Chart of the Day – Bonds Break

Daily Sector Snapshot — 4/11/22

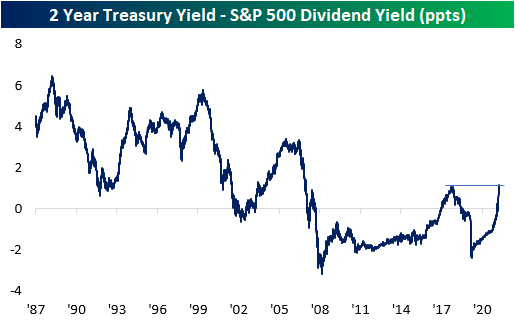

BABY’s Back

Since mid to late-2019 when interest rates really started to fall, the dividend yield on the S&P 500 consistently provided a higher yield than the two-year US Treasury. With a higher payout plus the potential for price appreciation, equities looked more attractive to many investors. The period from the Financial Crisis through 2017 also saw a similar setup where the S&P 500’s dividend yield was higher than the yield on the 2-year, but before the Financial Crisis and the FOMC’s zero-interest-rate policy, it was extremely uncommon for the S&P 500 to yield more than the two-year Treasury. This year has caused a tidal shift in the balance of power in yield between the S&P 500 and the two-year Treasury. As the Fed came to the conclusion that inflation wasn’t as transitory as originally thought and found itself behind the inflation curve, it shifted from a much more accommodative stance to one that was more biased towards tightening, and that shift resulted in one of the most rapid increases in two-year Treasury yields in decades. In the process of this spike in rates, back in February, the yield on the two-year rose back above the dividend yield of the S&P 500 for the first time since 2019.

As Treasury yields have continued to spike, the premium in yield of two-year Treasuries relative to the dividend yield of the S&P 500 reached an important milestone last Friday (4/8). As shown in the chart below, the spread between their yields widened out to 110 basis points (bps), taking out the high of 108 bps from 2018. At these levels, the spread between the two is now the widest it has been in fourteen years since the Financial Crisis. It started with long-term Treasury yields, but as the overall trend in rates has been higher, most of the Treasury yield curve is now yielding more than the S&P 500. For years now, investors have had a TINA (There Is No Alternative) relationship with the stock market, but as interest rates have shot higher, TINA is taking a backseat to BABY (Bonds Are Better Yielders). Click here to try out Bespoke’s premium research service.

B.I.G. Tips – Earnings Season Ahead

Earnings season kicks off this week as the major banks and brokers start to report their first-quarter numbers. BlackRock (BLK) and JP Morgan Chase (JPM) will kick things off on Wednesday, followed by Citigroup (C), Goldman Sachs (GS), and Morgan Stanley (MS) leading the charge on Thursday. On Friday, the equity market is closed in observance of Good Friday, but Bank of America (BAC), Bank of New York (BK), and Charles Schwab will all report next Monday (4/18). While it will be a busy few days for Financials, the heart of earnings season doesn’t really get rolling until later this month. The five largest companies in the S&P 500 (AAPL, AMZN, FB, GOOGL, and MSFT) won’t report until the last week of April.

For a more detailed rundown of the earnings schedule for the upcoming season, please see our Earnings Explorer Tool (available to all Institutional clients) on the Tools section of our website, and to see our quarterly preview of the upcoming earnings season with respect to analyst sentiment heading into it, start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Defensives Propping Up New Highs

The S&P 500 has fallen in four of the past five sessions continuing to pull back from its lower high, but surprisingly, the net percentage of the index hitting new 52-week highs actually saw one of the strongest readings of the year on Friday as we show in the chart from our Sector Snapshot below. To cap off last week, a net 11% of S&P 500 stocks were at new 52-week highs; the highest reading since January 5th which was only a couple of days after the index’s last all-time high. Typically, we look at net new highs as a way to confirm moves in the broader market. In other words, it is viewed as better to see a larger number of stocks trading at new highs versus new lows. While net new highs are so far lower today, Fridays’ double-digit positive reading was unusually high for a down day. Historically going back to 1990, the average net new high reading when the S&P 500 has been lower on the day has only been 1.6%. It was even a strong reading compared to the average for up days (4.77%) as well.

