Bespoke’s Morning Lineup – 2/16/22 – Retail Sales Lead a Busy Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Swim upstream. Go the other way. Ignore the conventional wisdom.” – Sam Walton

Retail Sales were just released and came in much stronger than expected at the headline level (3.8% vs 2.0%). Backing out Autos and Gas, the numbers were even stronger relative to expectations. Last month’s report was revised lower than originally reported but not by enough to offset this month’s strength. Other data released this morning includes Import and Export Prices, and both of those were also stronger than expected. Still on the calendar today, we have Industrial Production (9:15), Capacity Utilization (9:15), Business Inventories (10:00), and Homebuilder Sentiment (10:00). Then at 2 PM we’ll see a release of the Minutes from the January meeting.

Futures have seen a bit of a bounce in reaction to news but are still indicated to open modestly in the red.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Yesterday was just the third time in 2022 that the S&P 500 tracking ETF (SPY) traded in positive territory from the opening to the closing bell, and over the last 50 trading days, there have been just eight times where the S&P 500 traded higher all day. As recently as 2/1, though, the trailing number of times over the last 50 trading days that the SPY traded higher all day was at just six which was the lowest reading since March 2018. What’s even more notable is that back in early December, just as Powell was retiring the term transitory, the 50-day reading of the number of trading days that SPY traded in positive territory for the entire trading day reached a record high of 20. In other words, there’s been quite a reversal in the last three months where the market has frequently opened higher and stayed there to more a of choppy environment where the market has jumped between gains and losses throughout the trading day.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 2/15/22

Bespoke Stock Scores — 2/15/22

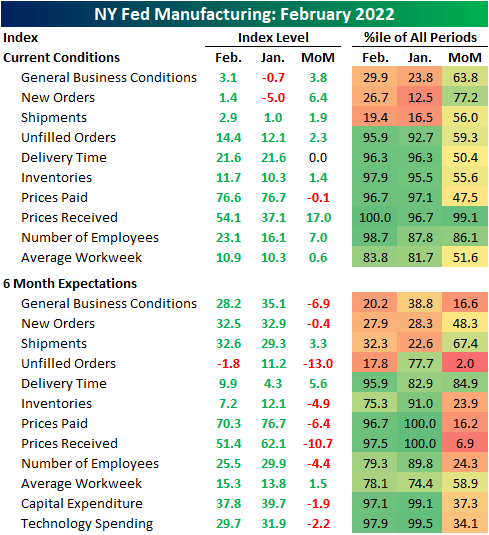

Empire Fed Back In Expansion

The New York Fed released the February results of the Empire Fed Manufacturing survey this morning. Last month saw the index fall into negative territory for the first time since June 2020. This month, the headline number is back into expansionary territory rising to 3.1.

As the region’s activity is once again expanding, most areas of the report showed improvement. New Orders are once again growing alongside shipments, although each of those indices are at the lower end of their historical ranges. Other areas are much more elevated with Prices Received even setting a new record high. Six-month expectations saw weaker breadth in February and are generally at lower levels with respect to their ranges.

Similar to the headline number, New Orders went from a negative reading to a positive one in the past month after rising 6.4 points. Unfilled Orders picked up in tune with a 2.3 point increase to 14.4 which was the highest reading since October. Expectations, however, experienced a dramatic 13-point decline ranking in the bottom 2% of all monthly moves. That marked the largest one-month drop for the index since June 2016.

The index of Delivery Times went unchanged at 21.6. Without any change, the index remains historically elevated but significantly improved versus the record highs in the fall. In other words, supply chains continue to show historic strain, but it appears to have alleviated to a degree.

Although the decline was small at just 0.1 points, Prices Paid fell for the third month in a row. In spite of having peaked, the index remains very high. Contrary to the move in Prices Paid, Prices Received surged from 37.1 in January to 54.1 this month. That wasn’t only a record high for the index, but it also marked the largest one-month gain in a decade.

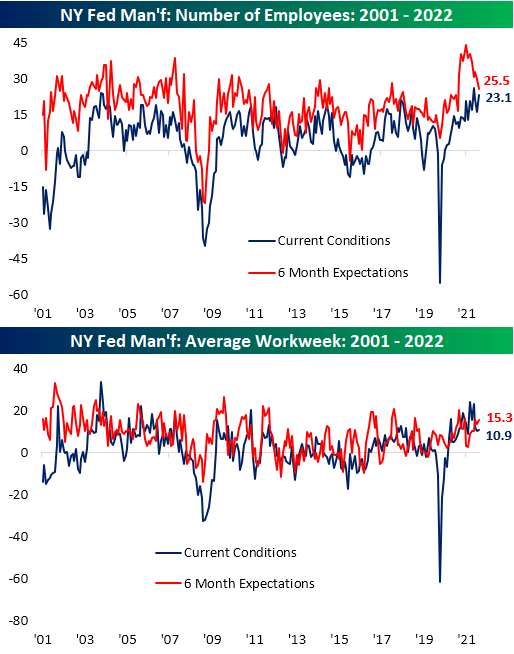

The employment situation also improved with the index for Number of Employees edging higher indicating the region’s firms took on more workers at an accelerated rate. Average Workweek meanwhile saw a small move only rising 0.6 points. Click here to learn about Bespoke’s stock market research services.

