Bespoke’s Morning Lineup – 11/3/25 – Nine’s Fine

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It would be a mistake to think something is wonderful just because it looks great.” – Anna Wintour

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last week may have been the peak week of earnings season in terms of the market cap of companies reporting, but we have another busy week in store for investors, and it’s picking up right where it left off last week. Of the companies reporting so far today, 89% have reported better than expected EPS forecasts, and 75% have topped sales forecasts, so you can’t ask for much more than that. Even in terms of guidance, 3 companies have raised forecasts while only one lowered.

In response to the better-than-expected reports, equity futures are also picking up right where they left off last week, as markets look to open the week higher with the Nasdaq leading the way. Today’s positive open for the Nasdaq will be the ninth straight positive start to a week for the index, which is only the longest streak since summer 2024, but still tied for the second longest in the index’s history.

In Asia, Japan was closed for the day, but other indices in the region were broadly higher even as South Korea’s manufacturing PMI moved into contraction territory. In Europe, most manufacturing PMIs were also in line with forecasts, and the STOXX 600 responded by rallying 0.5% while Germany rallied more than 1%.

Outside of equities, the 10-year yield is slightly lower at 4.09% ahead of a busy week for Fed speakers, who have mostly sounded more skeptical of a December rate cut, as concerns over inflation linger even as there are signs that the labor market is stabilizing.

Crude oil prices are essentially unchanged even as OPEC+ announced over the weekend that it would increase output by 137K barrels per day, but then pause those increases beginning in January. WTI is starting the month just over $60 per barrel after declining 2% in October, taking its monthly losing streak to three months.

Gold prices are starting off the month back above $4,000 per ounce as other metals also trade higher, but the troubles for digital gold continue as bitcoin prices trade down close to 2% and barely hangs on to $108K. Ethereum prices are down twice as much as they barely hang on to $3,700.

With just two months left in the year, over the weekend, we looked at asset class performance, country performance, and individual stock performance for October and various other time periods. Make sure to take a look at that rundown of where things stand heading into year-end. Even though the major averages may be looking good, not everything looks great.

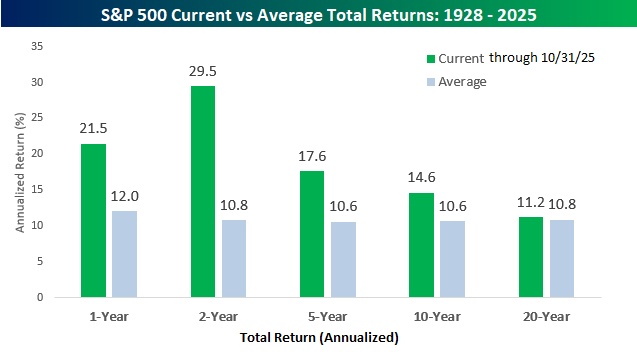

Taking a high-level look at equity market returns, whether you’re looking at the short-term or long-term, it has been a friendly environment. Over the last year, the S&P 500’s total return has been a gain of 21.5% which is nearly twice the historical average of 12.0%, but over the last two years, the 29.5% annualized gain has been nearly triple the long-term average. Looking out over longer-term time periods, though, over the last five, ten, and twenty years, returns aren’t as strong, but they’re still above the long-term average.

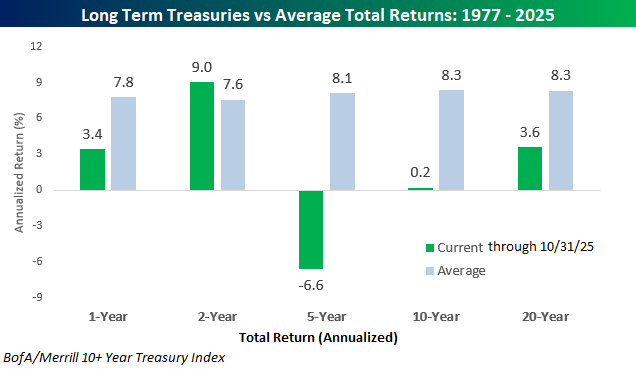

While equity market investors have been on a highway paved in green, the treasury market has been a world of pain. Over the last year, long-term treasuries, as measured by the BofA/Merrill 10+ Year Treasury Index, have posted positive returns, but at 3.4% it’s still less than half of the long-term average. Over the last two years, the annualized gain of 9.0% is actually slightly above average. Still, looking back further than that, it’s been a painful five, ten and twenty years for anyone who has loaned money to the US Treasury.