As for how new highs have held up relatively well as the broader market has pulled back, defensive sectors—Consumer Staples, Health Care, Utilities, and Real Estate—are almost entirely the ones to thank. To illustrate this, below we show the daily percentage of S&P 500 stocks hitting new highs that are from one of the four defensive sectors just mentioned. There is plenty of precedent in the past several years for these four sectors to account for all of a day’s new highs including several days in late January and early February. At the high last Wednesday, over 90% of S&P 500’s new highs came from defensive sectors. On a 50-DMA basis, this reading is now at the highest level since the spring of 2020.

In other words, defensives have been a notable pocket of strength recently. As for just how large of a run they have been on, in the charts below we show the rolling one month change of these sectors going back to 1990 (2001 for Real Estate). While the rates of change have peaked, Health Care and Utilities are up double digits in the past month while Consumer Staples and Real Estate have risen high single-digit percentage points. For all sectors except for Real Estate, those rallies rank in the top 3% of all monthly moves since 1990 and Real Estates is still in the top decile of all monthly moves going back to 2001. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup – 4/11/22 – Another Case of the Mondays

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You get recession, you have stock market declines. If you don’t understand that’s going to happen, then you’re not ready, you won’t do well in the markets.” – Peter Lynch

It’s another case of the Mondays for US stocks this morning as all three major averages are firmly in negative territory with the Nasdaq leading the way lower. Along with equities, just about every other risk asset is trading lower, including bitcoin and crude oil. Bonds are down again as well, while yields continue to surge in what has been one of the most relentless moves higher in yields that the market has seen in years.

The economic and earnings calendars are pretty much empty today, but things will pick up greatly as the week goes on with a busy slate from Tuesday through Thursday before Friday’s equity market holiday.

Read today’s Morning Lineup for a recap of all the major market news and events from around the world, including the latest US and international COVID trends.

Given the widening lockdowns in China and concerns of a broader economic slowdown, oil prices have been under pressure this morning continuing a trend of weakness from last week. While the week is just a few hours old at this point, WTI is trading below $94 per barrel and in danger of breaking a relatively important support level. At current levels this morning, WTI is pretty much up 24% YTD but down 24% from its closing high in early March.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Disney+ Turns Three

It seems like just yesterday that the streaming market was dominated by a single player: Netflix (NFLX). This dramatically changed when new entrants such as Amazon (AMZN), Paramount (PARA), Comcast (CMCSA), Hulu, and YouTube (GOOGL) helped create a relatively fragmented and competitive market. The conjunction of all of these platforms and a shift in consumer preferences has put pressure on legacy television brands and forced conversion into streaming. Three years ago today, Disney (DIS) announced that their streaming platform, Disney +, would be unveiled just seven months later.

When DIS first announced the launch of its streaming platform, investor excitement was clear, as the stock soared 11.5% the following day, the largest single day upside move since May of 2009. DIS has the ability to source content from its existing brands, such as Lucasfilm, Marvel, ABC, The History Channel, Pixar, 20th Century Studios, A+E Networks, and more. Its unique setup allows the company to produce content from profit generating-entities, and further monetize said content by offering it to consumers on its streaming platform. DIS also owns ESPN and Hulu, which increases the attractiveness of the collective platform as a family package, covering everything from live sports to children’s programming. At the end of fiscal year 2021, Disney+ had 33,000 episodes and 1,850 movies on the platform, bringing the title total to about 35,000. On the other hand, Netflix had 50,000 titles in March of 2020, so DIS is slightly behind in aggregate content relative to the largest competitor in the sector. Since the start of 2020, the number of users on the Disney+ platform has grown at a compounded annual growth rate of 111.1%, growing from 26.5 million in Q1 2020 to 118.1 million in Q4 2021. The most recent quarter (Q4 2021) saw the slowest q/q subscriber growth in both percentage and nominal terms, as the service added just 2.1 million users (+1.8%).

