Chart of the Day: Less Consumer ‘Calls’ to Dealer ‘Raises’

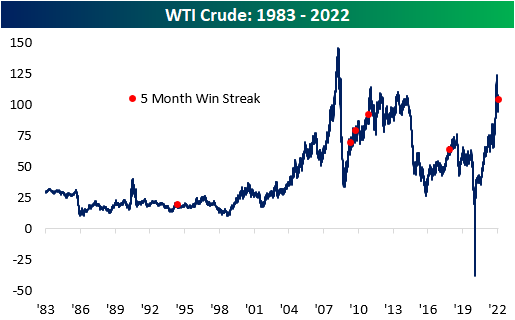

WTI Monthly Win Streak

It’s been a monster year for cruse oil and it continued in April. For the month, WTI rallied 4.4% and finished the month at $104.7 per barrel. This comes as Russian supply has been essentially cut off from Western markets, the Saudis hold back supply, and US drillers are in the process of ramping up capacity to meet demand, which is a process that takes several months to complete. Most notable about April’s rally was that it marked the fifth consecutive month in which WTI rallied, which is tied for the second-longest streak on record (since 1983). The only streak that was longer was in late 2010/early 2011 when WTI notched eight straight months of gains.

The chart below outlines the long-term price chart of WTI Crude. Two aspects stand out in the chart. First, crude oil tended to see additional gains in the short term following these five-month streaks. Secondly, it is also worth noting that three of these occurrences happened within two years (2009 – 2011), which was likely due to aggregate demand ticking higher as the economy emerged from the Global Financial Crisis. The current period is relatively similar, as the global reopening has put upward pressure on the demand curve after oil producers lowered output during COVID. That increased demand has also been exacerbated by supply constraints following the Russian invasion of Ukraine.

The table below outlines the performance of WTI after the fifth straight month of prior five-month win streaks. WTI tended to trade down over the following month but reversed course to book gains in the following three and six months. In the month following these streaks, WTI averaged a loss of 4.4% (median: -4.8%), booking gains just one time (20%). After three months, WTI averaged a gain of 5.1% (median: 5.5%), performing positively 80% of the time. Over the next six months, average performance and positivity rates declined to 1.9% and 60%, respectively.

Higher oil prices affect energy prices, shipping rates, and the cost of so many more secondary products. Therefore, higher oil prices tend to be inflationary and crimp corporate margins as well as consumer buying power. Historically speaking, though, the S&P 500 has averaged a gain of 8.3% (median: 12.1%) during these streaks, which is 420 basis points higher than the average performance for all five-month periods since 1983. In the month following these streaks, the S&P 500 has averaged a gain of 1.4% (median: 3.2%), which is higher than the historical average as well. In the next three months, the index has averaged a gain of 4.5% (median: 4.9%) with positivity rates higher than that of all periods. Similar to what we see in the six-month performance of WTI, positivity rates moderate for the S&P 500, with average six-month gains of 3.2% (median: 0.2%) versus around 5% for all six-month periods since 1983. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 5/2/22 – New Month, Same Market

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Take a simple idea, and take it seriously.” – Charlie Munger

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Futures were modestly positive for most of the overnight session but have weakened as we get closer to the opening bell. After a day like last Friday, it’s all but guaranteed that we’re likely to see continued volatility today. As they say around the roulette wheel, “Round and round it goes. Where it stops nobody knows.”

Economic data at 10 AM will also be a big factor in where the market trades today, but the looming Fed meeting mid-week will be on everyone’s mind. While the current rate hiking cycle has already been called the most aggressive in a generation, it’s important to remember that the Fed has only hiked 25 bps so far. That will change this week as a hike of at least 50 bps is pretty much fully priced in. The most ironic aspect of it all, though, is that after months of delay, the Fed is starting to ramp up the pace of hikes just after a negative Q1 US GDP print, slower than expected economic data, and even weaker data in China and Europe.

In today’s Morning Lineup, we recap overnight events in Asia and Europe (pg 4), economic data in China and Europe (pg 5), as well as a recap of PMI data for April (pg 6).

It’s often said that the stock market is one of the only places where investors don’t like bargains. In other words, when the market is rallying investors love stocks, but when it declines, investors can’t get out fast enough. Warren Buffett is one investor who has bucked the conventional approach of many investors and consistently used weakness as an opportunity. His actions in Q1 were a perfect example. In this weekend’s annual meeting, one slide that stood out was the breakdown of Berkshire Hathaway’s equity purchases during the quarter. Of the nearly $52 billion in purchases made by Berkshire in Q1, just under 80% of it occurred during the highlighted period in the chart (from 2/21 through 3/15) when prices in the quarter were at their weakest.

It’s also worth keeping in mind what Berkshire was buying during the quarter. It wasn’t growth stocks that were down the most. Instead, it was mostly in stocks with reasonable valuations like Chevron (CVX). Occidental (OXY), Alleghany (Y), HP (HPQ), and even Apple (AAPL).

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Berkshire’s Annual Conference

Warren Buffett’s Berkshire Hathaway (BRK/B) is hosting its annual investor conference this weekend, and investors who don’t make the pilgrimage to Omaha will tune in from around the world to hear Buffett and Munger provide their insights into the economy and the market. You can tune in here. We often hear that Berkshire’s stock gets a lift coming out of the annual meeting, but a look at the stock’s performance leading up to and after the annual meeting suggests otherwise.

Over the last 20 years, BRK/B stock has averaged a gain of 1.0% (median: 80 bps) in the week leading up to the meeting with gains 71% of the time. That average is higher than the average of all periods by a factor of just over four, with positivity rates 18 percentage points higher than that of all periods.