Best and Worst Stocks and ETFs Through October

With just two months left in the year, it’s time to update our asset class performance matrix and highlight the best and worst performing stocks year-to-date.

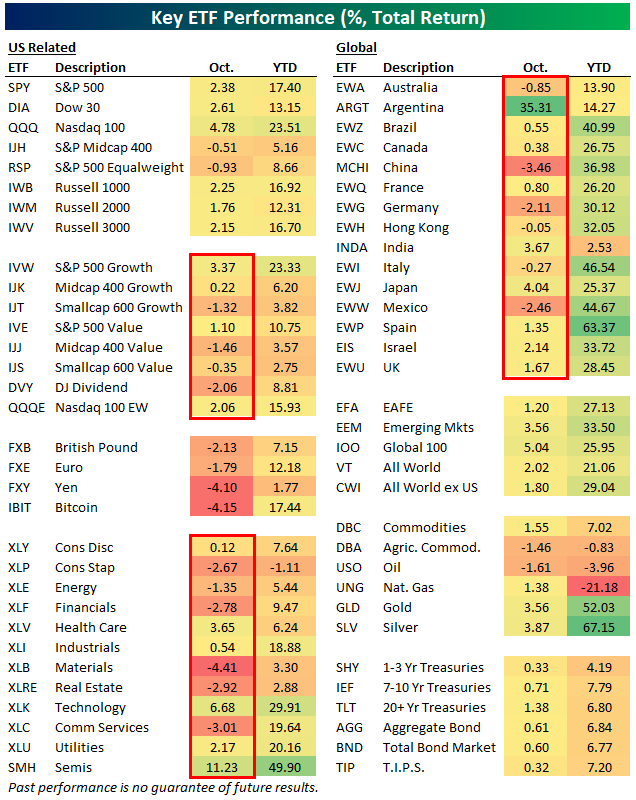

Below is a look at total returns across a range of ETFs both year-to-date and during the month of October.

October was a month dominated by the mega-caps, as they pushed large-cap ETFs like SPY, DIA, and QQQ solidly green, while the equal-weight ETF (RSP) and mid-caps actually fell. Small-cap growth (IJT) and value (IJS) were also red, along with the Dow Jones Dividend ETF (DVY).

Across sectors, more fell in October (6) than rose (5), with Technology (XLK) and Health Care (XLV) the only two big areas of strength.

Outside the US, Argentina (ARGT) rose 35% in October after President Milei’s party maintained control in elections. China (MCHI), Germany (EWG), and Mexico (EWW) were the three worst country ETFs in our matrix during October.

On a year-to-date basis, large-cap domestic ETFs are sitting on solid gains of 15-20%, and the Semis ETF (SMH) is up a whopping 49.9%. Silver (SLV), gold (GLD), and Spain (EWP) are the three best performers in the entire matrix so far in 2025 with 50%+ returns.