Alongside the subscriber spike has, of course, come a spike in direct-to-consumer revenues realized by DIS. In fiscal year 2021, DIS booked $16.3 billion in revenue from its DTC segment, which was an increase of 54.7% y/y. In fiscal year 2020, DIS recognized a 38.0% increase in subscription revenues. Clearly, this channel has been growing significantly, and the pandemic helped to only propel further. Although this aspect of the business was strong in the midst of the pandemic, losses from cruises, hotels, and resorts hampered earnings results, which resulted in poor equity performance for DIS. Since the start of 2020, DIS has traded down by 10.6%, even as the headwind of COVID restrictions has eased, travel has picked up, and the DTC channel has experienced immense growth.

The relative strength of Disney’s stock has been even bleaker. Since announcing the launch of Disney+, DIS has underperformed the S&P 500 by a wide margin, and the relative strength reading is currently sitting at the lowest level since 2012. In its Q4 2021 earnings report, DIS reported slowing subscriber growth, which caused the relative strength to weaken even further. Moving forward, investors will be keenly aware of the performance of Disney+ as well as the performance of the parks, resorts, and cruises as pent-up travel demand continues to come into the market. Although the launch of Disney+ has gone relatively well, the platform has room to run in terms of penetration, subscriber counts, and international expansion. The stock has not moved in conjunction with subscriber growth as questions over revenues generated per user, a highly competitive streaming space, and the company’s exposure to still-suppressed industries still cloud the outlook. Click here to try out Bespoke’s premium research service.

Bespoke Brunch Reads: 4/10/22

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium with a 30-day free trial!

The Masters

Augusta family next to Masters golf course keeps turning down millions for their 1,900-square-foot house by Cork Gaines (Insider)

The crowds at Augusta National often walk past the Thacker family abode at 1112 Stanley Drive, just across the street from Gate 6A. The Thackers have repeatedly turned down millions for the property. [Link]

Masters 2022: Anything but the green jacket — tales from player shopping sprees by Josh Weinfuss (ESPN)

What’s the point in attending the most exclusive golf tournament in the world if you don’t bring home some swag to prove you were there? [Link]

China

China’s $2.3 Trillion Infrastructure Plan Puts America’s to Shame by Tom Hancock (Bloomberg)

The already investment-intensive Chinese economy is going to plough another $2.3trn into infrastructure to offset slowing property markets and an economy wracked by COVID, high debt, and weak consumer spending. [Link; soft paywall]

Shunned Oil Piling Up Off China as Virus Outbreak Worsens (Bloomberg)

Amidst extreme oil shortages around the global economy, more than 20 million barrels of crude from Russia, Iran, and Venezuela are sitting offshore in China as domestic demand collapses thanks to interventions seeking to contain the spread of COVID. [Link; soft paywall]

Inflation

Shoppers Face ‘Shrinkflation’ at the Supermarket by Donna Fuscaldo (AARP)

In addition to raising the price of goods, companies are also reducing the size of packaged goods without changing the price. This shows up in official inflation measures (because they are adjusted for the weight or volume of a given item) but may sneak up on consumers at the store. [Link]

Inflation fears force Americans to rethink financial choices, CNBC and Acorns survey says by Michelle Fox (CNBC)

A somewhat hard-to-believe 48% of Americans report thinking about rising prices “all the time”. More than half of respondents to a recent survey reported cutting back on dining out, the most common response to inflation reported. Though that’s also tough to square with restaurant spending at a record level in February per BEA data. [Link]

New York

NYC’s Priciest Seafood Spots Skyrocket Further Into the $1,000 Stratosphere by Ryan Sutton (Eater)

Won’t someone think of the Nobu patrons? A dinner for two at Sushi Noz now costs $1k, amidst a wave of higher prices around the highest-end meals in New York City. [Link]

The world’s skinniest skyscraper is ready for its first residents by Lydia Armstrong (CNN)