Chart of the Day: Highly Shorted Names Keep Falling

Revisiting the Biggest Winners and Losers Since the COVID Crash Low

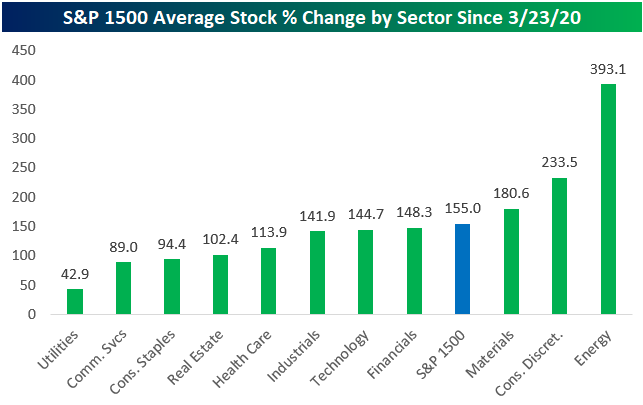

In a little over a month on 3/23/22, we’ll be exactly two years removed from the stock market’s COVID Crash closing low. Below we show how the average stock that’s currently in the S&P 1500 has done since the 3/23/20 low by sector. Stocks in the S&P 1500 are up an average of 155% since the COVID Crash low. By far the best performing sector has been Energy where the average stock is up 393%. Consumer Discretionary stocks are up the second most on average at +233.5%, while Materials stocks rank third with an average gain of 180.6%. Notably, stocks in the Financials and Technology sectors are both up roughly the same on average since 3/23/20 with gains of 148% and 145%, respectively. Three sectors have average gains of less than 100%: Consumer Staples (+94.4%), Communication Services (+89%), and Utilities (+42.9%). Note that these results are only based on price change, so higher dividend-paying sectors like Utilities are up more on a total return basis.

There are currently 59 stocks in the S&P 1500 up more than 500% from their closing level on 3/23/20, and there are 11 up more than 1,000%. GameStop (GME) remains at the top of the list with a gain of 3,042%, followed by SM Energy (SM) and Matador Resources (MTDR) with gains of more than 2,000%. Aluminum-maker Alcoa (AA) is the best performing Materials stock on the list with a gain of 1,160% since 3/23, rising from $5.67/share up to $71.45 as of this morning. The average share price of the 11 stocks that are up 1,000%+ was just $4.42 on 3/23/20. Their average share price now is $66.78!

Tesla (TSLA) is by far the largest company on the list of best performers with a market cap of more than $900 billion at the moment. Back on 3/23/20, Tesla (TSLA) shares closed at $86.86. Since then, the stock has gained 944%, putting shares above the $900 level.

There are 56 stocks currently in the S&P 1500 whose price today is lower than it was at the close on 3/23/20. Below are the 35 stocks that are down at least 10% in price since then. eHealth (EHTH) and Tabula Rasa (TRHC) have been the worst two with declines of more than 80%. Another three are down more than 50% (QURE, STRA, IVR), while 16 more are down 20%+. The two stocks on the list of worst performers with the largest markets caps at the moment are Gilead (GILD) and Biogen (BIIB). These two stocks performed well in the very early days of COVID, but they’ve been trending lower ever since and currently trade at the same levels they were at in mid to late 2019.

Clorox (CLX) is an interesting name to see on the list of worst performers. When COVID first hit, there was a run on disinfectant products like bleach that Clorox manufactures. (Remember trying to find Clorox wipes throughout the first half of 2020? They were nowhere to be found!)

The supply/demand imbalance pushed shares of Clorox (CLX) sharply higher from January to August 2020, but since then shares have steadily trended lower and lower, and they’re now right back to where they were trading in early January 2020. Normally, we see stocks “take the stairs up and the elevator down,” but the two-year chart for Clorox looks like the opposite: it took the elevator up when COVID first hit, and it has taken the stairs down ever since. Click here to view Bespoke’s premium membership options.

B.I.G. Tips – ‘Cheap’ Stocks With Assumed Growth

Bespoke’s Morning Lineup – 2/15/22 – On Again, Off Again

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“What we know is a drop, what we don’t know is an ocean.” – Isaac Newton

Investors have breathed a sigh of relief this morning on headlines that some Russian troops on the border of Ukraine are starting to return to their bases. Setting aside the fact that it wouldn’t make a lot of sense to take comments from a would-be invader seriously, investors will take any positive news while they can get it. The bottom line is that like the quote above, there is much more we don’t know about the situation at hand than what we do know, and that doesn’t even include the FOMC and the state of the US economy. On the latter, the economic calendar starts to pick up today and for the rest of the week. Today’s reports include PPI and Empire Manufacturing which will both be released at 8:30. For our first take on the data, make sure to listen to our Twitter Spaces where we will break it all down.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

A potential easing of Russia-Ukraine tensions has caused WTI crude oil prices to fall over 3% from yesterday’s close to the lowest levels since – hold on for it – last Friday. With energy prices lower, you would expect Energy stocks to show weakness today, and that’s exactly what we’re seeing in the pre-market with the Energy Select Sector ETF (XLE) trading down nearly 2%. While the positive correlation between crude oil prices and energy stocks is holding up so far today, we would note that in yesterday’s trading the two traded inverse with each other as WTI traded up over 2% while energy stocks traded down more than 2%. That was the first time in over a year that energy stocks were so weak on a day that crude oil was up over 2%.

Despite yesterday’s inverse trading, crude oil and energy stocks have been joined at the hip for the last year. Through the close yesterday, WTI was up 59% over the last year while the Energy sector was up 53%. While those performance numbers are already similar to each other, before Monday’s divergence, less than one percentage point separated their performance over the trailing twelve months. If tensions over Ukraine do in fact ease over the coming days, look for energy prices and therefore energy stocks, to take a breather from their torrid performance this year.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.