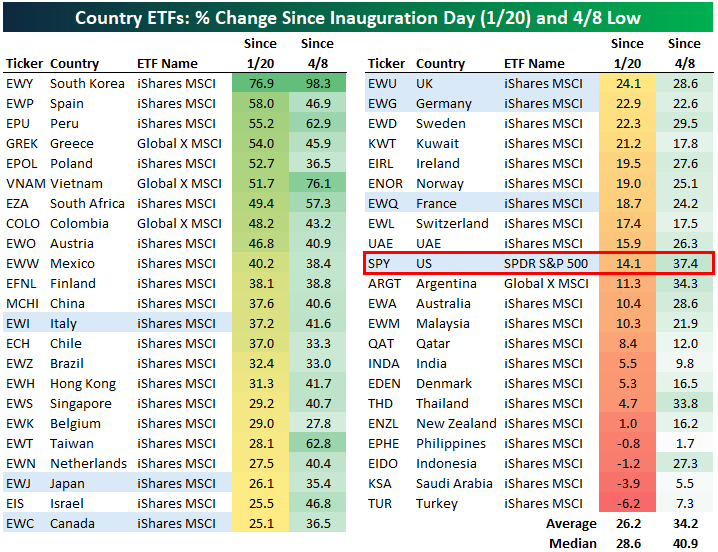

Below is an updated look at performance across a more expansive list of country ETFs since President Trump’s 2nd term began as well as since the “tariff tantrum” lows on April 8th.

The average country ETF is up 34.2% since 4/8 and 26.2% since Trump’s Inauguration on 1/20. The US (SPY) is slightly outperforming since the 4/8 low, but it’s underperforming since Inauguration Day with a gain of 14.1%.

South Korea (EWY), Spain (EWP), Peru (EPU), Greece (GREK), Poland (EPOL), and Vietnam (VNAM) have been the best performers since Trump’s 2nd term began with gains of more than 50%.

There are just four country ETFs in the red since Inauguration Day (Philippines – EPHE, Indonesia – EIDO, Saudi Arabia – KSA, and Turkey – TUR), and every single country ETF is positive since the tariff tantrum low on 4/8.

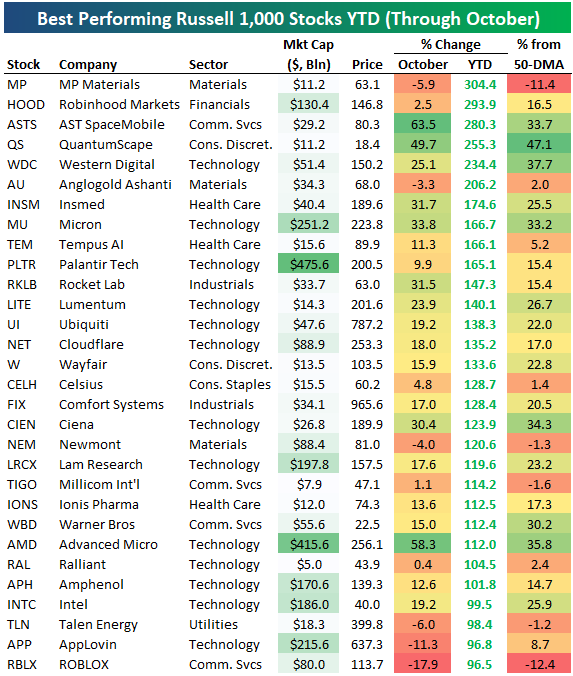

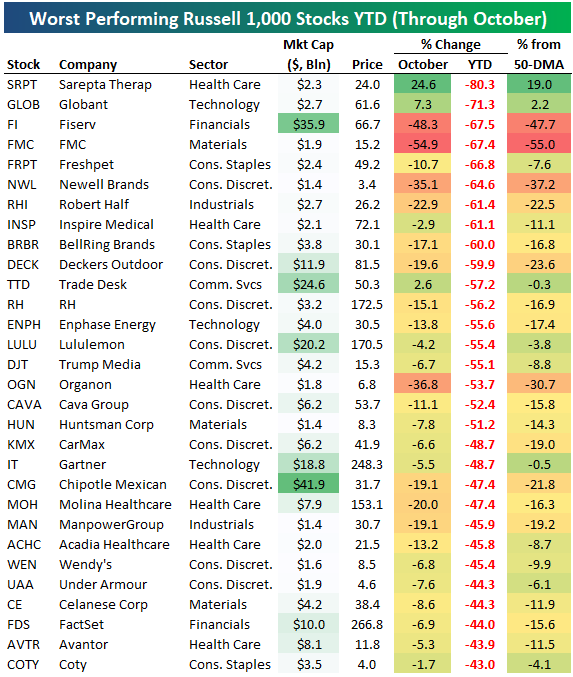

The average stock in the large-cap Russell 1,000 is up 9% year-to-date even though it fell 1% in October.

