Daily Sector Snapshot — 4/27/22

B.I.G. Tips – 100-Day Periods Most Correlated to Today

Chart of the Day – 60/40 Turns to 53/37

Bespoke’s Morning Lineup – 4/27/22 – Happy Birthday Universe!

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “I much prefer the sharpest criticism of a single intelligent man to the thoughtless approval of the masses.” – Johannes Kepler

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

6,999 years ago today, the Universe was born. At least that’s according to German astronomer Johannes Kepler who came to that conclusion in the 1600s. Kepler’s work has been ‘revised’ in the centuries since, and it is now widely agreed that he was off by at least 10 billion years. What’s a few billion amongst friends, though? It just goes to show that facts that people take for granted in one environment can look foolish in another.

Futures are looking to recoup some of yesterday’s losses, but even at their best levels earlier this morning, we weren’t even on pace to recoup half of Tuesday’s losses. Let’s just call it the ‘two steps backward, one step forward market’. There’s been a ton of earnings news since the close yesterday, and the pace will only intensify over the next two days.

The only two economic reports on the economic calendar this morning are Wholesale Inventories which came in higher than expected (2.3% vs 1.5%), and at 10 AM we’ll get the latest read on Pending Home Sales which are expected to show a decline of 1.0%

In today’s Morning Lineup, we recap overnight events in Asia and Europe (pg 4), take a look at the rising levels of volatility in the Nasdaq 100 (pg 4), and then highlight the dollar’s rip higher in recent weeks (pg 5).

While equities are looking to gain today, the Nasdaq has declined 8.3% over just the last five trading days. Relative to history, this move hasn’t been extraordinary by any means, but it still hurts. Looking more recently at just the period since COVID first surfaced in early 2020, there have only been three other periods where the Nasdaq saw steeper declines in a five-day period.

The first two were during the COVID crash while the third occurred in September 2020 right when the Nasdaq experienced a short-term peak. What’s interesting to note about the current period is that ever since the start of 2022, we’ve started to see the intensity of five-day sell-offs start to increase.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.

Daily Sector Snapshot — 4/26/22

Chart of the Day: Do Bad Months Finish Strong?

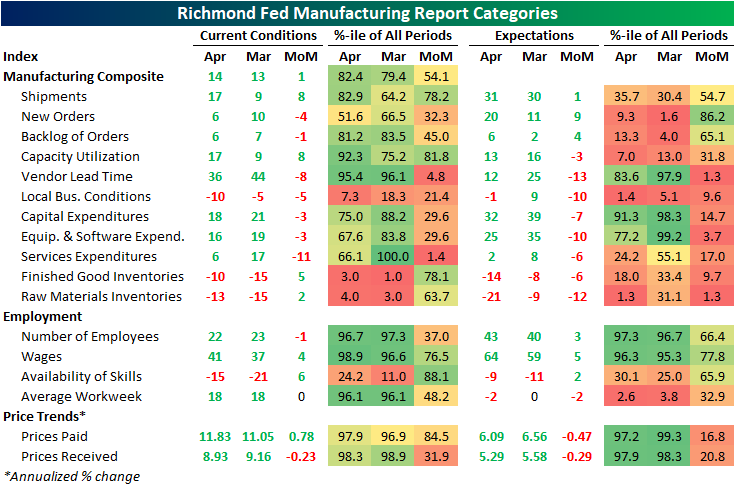

Shipments Saving Richmond

The Richmond Fed’s manufacturing survey was released this morning showing a modest improvement in conditions in the month of April. The headline number rose by a point to 14 which is still in the middle of the pandemic range of readings and the highest level since December.

In spite of the improvement in the composite index—a weighted average of shipments, new orders, and employment—the breadth of this month’s report was negative with over half of the categories declining month over month. Two of those declining categories were new orders and employment which are again inputs for the composite. That means the higher reading of the composite was entirely thanks to the 8-point increase in shipments.

Looking across other areas of the report, expenditures were weaker while inventories are recovering from historic lows. While business conditions are mixed to deteriorating, supply chains are showing signs of improvement as evidenced by the increase in shipments.

While shipments were an area of strength, another input to the composite, new orders, fell 4 points and is back near the middle of its historical range. Expectations, however, experienced a sizeable rebound with that index rising 9 points. While that increase bucks the trend of weak expectations readings relative to current conditions that we have seen in other regional Fed surveys (which we discussed in last night’s Closer), this index’s increase was the exception rather than the rule. As shown in the table above, only a handful of other expectations categories rose month over month with many declines ranking in the bottom decile of monthly moves.