The Steinway Tower at 111 West 57th is 24x as tall as it is wide, making it the third-tallest building in New York but at 84 stories it will be the most slender tower in the world. [Link]

NYC landlords filing so many eviction cases that firms for low-income tenants have run out of lawyers by Molly Crane-Newman (New York Daily News)

More than 10,000 eviction proceedings were filed in New York during the last two months, on top of more than 200,000 suits filed during the pandemic; there are so many suits that there aren’t enough lawyers to represent all the tenants. [Link; auto-playing video]

Social Studies

U.S. life expectancy falls for 2nd year in a row by Rob Stein (NPR)

Despite the country moving on from the pandemic, thousands of Americans are still dying of COVID, and provisional statistics showed that drove down life expectancy for the second consecutive year in 2021. [Link]

America’s internet is splitting along party lines by Sara Fischer and Scott Rosenberg (Axios)

Investors are betting on durable partisan splits in media consumption, as media consumers gravitate towards similar viewpoints at siloed sites. [Link]

The Workplace

This Is What Happens When There Are Too Many Meetings by Derek Thompson (The Atlantic)

White collar workers are increasingly finding productivity late into the night, with workers increasingly returning to tasks after dinner and before the end of the night. [Link; soft paywall]

“Great Resignations” Are Common During Fast Recoveries by Bart Hobijn (FRBSF)

Fast labor market recoveries generally lead to elevated job turnover, making the much-heralded “great resignation” of the current post-COVID jobs boom wholly unremarkable. [Link]

Bearish Bets

If Stocks Don’t Fall, the Fed Needs to Force Them by Bill Dudley (Bloomberg)

An argument that for the economy to slow as desired by the Federal Reserve, even more shock therapy is needed in the form tighter financial conditions. [Link; soft paywall, auto-playing video]

Crypto

The Metaverse Has Bosses Too. Meet the ‘Managers’ of Axie Infinity by Edward Ongweso Jr (Vice)

A dystopian vision of a crypto-fueled gaming future that outsources the hard work of collecting in-game rewards to workers in the Global South and exposes anybody playing to wild variations in market prices which have nothing to do with underlying game. [Link]

Conspicuous Consumption

The Real Yacht Rock: Inside the Lavish, Top-Secret World of Private Gigs by David Browne (Rolling Stone)

Some of the biggest paydays in music come from private bashes for the world’s wealthy: millions for a single quick show performed to a small private audience. [Link]

Drones

Amazon, Alphabet and Others Are Quietly Rolling Out Drone Delivery Across America by Christopher Mims (WSJ)

Consumers are starting to get deliveries from drones after years of promises that they are right around the corner. Air dropped packages, quadcopter deliveries, and rapid Prime from the sky are all part of the landscape. [Link; paywall]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report – 4/8/22 – Earnings Keep The Market Afloat

This week’s Bespoke Report newsletter is now available for members.

The US equity market is facing big valuation headwinds from rapid shifts in expectations for Federal Reserve policy near-term and a market view that rates will be higher in the long term. With yields surging, the market has relied on ever-higher earnings estimates to stay afloat as we approach Q1 earnings. High earnings estimates make this season a unique risk for the market as the post-COVID bonanza in beats trails off. Foreign central banks are also getting in on the game as interest rates surge into positive territory in the Eurozone. We discuss French elections with the first round of voting this Sunday, as well as touching on policy in Russia and China. Global trade frictions appear to be easing, and used auto prices have started to fall, both of which offer a sunnier picture for inflation. We also look at earnings Triple Plays, credit markets, the strong dollar, the outlook for the Fed’s balance sheet, oil markets, big NASDAQ drops, equity market dividend yields, recession probabilities, and more in this week’s Bespoke Report.

To read this week’s full Bespoke Report newsletter and access everything else Bespoke’s research platform has to offer, start a two-week trial to one of our three membership levels.

Daily Sector Snapshot — 4/8/22

Please click the thumbnail image below to view today’s Daily Sector Snapshot.