The tables below show the 30 best and worst performing stocks in the index both year-to-date and in October.

There are 26 stocks in the index up more than 100% year-to-date, along with six that are up 200%, and one that’s up 300%. MP Materials (MP) ranks first with a YTD gain of 304.4%, followed by Robinhood (HOOD), AST SpaceMobile (ASTS), QuantumSpace (QS), and Western Digital (WDC).

Other notables on the list of 100%+ gainers this year include Micron (MU), Palantir (PLTR), Cloudflare (NET), Wayfair (W), Celsius (CELH), Warner Bros (WBD), Advanced Micro (AMD), Intel (INTC), AppLovin (APP), and ROBLOX (RBLX).

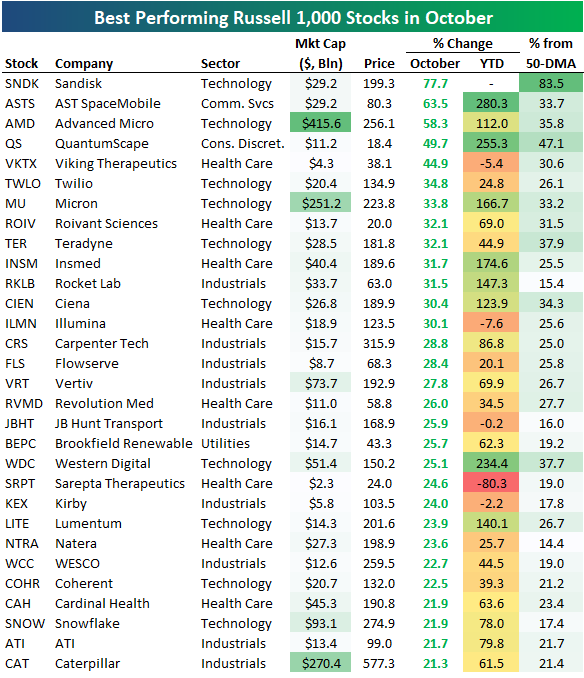

In October, Sandisk (SNDK) was up the most with a gain of nearly 78%, followed by AST SpaceMobile (ASTS) and Advanced Micro (AMD). Other notable winners in October include Twilio (TWLO), Rocket Lab (RKLB), Ciena (CIEN), Vertiv (VRT), JB Hunt (JBHT), Natera (NTRA), and Caterpillar (CAT).

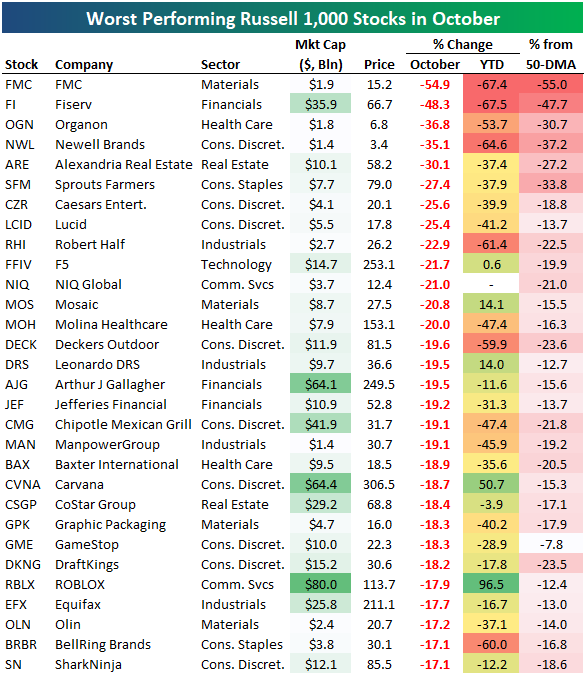

On the flip side, FMC was the worst performing Russell 1,000 stock in October with a decline of 54.9%. Fiserv (FI), Organon (OGN), and Newell Brands (NWL) each fell more than 35% as well.