The big increase to shipments left that index at the highest level since last July as backlog of orders are growing at a substantially more modest pace compared to earlier in the pandemic. One likely reason that both of these readings are improving is a coincident improvement in supply chain stress. The index for lead times saw an 8-point decline ranking in the bottom 5% of all monthly moves. That leaves the index one point above the December low of 35.

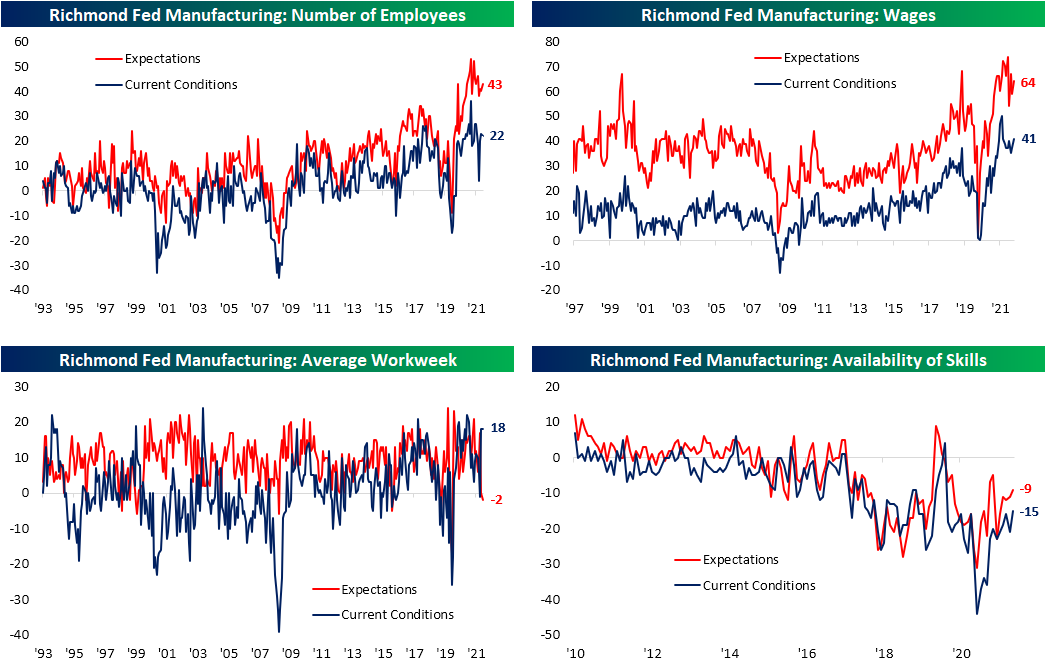

Employment metrics were mixed this month. The region’s firms are still hiring on a net basis, but hiring has peaked and declined again in April. That was in spite of firms also reporting better availability of workers with in-demand skills as that index rose to the highest level since July 2020. With that being said, the negative number indicates a still insufficient supply of quality talent. Wages, meanwhile, saw one of the larger increases in recent months rising to the highest level since September. The average workweek was unchanged at a healthy level in the top 5% of its historical range, but expectations are calling for declines in hours worked on the horizon. Click here to learn more about Bespoke’s premium stock market research service.

Bespoke Stock Scores — 4/26/22

Bespoke’s Morning Lineup – 4/26/22 – Big Tech Steps Up to the Plate

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

Bespoke’s Quote of the Day: “Good ideas are always crazy until they’re not” – Larry Page

Below is a snippet of content from today’s Morning Lineup for Bespoke Premium members. Start a two-week trial to Bespoke Premium now to access the full report.

Yesterday’s reversal was a welcome reprieve for bulls, especially after the straight line lower from early last Thursday. From a technical perspective, there’s not much positive to say about the charts of the S&P 500 and the Nasdaq, but to provide an optimistic scenario, we would note that both indices appear to be showing some signs of a reverse head and shoulders. It’s going to take a lot more upside to make these formations look more convincing, and the pattern for the Nasdaq is much looser than the pattern for the S&P 500, but we thought it was worth highlighting.

While the two largest US indices may, and we stress the word may, be showing early signs of a positive pattern, the semiconductors, which typically act as a leading indicator actually opened at their lowest level since Last May on Monday morning. That being said, like the broader market, the SOX did manage to turn things around finishing the day higher by just over 1.75% and outperforming the S&P 500 and the Nasdaq in the process.

Start a two-week trial to Bespoke Premium to read today’s full Morning Lineup.