Immediately coming out of the conference, Berkshire has also tended to get a lift with the stock averaging a gain of 40 bps (median: 80 bps) the day after the conference, but that bounce didn’t tend to last long. As shown in the table, on both an average and median basis, returns over the following week were lower than the following day. Buffett would be the last person to advocate a strategy of short-term trading of Berkshire stock, so it’s only fitting that there isn’t a clear pattern of performance leading up to or immediately after his annual “Woodstock for Capitalists”. Click here to view Bespoke’s premium membership options.

Historic End to a Down Month

It was a rough finish to the month of April. Not only did the S&P 500 (SPY) finish the month with an 8.78% decline month to date, the biggest one-month decline since March 2020, but the last trading day of the month was one for the record books. Since SPY began trading in 1993, the only bigger drop on the final trading day of the month was in August 1998. Back then it was a much larger 7.13% decline.

In the table below, we show all months since 1993 that SPY declined at least 2% on the last trading day of a month. Behind April, the next worst final day of a month and the only other month with an over 3% decline was September 1998, but back then, SPY had still managed to finish up MTD. Finishing up MTD has been the exception rather than the rule of these occurrences, though, as November 1998 and October 2011 were the only other times that SPY fell over 2% on the last trading day of the month but still finished with a MTD gain.

As for where the S&P 500 has typically gone from there, the first trading day of the new month has only seen a move higher 46% of the time as the index has averaged a 30 bps decline. For the full month, though, performance is generally more positive with an average gain of 2.75% and positive returns almost 70% of the time. Click here to learn more about Bespoke’s premium stock market research service.

The Bespoke Report – 4/29/22 – Is That Blood in the Streets?

This week’s Bespoke Report newsletter is now available for members.

An appointment for a root canal has sounded better than having to watch this stock market lately. Just when you think things can’t get any worse in this market, they do, as every bounce has been quickly repudiated with stocks grinding down to new lows for the year.

It’s never a good feeling when equities close out the week at their lows, but we’ve now had that happen two weeks in a row. The S&P 500 has now declined at least 1% for four straight weeks while the Nasdaq has been down at least 2.5% for four straight weeks. Since 1971, there have only been four other times where the Nasdaq experienced a similar streak, so this kind of persistent weakness doesn’t occur very often.

When the markets start acting like this, it’s incredibly difficult to make any sense of the day-to-day moves, so for us or anyone to say anything about what to expect in the short-term would be foolish. Long-term investors have experienced worse and the market will eventually turn, but until it does, that root canal doesn’t look all that bad.

The snippet above is pulled from a page from this week’s Bespoke Report newsletter. If you’re not a Bespoke subscriber and you want to read this week’s full Bespoke Report (and access everything else Bespoke’s research platform has to offer), start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 4/29/22

Amazon (AMZN) Shares Now Barely Up Post-COVID

Amazon (AMZN) was one of the primary beneficiaries of the pandemic as consumers were forced to engage in commerce digitally and corporations became increasingly willing to migrate to the cloud. In the first year or so after the March 2020 COVID Crash, AMZN shares soared from $2,000 up to $3,700. Since peaking in mid-2021, however, it has been a different story. Since AMZN reported earnings last night, shares have fallen another 15%. This leaves AMZN up just 13.5% from the level it was trading at right before the pandemic began on 2/19/20.

Although the stock is now barely higher versus pre-COVID levels, revenues continue to climb. Relative to pre-pandemic levels, trailing 12-month revenues have increased by 70.3% (CAGR of 27.2%). As implied, the price to sales multiple has compressed considerably relative to pre-pandemic levels. At the highs, AMZN was trading 3.8 times sales. The highest P/S multiple for the stock since the start of 2020 occurred in September of 2020, when the multiple hit 5.5. As it currently stands, the price to sales multiple is at new lows relative to the start of 2020 at just 2.7.

While AMZN revenues are up 70% from pre-COVID levels, margins have compressed considerably. In Q1 2020, AMZN posted operating margins of 9.5%. In Q1 2022, AMZN reported operating margins of 3.2%. These results can be attributed to inflationary pressures, labor challenges, supply chain constraints and foreign exchange headwinds. As you can see in the chart below, margin compression has hampered EPS, resulting in a decline in trailing 12-month EPS over the last three quarters. Relative to pre-pandemic levels, EPS have risen by 52.5% (CAGR: 21.1%), but they’ve declined by 38.8% over the last three quarters. Click here to become a Bespoke Institutional subscriber and gain access to our Conference Call Recaps.

Bespoke’s Morning Lineup – 4/29/22 – Amazon Fails to Deliver

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “Risk comes from not knowing what you’re doing.” – Warren Buffett

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

It’s not looking like a positive close to the week with futures solidly in the red following negative reactions to earnings from Amazon.com (AMZN) and Apple (AAPL). With the Fed announcement looming next week, investors are likely to be a bit apprehensive ahead of the meeting.

In terms of economic data, the week is closing off on a busy note. Employment Cost Index for Q1 came in much higher than expected at 1.4% compared to forecasts for an increase of 1.1%, and it was the highest level since at least the mid-1990s. Personal Income and Personal Spending also topped expectations. Still upcoming, we’ll get an update of Chicago PMI at 9:45 and Michigan Sentiment at 10 AM.

In today’s Morning Lineup, we recap overnight events in Asia and Europe (pg 4), inflation in Europe (pg 5), and prior quarters whereAMZN gapped down sharply in reaction to earnings (pg 5).

It’s been quite a week for US stocks. While both the Russell 2000 (IWM) and Nasdaq 100 (QQQ) made marginal new lows this week, the S&P 500 (SPY) managed to hang on to its lows from earlier this year. The fact that equities were quick to bounce following those breakdowns was encouraging, but with futures in the red to kick off the last trading day of the month, these will be critical levels to watch throughout the day.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.