Some of the biggest names on the list of October losers include Chipotle (CMG), Carvana (CVNA), and ROBLOX (RBLX). RBLX is on the list of October’s biggest losers even though it’s also on the list of 2025’s biggest winners.

Even though it has been a strong year for major cap-weighted US indices, 44.4% of stocks in the Russell 1,000 are in the red on the year. Below are the year’s biggest decliners thus far. W

You won’t find many “AI” names on this list…

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to start receiving our daily emails today!

Brunch Reads – 11/2/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Home Sweet Space Station: On November 2, 2000, the first resident crew arrived at the International Space Station (ISS). Known as Expedition 1, the team consisted of American astronaut William Shepherd and Russian cosmonauts Sergei Krikalev and Yuri Gidzenko. Their arrival was the beginning of a continuous human presence aboard the orbiting laboratory, which has now lasted for decades.

Launched from Kazakhstan aboard a Russian Soyuz spacecraft, the trio docked with the ISS just two weeks after its final pre-crew construction phase. The station was still in its infancy, with just three modules connected together, and basic life-support systems and minimal equipment. The crew spent four and a half months in orbit, getting systems up and running, unpacking supplies from unmanned cargo ships, and preparing the station for the future.

Expedition 1 was a post–Cold War collaboration between the United States and Russia in space exploration. It paved the way for over 200 astronauts and cosmonauts from around the world to live and work aboard the ISS. What began as a small outpost for three men has evolved into one of the most remarkable international scientific partnerships in history, a testament to cooperation beyond borders, orbiting 250 miles above Earth.

Culture & Population Trends

The LL game: the curious preference for low quality and its norms (Sage Journals)

In some Italian institutions, mediocrity can become a social norm, where low-quality work isn’t just tolerated but expected. Those who try to deliver higher quality often face pushback because it disrupts the accepted balance. The study suggests that this creates a stable culture of mediocrity that resists improvement. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – Quarterly Macro Update – 10/31/25

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week we are publishing our quarterly review of global financial markets from a macro perspective, touching on the AI boom and the debt underpinning it, the US economic and Federal Reserve outlook, and snapshots of the Eurozone, Germany, Sweden, South Korea, and China.

Daily Sector Snapshot — 10/31/25

Q3 2025 Earnings Conference Call Recaps: Visa (V)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Visa’s (V) Q4 2025 earnings call.

![]()

Visa (V) operates the world’s largest electronic payments network, connecting more than 4 billion cards, bank accounts, and digital wallets through roughly 12 billion endpoints. The company doesn’t issue cards or extend credit but provides the infrastructure that enables global commerce, handling $14 trillion in payments volume in fiscal 2025. Visa’s fiscal Q4 results showed steady consumer resilience despite global uncertainty. Payments volume rose 9% YoY, cross-border transactions climbed 11%, and value-added services revenue jumped 25%. Management emphasized growth in agentic commerce (AI-powered shopping experiences) and accelerating use of stablecoins for settlement and cross-border money movement. Tokenized transactions now exceed 16 billion, and Visa is enabling banks to mint and burn stablecoins. Tap-to-pay reached 79% of global face-to-face transactions, while Visa Direct volumes surged 27%. CEO Ryan McInerney called Visa a “hyperscaler” for the payments ecosystem, integrating AI across all operations heading into a year boosted by the Olympics and FIFA World Cup. Shares fell 1.8% on 10/29 despite EPS and revenue beats…

Continue reading our Conference Call Recap for V by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q3 2025 Earnings Conference Call Recaps: Caterpillar (CAT)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Caterpillar’s (CAT) Q3 2025 earnings call.

