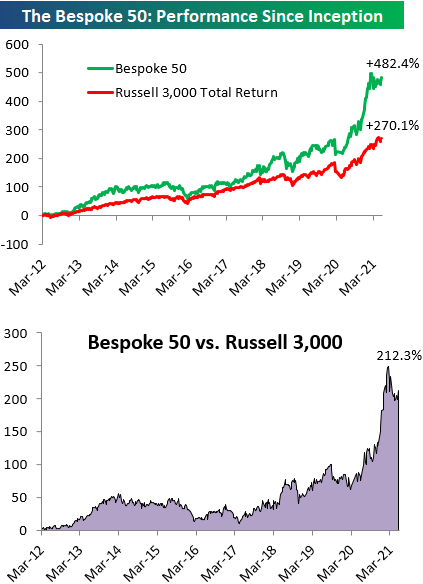

The Bespoke 50 Top Growth Stocks — 5/27/21

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” list is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” is up 482.4% excluding dividends, commissions, or fees. Over the same period, the Russell 3,000’s total return has been +270.1%. Always remember, though, that past performance is no guarantee of future returns. (Please read below for more info.) To view our “Bespoke 50” list of top growth stocks, please start a two-week trial to either Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated weekly on Thursday. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning each week. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, fees, or dividends are not included in the performance calculation. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities.