Daily Sector Snapshot — 8/17/21

B.I.G. Tips – Retail Sales Marked Down

Bespoke Stock Scores — 8/17/21

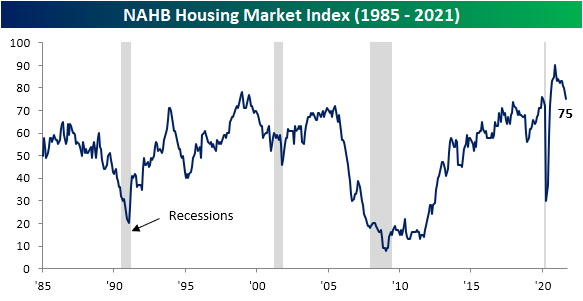

Homebuilder Sentiment: The Next Big Miss

Prior to the pandemic, the NAHB’s record monthly reading on homebuilder sentiment was back in December 1998 when the index hit 78. Last November, the sentiment bar was set even higher when the index reached 90. Since then, though, two-thirds of the releases have declined month over month. The most recent release saw the index drop five more points to 75, marking the first time in a year that homebuilder sentiment came in below the pre-pandemic record high. Additionally, August’s 5-point drop is the largest one-month decline since last April when the index collapsed by a record 42 points at the onset of the pandemic. It is also tied with a dozen other months for the seventh-largest month-over-month decline in the history of the index going back to 1985.

While the release indicates worsening, but still historically strong, sentiment among homebuilders, it can be added to the growing list of economic indicators that have been coming in well below expectations. As we noted in last week’s Bespoke Report, Citi Surprise indices measuring how economic data comes in relative to estimates tipped into negative territory last week. That was as the University of Michigan’s Consumer Sentiment survey saw the biggest miss relative to expectations on record. Today’s reading on homebuilders was not far off those results. The five-point miss relative to expectations was the largest since last April and is tied with 4 other months (April and May 2006, November 2008, and October 2014) for the six largest miss going back to at least 2003.

Driving the decline in the headline reading were five-point drops in present sales and traffic. Even though there has been deterioration in those readings on current conditions, future sales have held up better going unchanged at 81.

Looking across regions, the ones that have seen COVID cases rising the most of late, namely in the South and Midwest, generally saw sharp drops in homebuilder sentiment in August although those are in the context of longer-term declines. The Northeast and the West, on the other hand, are off of their peaks but each region did show an uptick in sentiment for August. Click here to view Bespoke’s premium membership options.

Chart of the Day – New S&P 500 Record Highs Reach Record Pace

Bespoke’s Morning Lineup – 8/17/21

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“All animals are equal, but some animals are more equal than others.” – George Orwell, Animal Farm (published on this day in 1945)

Chinese equity ETFs are trading down more than 2% this morning on continued regulatory concerns out of the country. US equity futures are lower as well as both Walmart (WMT) and Home Depot (HD) are set to open down following their earnings releases. These reports mark the unofficial end to the Q2 reporting period, which we will recap further later this week. Retail Sales were just released and missed expectations with weakness in Autos contributing to the decline.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Also, make sure to check out our Daily Sector Snapshot.

The two most overbought sectors at the moment are the two most defensive sectors — Utilities (XLU) and Consumer Staples (XLP). Utilities have been on an absolute tear lately with XLU now 5.5% above its 50-DMA.

At the same time, the relative strength of the Consumer Discretionary sector just hit new lows.

Want to see more charts and analysis ahead of today’s open? This morning we’re covering earnings reports from Walmart (WMT) and Home Depot (HD), the recent underperformance of small-caps, weakness for Chinese ADRs, and chart patterns for the mega-cap Tech stocks. Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.

Daily Sector Snapshot — 8/16/21

Chart of the Day: Reversal of Re-opening or Seasonality?

B.I.G. Tips – State-Level Covid Test Search Trends

Bespoke’s Morning Lineup – 8/16/21

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Governments never learn. Only people learn.” – Milton Friedman

The pictures all over the news were disheartening this weekend with the Taliban increasingly taking control of Afghanistan as city after city, including Kabul, surrenders to the militant group at a pace that foreign policy ‘experts’ could never have imagined. In the words of one commentator this weekend, “The battle was over before it even began.” The Taliban has gained control of the country’s borders, so the only way out now is the Kabul airport which has been flooded with people seeking to exit, including the US embassy. There have been reports of shots fired at people running to the airport, and pictures of desperate Afghanis and foreign nationals climbing onto moving planes shows the desperation among those seeking an exit. What ultimately unfolds in the country is anyone’s guess at this point, but after nearly 20 years of involvement, it doesn’t look like the US has much to show for its efforts. From a market perspective, this weekend’s events are certainly having some impact this morning, and while there may be long-term macro implications down the road, these kind of immediate reactions are usually short-lived.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Also, make sure to check out our Daily Sector Snapshot.

We don’t normally use technical analysis on things like interest rates, but we noticed that the recent bounce in the 10-year Treasury yield stalled out right at its 50-day moving average before pulling back quite a bit on Friday after the weaker-than-expected Michigan Confidence release. Remember, sectors like Financials and Industrials have been trading right inline with moves in the 10-year Treasury yield recently.

Want to see more charts and analysis ahead of today’s open? Start a two-week trial to Bespoke Premium and read today’s full Morning Lineup.