![]()

Caterpillar (CAT) is the world’s largest manufacturer of heavy equipment used in construction, mining, energy, and transportation. Its signature yellow machines (excavators, dozers, trucks, and engines) are sold through a global dealer network that serves infrastructure builders, miners, energy producers, and industrial operators. Beyond machines, Caterpillar’s engine and power systems businesses, including Solar Turbines. Caterpillar reported a record backlog of $39.8 billion, fueled by surging demand for data-center prime power and oil and gas engines. Management highlighted data center expansion tied to AI as a major driver for power generation orders, with long lead times now emerging for large turbines. Tariff headwinds reached the top end of estimates ($500–$600 million) but were partly offset by stronger E&T (Energy & Transportation) margins. North American construction remained firm on IIJA (Infrastructure Investment and Jobs Act) projects, while Asia-Pacific softened outside China. Resource Industries saw continued capital discipline despite healthy mining truck orders and rising adoption of autonomy. On better-than-expected results, CAT shares rose 11.6% on 10/29…

Continue reading our Conference Call Recap for CAT by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

What Volatility?

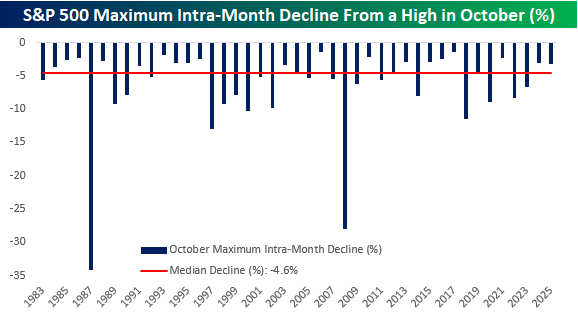

October is winding down, and while investors braced for volatility this month, they got off relatively easy. From its MTD high (at the time) on 10/9 to its intraday low on 10/10, the S&P 500’s maximum drawdown from a high was 3.16%, While last October’s maximum drawdown of 2.99% was smaller, this month’s max decline was 1.44 percentage points less than the median maximum drawdown of 4.60% seen during the month dating back to 1983, which is as far back as we have intraday price history for the S&P 500.

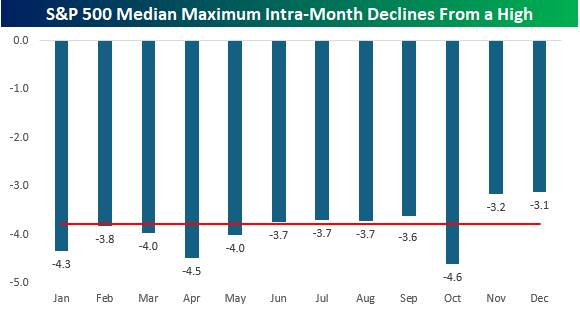

October is known as the most volatile month, and history backs that up. As shown in the chart below, no other month has experienced a larger median maximum drawdown. Somewhat surprisingly, though, April at -4.5% and January at -4.3% aren’t far behind. What makes the month seem even more volatile than it is, though, is that for anyone who has been around a while, two of the three largest intra-month drawdowns from a high have both occurred in October. In 1987, the S&P 500 declined by more than 34% from peak to trough, while in 2008, it plunged by 28%. The only other months with an intra-month decline of more than 25% were March 2020 (-30.12%) when Covid shut down the economy and November 2008 (-26.45%) during the Financial Crisis. It isn’t always a crazy month, but when it is, October sure knows how to disappoint!

Not a Bespoke client? We’d love for you to give our equity research platform, Bespoke Premium, a try. You can sign up for complimentary access for 14 days at this link to start receiving our daily emails today!

The Triple Play Report — 10/31/25

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 20 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

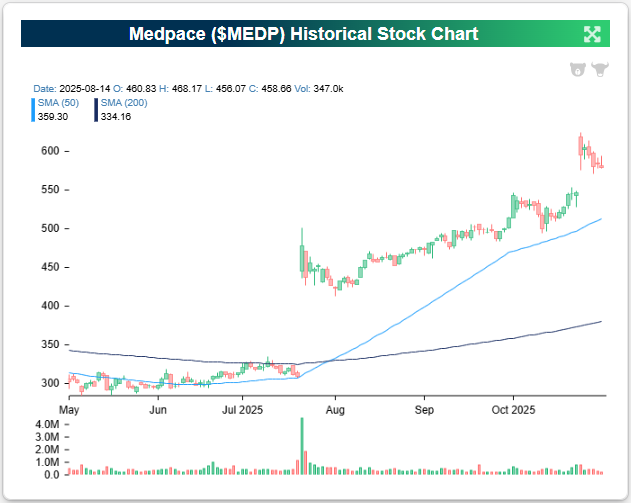

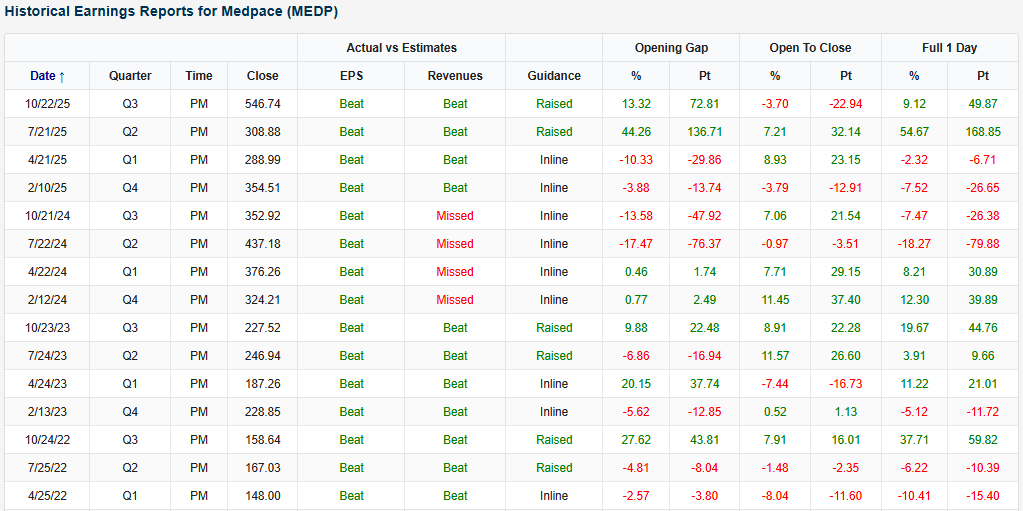

Medpace (MEDP) is an example of a company that recently reported an earnings triple play after the close on 10/22. MEDP reported its second straight triple play, and the stock was up 9.1% on 10/23. After the previous quarter’s triple play report, the stock skyrocketed 54.7%! It hit another all-time high after its latest triple play and is up 74.7% YTD.

Here’s how AI describes the company: Medpace (MEDP) is a global clinical research company that helps biotech and pharmaceutical firms bring new drugs to market by managing every stage of the clinical trial process. The company handles trial design, patient recruitment, site coordination, data analysis, and regulatory submissions under one roof, which gives it tight control over quality and timing. Its work spans a range of therapeutic areas but has become especially concentrated in metabolic disease, oncology, and cardiovascular trials, with a growing portion of business tied to obesity and GLP-1 drug development. A large part of its future revenue comes from its “backlog” of awarded projects that have yet to start, giving strong visibility into client demand.

Medpace’s quarter showed how it is benefiting from the surge in obesity and metabolic disease drug development, which has become one of the hottest areas in biotech. Revenue climbed 23.7% to $659.9 million as the company managed a growing volume of late-stage GLP-1 studies, which are larger, faster-paced, and more expensive to run because of high site and investigator costs. After several quarters of disruption from study cancellations, management said the environment has improved sharply, with fewer cancellations and more consistent client funding. That allowed the value of awarded but not-yet-launched projects to grow 30% from last year, positioning the company for continued growth as those trials move into active enrollment. Hiring was strongest in the US, where most GLP-1 trials are based, and India remains a key location for back-office and data work as Medpace scales up to meet record demand.

Looking at the snapshot below from our Earnings Explorer, Medpace (MEDP) has started to find its footing again after hitting somewhat of a rough stretch in 2024, headlined by revenue misses and heavy declines for the stock after reporting. In the last year, though, MEDP has been consistent with EPS and revenue beats, and with two recent triple plays, investors are coming back around to the stock. Historically speaking, MEDP has been a reliable earnings bet against estimates, with EPS and revenue beat rates going back to 2016 of 89% and 78%, respectively, which are both meaningfully above average.

You can read more about MEDP and the 21 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 10/31/25 – No Scares From the Mega Caps

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The work of today is the history of tomorrow and we are its makers” – Juliette Gordon Low

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view yesterday’s CNBC interview talking about market breadth, click on the image below.

The S&P 500 heads into today with just fractional gains for the week, but today’s trading should add to those gains with futures indicated 0.7% higher. Strong earnings from the mega-caps are to thank for the gains, as what has already been a positive earnings season continues. Outside of equities, treasury yields are slightly higher, while crude oil trades slightly lower but has hung on to $60 per barrel for now. Metals prices are mixed as gold hangs on to $4,000 while silver and copper are essentially unchanged. Crypto is showing some life as Bitcoin trades higher by 3% and Ethereum rallies closer to 5%.

In Asia overnight, markets were mixed. Japan, China, and South Korea all closed out the week higher and with solid gains for the week, but Hong Kong and India were both lower. The biggest economic datapoints of the session were PMI readings in China as the Manufacturing index slid further into contraction territory while the Services component barely stayed out of contraction (50.1).

In Europe, there’s another negative bias with the STOXX 600 down 0.4% as an index of inflation expectations showed a modest uptick from 2.0% to 2.1% for 2025. It wasn’t all bad news, though, as 2025 GDP growth forecasts also showed a modest uptick from 1.1% to a still anemic 1.2%. The higher inflation expectations were also accompanied by an uptick in headline CPI to 0.2% m/m from September’s rate of 0.1%.

Apple (AAPL) and Amazon.com (AMZN) rounded out the group of mega-caps reporting this week with earnings releases after the bell Thursday. Shares of Apple (AAPL) are poised to gap up over 2% at the open, but the real standout is Amazon.com (AMZN). While investors worried that the company’s layoff announcement earlier in the week was a precursor to a weak report, AMZN eased those fears with strong numbers across the board, and in response, shares spiked more than 10%.

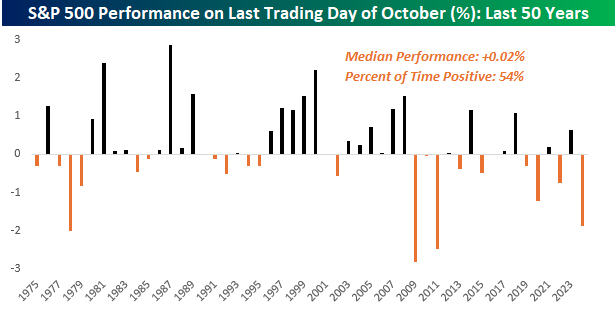

Today is Halloween and the last trading day of October, so can investors expect a trick or a treat? Over the last 50 years, it’s been a bit of a coin flip. As shown in the chart below, the S&P 500’s median performance on the last trading day of October has been a gain of 0.02% with positive returns 54% of the time. In terms of volatility, the median absolute daily change on these days has been 0.50%.

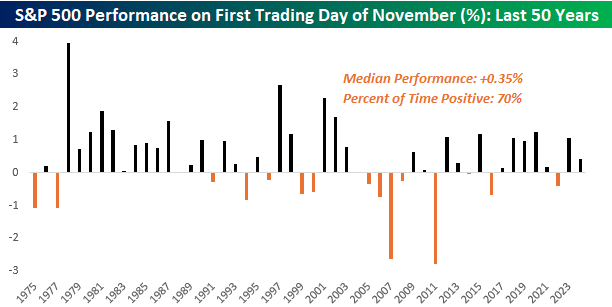

While the last day of October has been relatively uneventful in terms of returns, November typically starts on a more positive note. Over the last 50 years, the S&P 500’s median gain has been 0.35% with gains 70% of the time. And while October is a month known for its volatility, with a median absolute daily change of 0.77%, the first trading day of November has been more volatile than the last day of October.